Eric Kim

140 posts

Eric Kim

@EKbroker

Investor Bahamas Exumas Real Estate

Chicago/Miami/Bahamas Katılım Kasım 2014

546 Takip Edilen119 Takipçiler

What’s the best stock to buy right now sub $1b market cap?

English

@EhrmantrautCap_ $AMPG Wondering if the shorting is related to the rights that expire in a few weeks

English

$AMPG shorters are in for a massive beating at some point:

8.047 million shares short or 36.28% of the share float (as of June 23rd).

Not often do you see such a high level of shorting, especially for an incredible company of the likes of AmpliTech Group.

Time is on the side of the bulls.

Matt@ROIRecruiter

$AMPG shorts seem to be active once again. Doesn’t seem like they took the opportunity to cover… They actually increased their positions. Short interest- 8.04mil shares Short float- 36% For a company positioned so well with many growth levers being activated, I can’t see this ending well for them!

English

I've analyzed Leopold Aschenbrenner's entire portfolio.

There's just two stocks that actually got my attention, and have massive upside potential.

1. $WYFI | WhiteFiber

AI Data center pureplay with massive pipeline and upside potential.

The company is going for a retrofit stragety, deploying capacity on sites that already have secured power and are already built.

This makes it cheaper and faster to deploy capacity.

The pipeline is massive, 1.5GW is what management aims for.

That would put $WYFI at a $4B ARR.

It's currently sitting at a $1.8B MC.

WhiteFiber also focusses on selling Cloud-Services, potentially pushing revenue per MW.

If the company is ablte to execute well, this is a potential 15x until 2030.

