Ed Castel

2.1K posts

Ed Castel

@EdCastel10

⚡️ Seeking innovation, sharing insights

Magellan Capital Katılım Ocak 2018

1.8K Takip Edilen393 Takipçiler

Ed Castel retweetledi

Ed Castel retweetledi

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

English

Ed Castel retweetledi

After $GOOGL and $AMZN being frustrating to hold and then going on a generational run to ATHs, next up is $MSFT.

Book it. Typical rotation of the Mag 7.

English

Ed Castel retweetledi

$INTC I don't know who needs to hear this but $INTC is not a buy

Parabolic moves, regardless of who they are should be avoided.

English

@mat78704 @diyas_1989 I think $MU in the long run can go much higher, but in the short term, the parabolic move needs some rest, ATR multiple is almost at extreme.

Today I converted all of my 2x etf of MU and SNDK to shares , same size.

I’m ready for a 10-20% correction

English

这个信息对我的粉丝非常重要。我系统看MU到800-835就会被dump。而这个日期就在本周。我不建议乱做空,but protect your profit。

DegenQuant@BruceCMaster

IMO the best and most surprising proxy trade for Cerebras IPO: sell $MU/$DRAM. Cerebras use zero HBM. Second best is to long $VICR/$DGXX. So the long/short version I like is to long VICR short MU. Maybe need $MU to touch 1T to fade.

中文

Ed Castel retweetledi

Ed Castel retweetledi

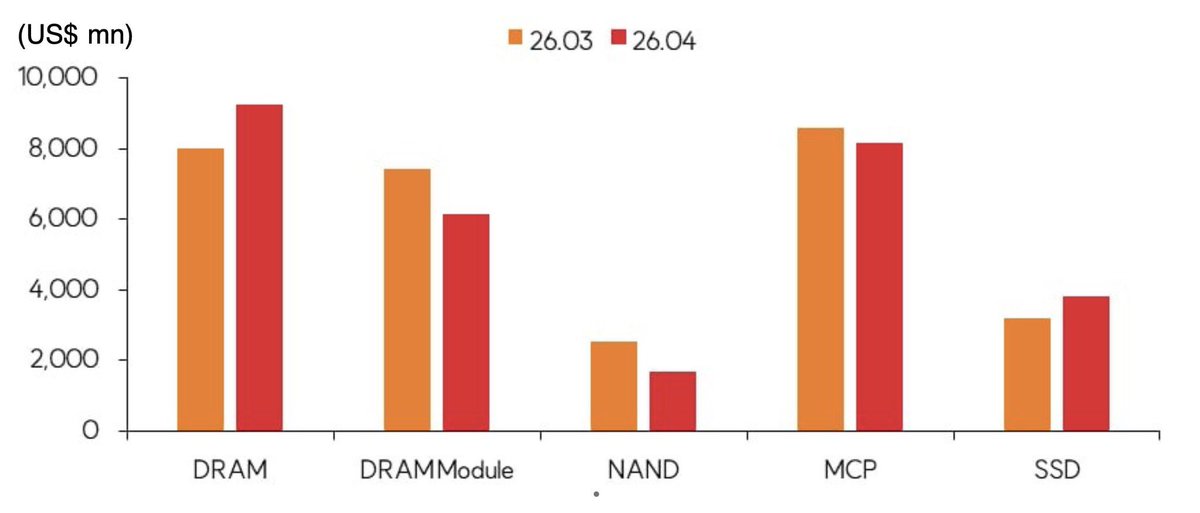

Memory prices are going absolutely vertical.

Look at the Korea export price data. DRAM +18%. DRAM excluding modules +35%. Flash memory +47%. SSD +140%. In one month.

This is a supply-constrained market running into 56% CAGR AI inference demand through 2031.

Main beneficiaries.

$SNDK – +500% YTD. Pure-play NAND. Only name with clean exposure to the storage side of the AI buildout. Entire supply sold out through 2026.

$MU – +124% YTD. Market cap just crossed $700B. HBM fully booked. DRAM average selling price up 32% quarter over quarter. New York megafab breaking ground January 2026.

SK Hynix – the HBM pure-play. Operating margins approaching 70%. Every HBM, DRAM, and NAND unit for 2026 already committed. Planning US ADR listing because Korean market valuation doesn’t reflect what global capital is willing to pay.

The NAND bit demand chart makes it a lot clearer: 286 exabytes in 2025. 1,686 exabytes by 2031.

AI inference driving 56% CAGR – three times faster than training and traditional workloads combined.

Secondary beneficiaries

While the big three chase HBM, they walked away from legacy 2D NAND.

Two Taiwanese names own that vacuum.

Macronix (2337.TW) – NAND revenue +382% YoY. Gross margin from 17% to 40.8% in twelve months.

Winbond (2344.TW) – Number one globally in SPI NOR flash. Own fabs. Lead times past nine months.

What is clear is that memory is no longer a commodity business it’s a structural shift.

You are not early, but there is definitely a lot more juice to run.

Jukan@jukan05

HOLY SMOKE. What the hell is this?? Memory prices are going absolutely insane. $DRAM $MU $SNDK

English

Ed Castel retweetledi

Lauching a chain is probably the worst u can do these days

You need TVL as proxy of success, no one wants or should be using defi with current security assurances specially on untested protocols on a new chain, you either have very special consumer apps or you're cooked.

English

Ed Castel retweetledi

Just wrapped our quarterly earnings call.

We are focused on delivering AI infrastructure and solutions that empower every business to eval-max their outcomes in this agentic computing era.

Our AI business surpassed a $37 billion annual revenue run rate, up 123%.

