Downside Case

1.8K posts

To be clear: 1/3 of $CCLFX sits in PIVs run by a third party. Nobody, not me, not you, not the anon PC accounts, can say the exact fee load on that sleeve. I am asking for TRANSPARENCY. What I can tell you: it’s fees on fees on fees. It’s gates on gates. CLO equity marked at par (someone tell me what CLO equity actually clears at right now??). And PIVs reported at NET exposure, not gross — so that 1.3x leverage headline (~$47B/$32.5B) is NOT the whole story. Don’t tell me I can’t scrutinize the third with layered fees because the other two thirds doesn’t have them. That’s not a defense. That’s a deflection. I want every loan, every allocation. The PIV black box is exactly why I can’t get there. If you want to justify that structure, I’m here. But “the rest of the portfolio is fine” isn’t the conversation I’m asking for. Why is it so offending that I would like to discuss the marks and fees being pushed to retail?

A Blue Owl fund is urging investors to reject a share purchase offer led by Boaz Weinstein’s Saba, saying the offer price is too low bloomberg.com/news/articles/…

This one is an interesting case study on what the price of liquidity is. For background: OBDC II attempted a merger with OBDC late last year. Long story, but investors in OBDC II would have taken a 20% haircut (the merger was cancelled) The fund manager is now guiding to fund liquidation (but keep in mind, the verbiage in SEC filings is pretty open) The fund sold $600M in loans (the crown jewels of the portfolio), and is making a distribution of about 30% to all investors. Enter Saba/Cox with their tender offer (~33% discount to NAV) for ~7% of outstanding shares. According to Blue Owl: "Cox and Saba's offer price is inadequate, arbitrary and substantially undervalues OBDC II's assets and ongoing access to liquidity." LOL Three things here: 1. the remaining portfolio is not all unicorns and roses 2. the offer is voluntary - meaning, investors who want to stay in the fund don't have to sell at this price 3. I bet the 20% discount to NAV via merger with OBDC (which, again, didn't happen) is looking fairly attractive in retrospect.. I did the math to estimate the value of the remaining assets (and see what investors stand to gain - or lose - by staying in the fund vs. tendering the offers) You can read it here: open.substack.com/pub/accredited…

@DumbInvestorGuy In the most extreme scenario (say 25% losses on the whole 1.3tln industry in the US), the losses on private credit will be less than a 1 day standard deviation in the US stock market.

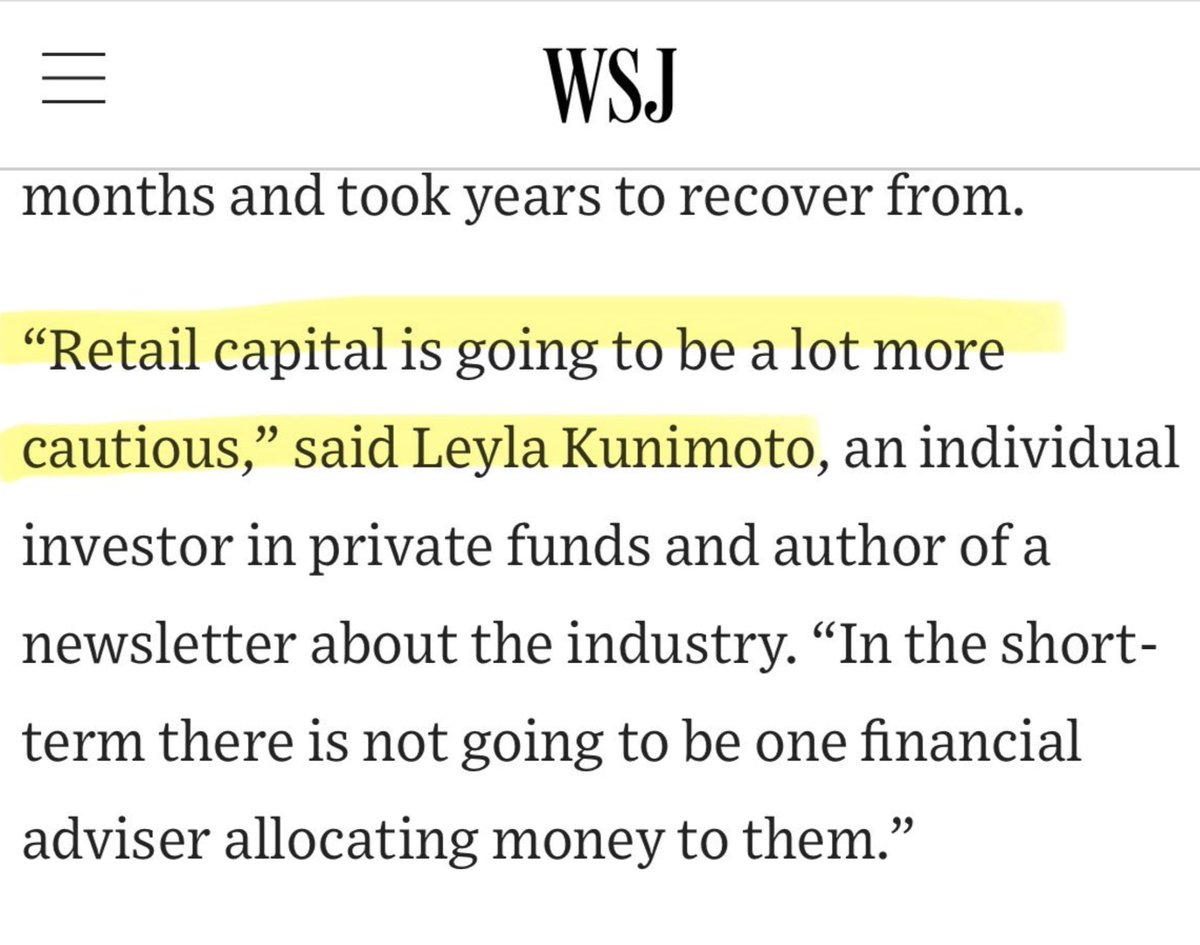

The private-credit engine that powered massive growth on Wall Street is sputtering, with investors trying to pull money out of big funds on.wsj.com/4s4rdlV

Three of the largest private credit firms on earth have blocked investor withdrawals in the last 14 days and they're still trying to put these products in your 401(k).

Goldman on European private credit: lenders are swapping debt for equity more than they're forcing bankruptcy. The question nobody's asking: are these lenders equipped to run the companies they're inheriting? Being a good underwriter doesn't make you a good operator.