Mr. Gravity

1K posts

Mr. Gravity

@Endogenous_i

Endogenous (Emergent) Transactional Interpretation of Everything...

Katılım Ekim 2011

546 Takip Edilen220 Takipçiler

What is happening here?

The US birthrate is now down -30% since pre-2008 levels while financial wealth is at record highs.

Why? Because only asset owners are able to afford this economy.

As shown in our below analysis, this crisis accelerated in both 2008 and 2020.

And, with every recession and every round of inflationary economic stimulus, the crisis simply accelerates even further.

Now, we are seeing the biggest divergence between the S&P 500 and the US birth rate in history.

The result? Tons of young Americans simply cannot afford to have kids in another sign of the "K-Shaped" economy.

The US is facing a massive demographic crisis.

English

Mr. Gravity retweetledi

🚨 The wait is over!

The In Gold We Trust report 2026 has just been released, marking the 20th edition of this landmark publication. 🪙📘

Dive into the latest insights on gold, silver, commodities, monetary shifts & the future of the global financial system. 🌍📈

📥 Get your free copy fresh off the presses here:

ingoldwetrust.report/in-gold-we-tru…

#InGoldWeTrust #20YearAnniversary #GoldReport #GoldInvesting #SilverRally #PreciousMetals #SoundMoney #Commodities #DeDollarization #MonetarySystem #FinancialMarkets #GlobalEconomy #Geopolitics #AustrianEconomics #MacroResearch #MonetaryFuture #IGWT26

English

@ThierryBorgeat Monopoly money, but also a Monopoly... Question is, how fast and when do they eclipse Verizon?

English

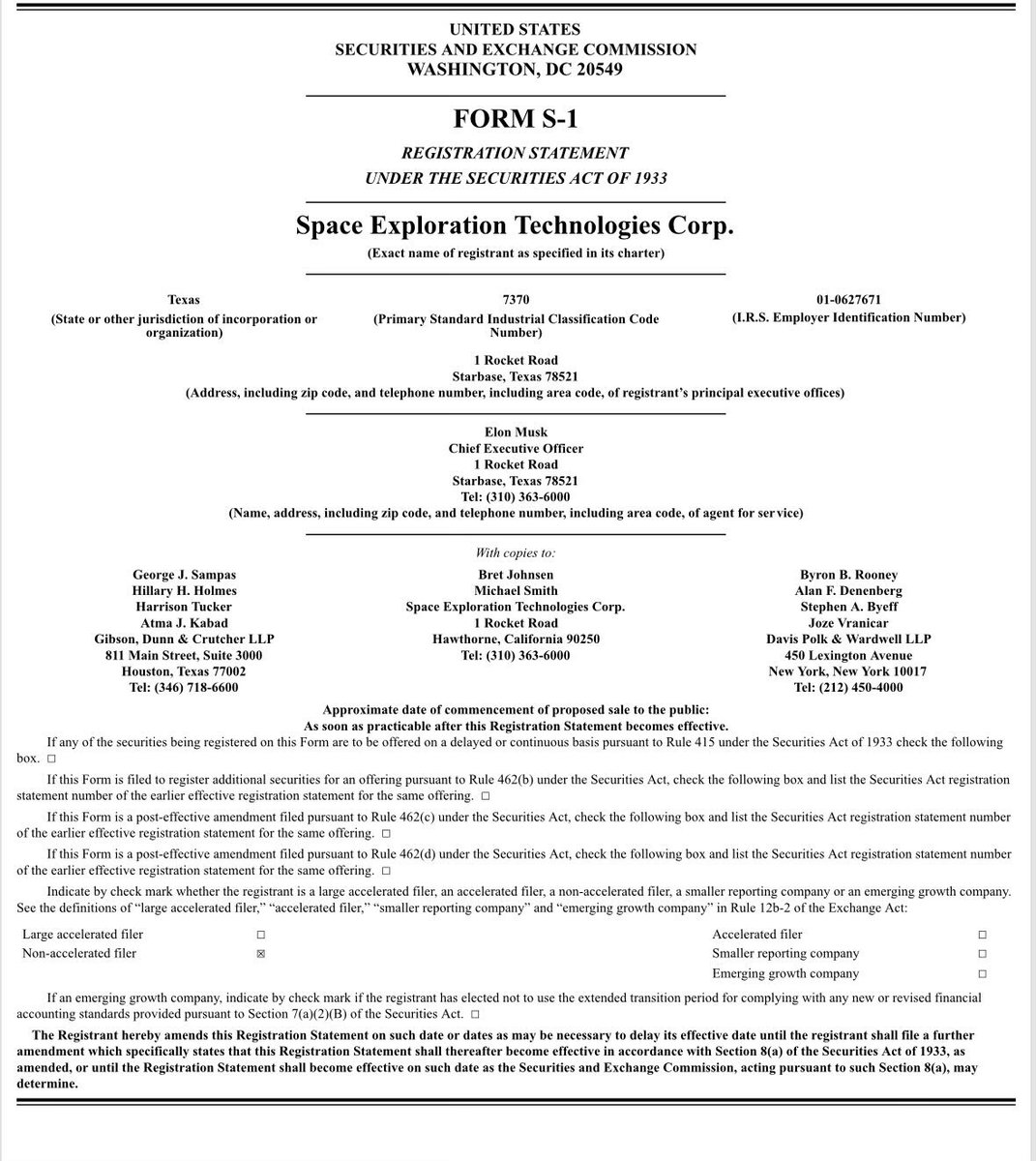

🚨YOU ARE THE EXIT LIQUIDITY

You are about to be offered the most expensive IPO in modern history.