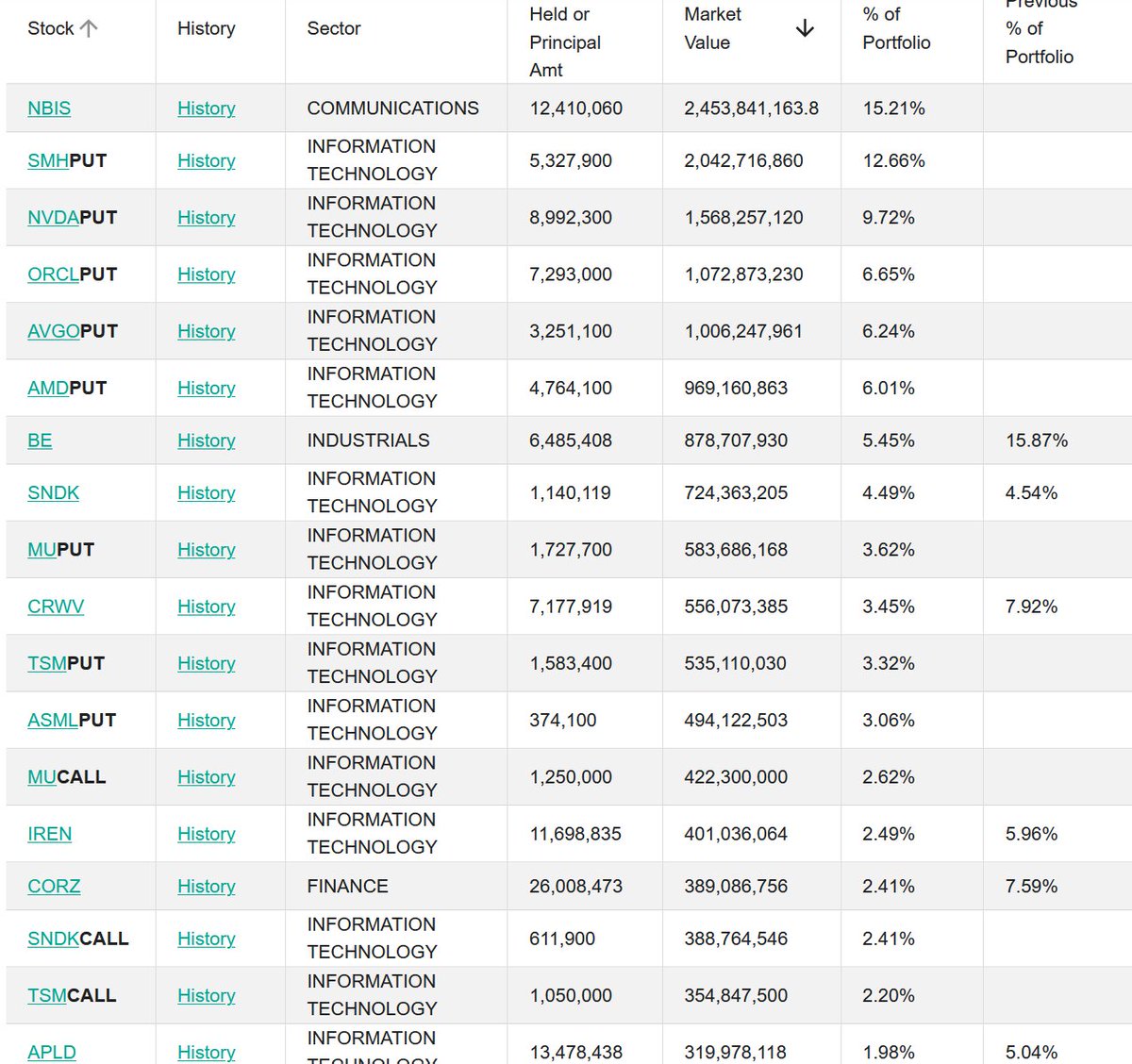

2. $CRWV | CoreWeave

The biggest Neocloud in todays market.

Cloud-computing services for hyperscalers.

Early access to $NVDA's newest tech.

The $99B in backlog prove the demand.

Revenue ramp expects 1500% growth until 2030.

The second reason for why this is so interesting, lays in the valuation difference to $NBIS.

They are currently worth roughlty the same.

But looking at revenue projection, $CRWV will generate double the revenue by 2030.

Profit margins will be pretty similar, the only problem with $CRWV is the massive debt.

But over time, this will become less and less relevant.

This makes one thing clear:

$CRWV will catch up to $NBIS valuation.

This comes on top of the massive growth that will be priced in over the next years.

Are you invested in these?

English

$AMPG

Why are you trying to spread fear?

Whether the demand requirement will be legally met or excused is the central battleground of this case, and AmpliTech Group (AMPG) is heavily favored to win a dismissal on this exact issue.According to AmpliTech’s SEC Form 8-K filing, the shareholder actually initiated a formal demand letter on October 31, 2024, followed by extensive correspondence through February 2025. However, because the board ultimately refused the demand, the filing party must now prove that this refusal was "wrongful", or that a formal pre-suit demand was entirely "futile" under Nevada law.

The filling party faces a steep uphill battle to successfully meet or excuse the demand requirement for three critical reasons:1. The Protection of Nevada’s Exculpation StatuteBecause AMPG is incorporated in Nevada, the lawsuit is bound by Nevada Revised Statute § 78.138(7). This law provides some of the strongest director-and-officer protections in the United States. To bypass the board's refusal or prove "demand futility," a plaintiff must plead highly specific, particularized facts proving that the directors engaged in intentional misconduct, fraud, or a knowing violation of the law. Gross negligence or simply making a bad financial decision is not enough to pierce Nevada's liability protections.2. AMPG's Proactive Independent Special CommitteeWhen the $3.2 million crypto phishing scam occurred in March 2024, the AMPG Board did not ignore it. They immediately took steps that legally insulate them:Formed an Independent Special Committee to run an internal inquiry.Retained independent outside legal counsel to review the breach.Formally identified the internal reporting weaknesses and instituted strict remedial control measures (such as mandatory dual authorization on wires and tiered approval hierarchies).Under the Business Judgment Rule, Nevada courts will heavily defer to a board that handles a crisis using an independent committee. AMPG's thorough and documented cleanup response will make it nearly impossible for the plaintiff to prove the board's subsequent refusal of the lawsuit was "wrongful" or self-interested.

English

$AMPG

Siber Saldırının Bedeli AmpliTech'e Ağır Oldu

Basit bir phishing tuzağı şirketin kasasından tek kalemde 3.2 milyon $ sildi. AmpliTech, sahte bir dijital varlık platformuna kanarak fonlarını sıfırladı.

Hisse hızla %8.5 düşerken hissedar davaları yolda. Ders çok net: Çift onay ve iç denetim eksiği olan şirketler devasa bir risktir.

Türkçe

$AMPG @gulVasikova

This is just a lot of noise and ammunition for the shorts

English

$AMPG

Whether the demand requirement will be legally met or excused is the central battleground of this case, and AmpliTech Group (AMPG) is heavily favored to win a dismissal on this exact issue.