We are at the beginning of one of the most consequential platform shifts that will change the entire tech stack as we move from end-user driven workloads to workloads driven by end-users and agents.

This will drive TAM expansion and change the value creation equation across the entire economy.

To capture this opportunity, we are executing against two major priorities:

English

@redactedrain actually, your employer fundraiser looks like a top

English

Absolute intergalactic top on these slop videos

MegaETH@megaeth

MEGA will go live: 6am EST onchain. 7am EST offchain. April 30th, 2026

English

dear @Official_Upbit

make me rich

MegaETH@megaeth

MEGA will go live: 6am EST onchain. 7am EST offchain. April 30th, 2026

English

Ed Castel retweetledi

Exciting news - GPT-Image-2 by @OpenAI has claimed the #1 spot across all Image Arena leaderboards!

A clean sweep with a record-breaking +242 point lead in Text-to-Image - the largest gap we’ve seen to date.

- #1 Text-to-Image (1512), +242 over #2 (Nano-banana-2 with web-search aka gemini-3.1-flash-image)

- #1 Single-Image Edit (1513), +125 over #2 (Nano-banana-pro aka gemini-3-pro-image)

- #1 Multi-Image Edit (1464), +90 over #2 (Nano-banana-2)

No model has dominated Image Arena with margins this wide.

Huge congratulations to @OpenAI on this major breakthrough in image generation! More performance breakdowns by category in the thread below.

OpenAI@OpenAI

Made with ChatGPT Images 2.0

English

Ed Castel retweetledi

Ed Castel retweetledi

POV: Me and bros day to day life after full porting the $MSFT and $META pullback…

English

Ed Castel retweetledi

The world is transitioning to a compute-powered economy.

The field of software engineering is currently undergoing a renaissance, with AI having dramatically sped up software engineering even over just the past six months. AI is now on track to bring this same transformation to every other kind of work that people do with a computer.

Using a computer has always been about contorting yourself to the machine. You take a goal and break it down into smaller goals. You translate intent into instructions. We are moving into a world where you no longer have to micromanage the computer. More and more, it adapts to what you want. Rather doing work with a computer, the computer does work for you. The rate, scale, and sophistication of problem solving it will do for you will be bound by the amount of compute you have access to.

Friction is starting to disappear. You can try ideas faster. You can build things you would not have attempted before. Small teams can do what used to require much larger ones, and larger ones may be capable of unprecedented feats. More and more, people can turn intent into software, spreadsheets, presentations, workflows, science, and companies.

People are spending less energy managing the tool and more energy focusing on what they are actually trying to create. That shift brings a kind of joy back into work that many people haven’t felt in a long time. Everyone can just build things with these tools.

This is disruptive. Institutions will change, and the paths and jobs that people assumed were stable may not hold. We don’t know exactly how it will play out and we need to take mitigating downsides very seriously, as well as figuring out how to support each other as a society and world through this time. But there is something very freeing about this moment. For the first time, far more people can become who they want to become, with fewer barriers between an idea and a reality. OpenAI’s mission implies making sure that, as the tools do more, humans are the ones who set their intent and that the benefits are broadly distributed, rather than empowering just one or a small set of people.

We're already seeing this in practice with ChatGPT and Codex. Nearly a billion people are using these systems every week in their personal and work lives. Token usage is growing quickly on many use-cases, as the surface of ways people are getting value from these models keeps expanding.

Ten years ago, when we started OpenAI, we thought this moment might be possible. It’s happening on the earlier side, and happening in a much more interesting and empowering way for everyone than we’d anticipated (for example, we are seeing an emerging wave of entrepreneurship that we hadn’t previously been anticipating). And at the same time, we are still so early, and there is so much for everyone to define about how these systems get deployed and used in the world.

The next phase will be defined by systems that can do more — reason better, use tools better, plan over longer horizons, and take more useful actions on your behalf. And there are horizons beyond, as AI starts to accelerate science and technology development, which have the potential to truly lift up quality of life for everyone. All of this is starting to happen, in small ways and large, today, and everyone can participate. I feel this shift in my own work every day, and see a roadmap to much more useful and beneficial systems. These systems can truly benefit all of humanity.

English

Ed Castel retweetledi

First it was $META in 2022.

Then it was $GOOGL in 2025.

Now it’s $MSFT in 2026.

If we’ve learned anything from history, you don’t want to bet against big tech long term.

English

Ed Castel retweetledi

Microsoft tiene 450 millones de licencias de M365.

Copilot tiene 15 millones de usuarios de pago. $MSFT

Eso es un 3.3% de penetración. 96.7% sin explotar.

Los ingresos de M365 crecieron un 17% mientras que las licencias solo crecieron un 6%.

La brecha es el poder de precios. Microsoft no necesita nuevos clientes, necesita que los existentes actualicen.

Y la actualización acaba de volverse mucho más atractiva.

El 9 de marzo, Microsoft lanzó Copilot Cowork, un verdadero agente autónomo construido con Claude de Anthropic.

No un asistente. Un agente.

Analiza un mes de reuniones, construye el informe, envía el correo. Una instrucción. Hecho.

ChatGPT no puede hacer eso. No tiene tu calendario, tus archivos, tu historial de Teams.

Copilot Cowork sí. De forma nativa.

La matemática es simple:

10% de penetración = $16 mil millones en nuevos ingresos anuales

20% de penetración = $32 mil millones, aproximadamente el tamaño de Google Cloud hoy

El mercado aún no está valorando esto.

Anthropic construyó el producto que amenazó el valor de las acciones de Microsoft.

Microsoft licenció la tecnología, la integró en 450 millones de lugares de trabajo y lo llamó Copilot.

Eso no es ponerse al día.

Eso es distribución a escala.

$MSFT

Español