SpaceX's S-1 just dropped. The headline numbers:

- 2025 revenue: $18.7 billion

- 2025 net loss: $4.9 billion

- Q1 2026: still losing money

- Reported IPO valuation target: roughly 90 times sales

For context, the previous record IPO, Saudi Aramco, listed at 6 times sales. SpaceX is asking for fifteen times that multiple. With a net loss attached.

Four things in this S-1 that should make you pause.

English

Gold and Silver Alert

4 hour charts creating the inverted head and shoulders pattern with positive divergence in relative strength.

bob coleman@profitsplusid

Silver market structure developing. hourly chart has an inverted head and shoulders. 4 hour chart has the left shoulder and head with positive divergence in relative strength.....waiting for the right shoulder to develop. Could see another pullback, ideally looking for 73-74 to hold. A lot of call options were obliterated since Friday, with volatility skew spiking from very bullish to neutral readings. To follow more of my work goldsilvervault.com/iav_blog/

English

@chamath When is the new social contract for the young being delivered?

English

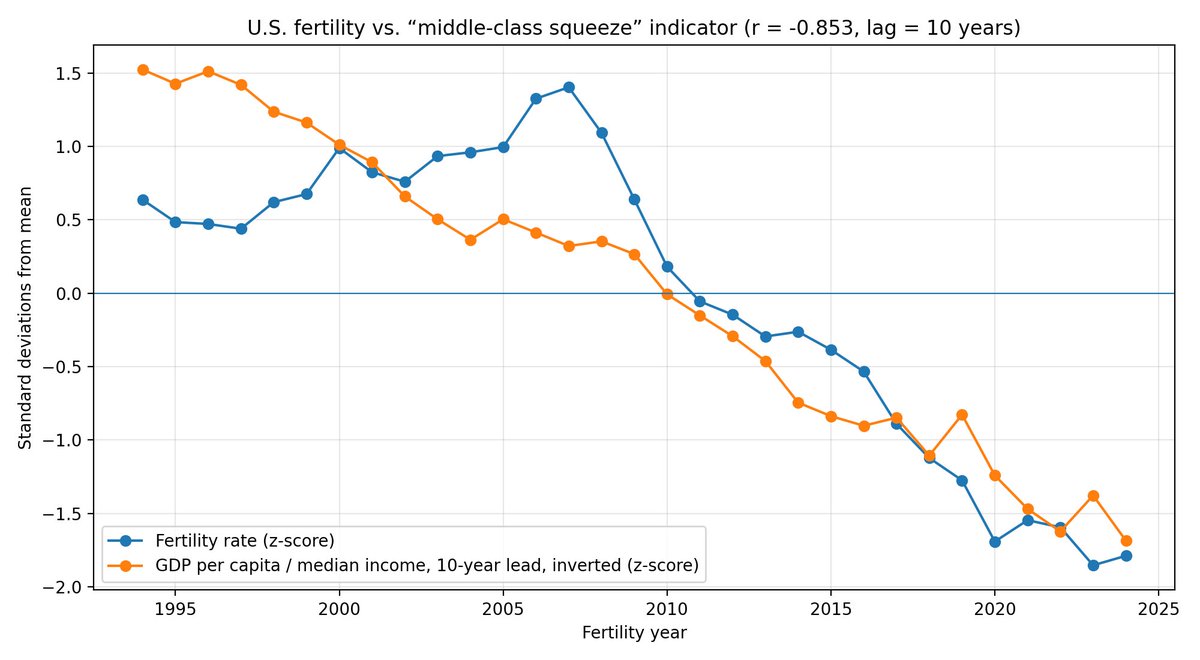

I took the first chart on fertility rate and then asked the following:

“Run a Monte Carlo simulation where you overlay various economic indicators on this chart of fertility. For example, GDP, GINI, cost of housing, middle class income growth etc. find the economic indicator that has the highest correlation to the chart provided. There may be a lag effect where the chart is the byproduct of some economic event so consider this lag in your correlation analysis.”

Result: the strongest match was not GDP, Gini, or housing alone. It was a derived “middle-class squeeze” indicator: real GDP per capita ÷ real median household income, with the indicator leading fertility by 10 years. The correlation was r = -0.853 over the 1994–2024 fertility window. Interpreted plainly: when output per person rose faster than median household income, fertility tended to be lower roughly a decade later.

English

End of the Republic.