According to AmpliTech’s SEC Form 8-K filing, the shareholder actually initiated a formal demand letter on October 31, 2024, followed by extensive correspondence through February 2025. However, because the board ultimately refused the demand, the filing party must now prove that this refusal was "wrongful", or that a formal pre-suit demand was entirely "futile" under Nevada law.

The filling party faces a steep uphill battle to successfully meet or excuse the demand requirement for three critical reasons:1. The Protection of Nevada’s Exculpation StatuteBecause AMPG is incorporated in Nevada, the lawsuit is bound by Nevada Revised Statute § 78.138(7). This law provides some of the strongest director-and-officer protections in the United States. To bypass the board's refusal or prove "demand futility," a plaintiff must plead highly specific, particularized facts proving that the directors engaged in intentional misconduct, fraud, or a knowing violation of the law. Gross negligence or simply making a bad financial decision is not enough to pierce Nevada's liability protections.2. AMPG's Proactive Independent Special CommitteeWhen the $3.2 million crypto phishing scam occurred in March 2024, the AMPG Board did not ignore it. They immediately took steps that legally insulate them:Formed an Independent Special Committee to run an internal inquiry.Retained independent outside legal counsel to review the breach.Formally identified the internal reporting weaknesses and instituted strict remedial control measures (such as mandatory dual authorization on wires and tiered approval hierarchies).Under the Business Judgment Rule, Nevada courts will heavily defer to a board that handles a crisis using an independent committee. AMPG's thorough and documented cleanup response will make it nearly impossible for the plaintiff to prove the board's subsequent refusal of the lawsuit was "wrongful" or self-interested.

English

@gulVasikova $AMPG Looks like an attempt to cover short positions. What does this have to do with the core business and the massive future opportunities?

English

@gulVasikova $AMPG Complaint from something that happened 2 years ago in 2024?

English

$AMPG Not the kind of headline investors want to see.

A shareholder’s intention to file a derivative complaint against AmpliTech Group $AMPG , its directors, and officers introduces a new layer of uncertainty beyond the company’s business fundamentals.

Derivative lawsuits typically allege that management or the board failed in their fiduciary duties, resulting in harm to the company and shareholders. The filing itself does not prove wrongdoing, but it can create legal costs, management distraction, and reputational risk.

For a small-cap company like AmpliTech, investor confidence can be particularly sensitive to governance-related issues. Even if the underlying business remains unchanged, legal disputes often pressure sentiment until more details emerge.

The key thing investors should watch is whether the complaint relates to disclosure practices, corporate governance, executive actions, or financial matters. The specifics will determine whether this becomes a temporary headline risk or a more significant issue.

For now, this appears to be a governance story rather than a technology or operational story.

Small-cap stocks can recover from legal overhangs if fundamentals remain intact, but uncertainty alone is often enough to keep investors on the sidelines until the facts become clearer.

English

Eric Kim retweetledi

Finland keeps showing the playbook: don’t just add compute—pair it with grid certainty, storage, and a credible local benefit loop. Battery + permitting + community integration is what turns “AI ambition” into resilient infrastructure.

prnewswire.com/no/pressemeldi…

English

Eric Kim retweetledi

@CKCapitalxx $VIVO Management converted 2.96 million class A public shares into unlisted class B shares in early 2026. There are now over 3.2 million shares short with a total public float of 2.37 million

English

$VIVO just shortlisted prospective AI tenants for their 41.5MW Norway data center following a competitive RFP process with multiple formal bids.

The catalyst I have been waiting for is closer than ever.

Let me remind everyone why this is still one of the most asymmetrical small cap setups in the market.

$75 million market cap. Already operational. Already generating $31 million in annualized revenue. Grid demand response already activated and paying. And now a formal shortlist of AI operators and infrastructure groups competing to become the anchor tenant.

This is not a company hoping someone shows up. Multiple parties submitted formal bids. The RFP process is competitive. That means $VIVO has leverage on pricing and terms. When you are the only operational renewable powered AI data center with sub $0.035 per kilowatt hour energy costs in Norway you do not beg for tenants. You choose them.

When a hyperscaler or AI neocloud signs that lease the revenue per watt jumps 3 to 5x over standard hosting rates. That single facility at AI compute pricing could generate $150 to $200 million annually.

And behind Norway sits 291MW of secured powered land in Finland and a 25MW sovereign AI platform in the UAE.

Management formally targeting $1 billion in revenue by 2029. By 2033 they are targeting $3 billion. On assets they already control today.

At $1 billion in revenue and 5x revenue multiple that is a $5 billion market cap from $75 million today.

The tenant announcement is the catalyst. The shortlist just told you it is coming.

English

Eric Kim retweetledi

Is it me, or has $VIVO been under reporting their pipeline? New investor presentation filed today with the SEC. sec.gov/Archives/edgar…

English

I don’t usually load up on small caps. But $AMPG and $VIVO are two of the best setups I have seen in this space in a long time.

$AMPG first.

46 person company that has already qualified into the supply chains of Lockheed Martin, Boeing, Raytheon, and NASA.

Those qualifications take years of security clearances, technical audits, and product validation. Most companies never get in the room. $AMPG is already supplying product.

AmpliTech designs and manufactures advanced RF and microwave signal processing components.

The hardware that sits inside 5G base stations, satellites, defense communications systems, and quantum computing infrastructure.

Every signal that travels through a modern wireless network passes through components like theirs.

$140 million in active LOIs with North American mobile network operators. Production shipments already started.

100% revenue growth guidance for 2026. Gross margins expanded from 33% to 48% in a single year. Zero debt. $18.4 million in cash.

And the EU opportunity is completely unpriced. European carriers are under mandate to eliminate Huawei and adopt Open RAN standards.

$AMPG’s certified O-RAN radios are exactly what Deutsche Telekom, Vodafone, and Orange need. They presented directly in front of all of them at MWC Barcelona. A single EU contract announcement is a company defining catalyst.

Now $VIVO.

$78 million market cap. 41.5MW data center in Norway operational today generating $31 million in annualized revenue. 291MW of secured powered land in Finland. 25MW sovereign AI platform in the UAE.

Management formally targeting $1 billion in revenue by 2029 on assets they already control.

Two completely different businesses. Same theme. Asymmetric setups with catalysts that have not happened yet at valuations that do not reflect what is coming.

This is exactly why I own both.

$AMPG $VIVO

English

@saso_capital $VIVO Don’t forget the Tembo ev spinoff already has an approved symbol $temb

English

$VIVO is the $ASTS of the AI infrastructure world.

The binding constraint on AI infrastructure is no longer silicon. It’s grid interconnection. VivoPower doesn’t build servers or sell GPUs. It acquires energized grid connections and powered land, then leases that infrastructure to AI compute tenants on long-term contracts. The business model is narrow by design: own the land, own the grid connection, build the shell. The tenant brings the technology. Revenue comes from bankable leases, not hardware cycles.

The reason this matters is scarcity. Grid interconnection rights in Europe are becoming structurally equivalent to wireless spectrum. They are finite, you cannot build a second grid. They are non-replicable, queue position is determined by regulatory process, not capital. They appreciate over time, as queues lengthen, the replacement cost of an energized connection rises. And they are jurisdictionally protected, governed by state transmission operators with no mechanism for bypass.

If you followed the $ASTS thesis, you already understand this pattern. AST SpaceMobile’s value was never the satellites. It was the spectrum access agreements, exclusive partnerships with mobile operators covering 2.8 billion subscribers across 50+ countries. The satellites are the delivery mechanism; the spectrum relationships are the moat. The market spent years pricing $ASTS on hardware execution risk while ignoring that the company was quietly locking up the scarcest input in direct-to-device connectivity: licensed spectrum access that no competitor could replicate.

$VIVO is running the same playbook in a different domain. The data center is the delivery mechanism. The grid interconnection is the moat. And the window to accumulate these rights at development-stage prices is closing as moratoriums spread across Europe and queue times extend past a decade.

I am positioned in $VIVO.

English

@KakashiCapital_ $VIVO What about the Tembo spinoff? With a target valuation of $838 million imo $vivo is about to be rerated!

English

$VIVO timeline mapped out

> ATM start and cancellation

> F3 filing and termination

> + many other tailwinds, events and catalysts

+ wasn’t aware that they received funding at $6.80 when they were trading in the $1’s

Still under that price

What am I missing?

Cc $DGXX $HIVE

English

Properly analyzing a company takes hours.

I do it for free.

But I'm only interested in ones with 5x potential.

→ Like this post if you want me to analyze one

→ Drop your ticker in the comments

Starting with the most requested.

Which one do you think could 5x?

English

@TF_141Z @CKCapitalxx $VIVO at only a $74 million market cap it’s a strong buy. Major catalysts coming!

English

@CKCapitalxx $VIVO Almost 20% of the float is now short. More importantly the short borrow rate is an annualized rate of 75%~80% or almost a quarter of a percent a day!!!! Max Pain!!

English