Beginning of the Empire.

And what better way to announce it than by triggering the greatest petrodollar milkshake monetary reset?

Polymarket@Polymarket

JUST IN: Trump announces he's "seriously considering" making Venezuela the 51st state.

English

@Hedgeye The new policy will continue to be, extend and pretend, avoiding foreclosures nationwide, and thus limiting inventories of resale homes

English

U.S. Affordability Crisis:

Blue is affordable. Orange is not.

Very little of the map is still blue.

In Q1 2020, California was the only unaffordable state. Five years later, 17 states are.

As of mid-2025, owning a median-priced home consumed 47.7% of median household income nationally.

The entire West Coast and Northeast corridor are orange.

This is the K-shaped economy revealing itself on a map.

The U.S. has an affordability problem.

English

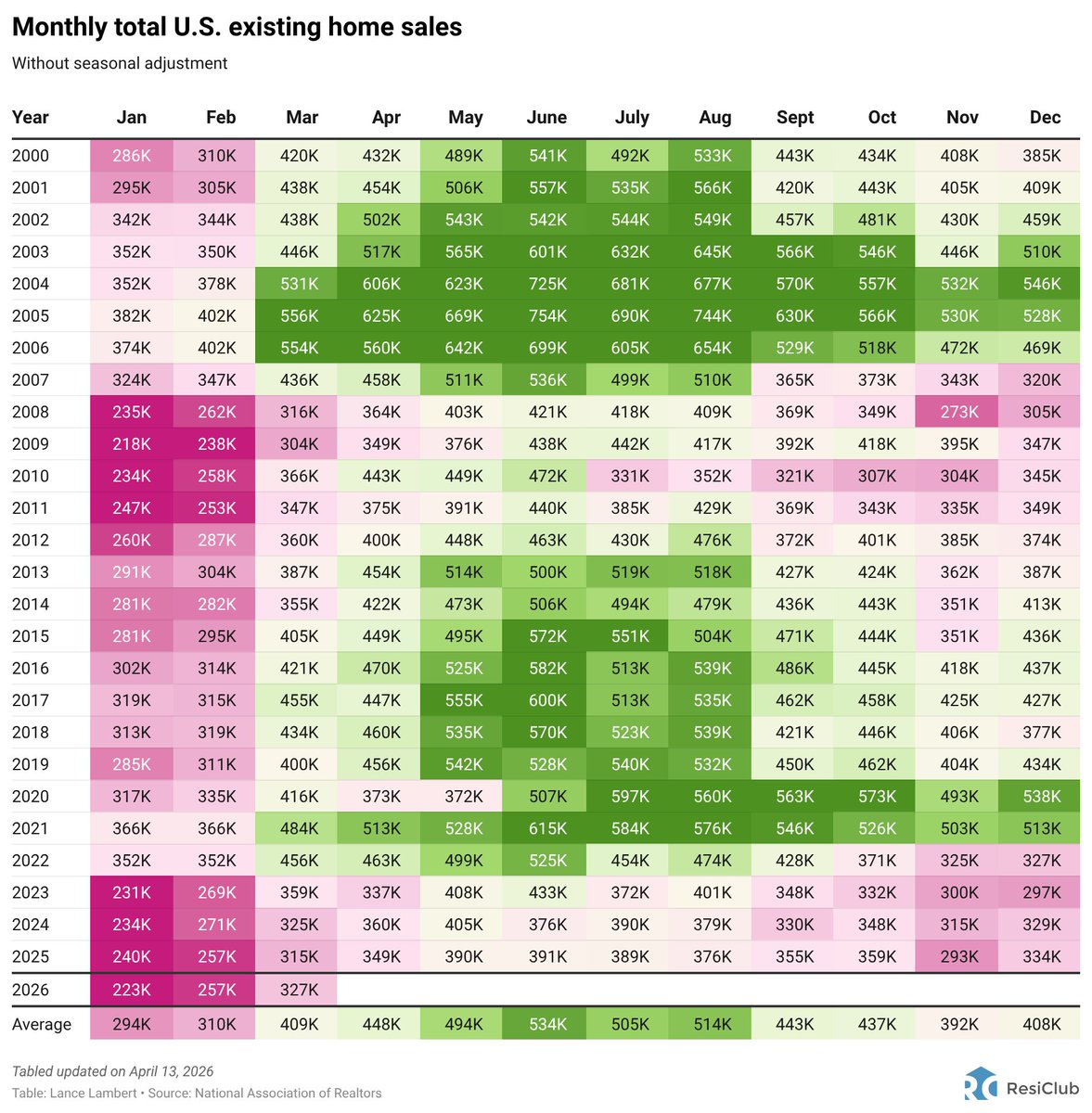

Mr. Gravity retweetledi

U.S. existing home sales by month

Resale turnover remains constrained

This is the raw adjusted data

Table via @ResidentialClub

English

We’ve spent $300 billion a year defending Europe

Making it easier for Europe to afford socialism

When Europe refuses to back up the U.S., it’s time to leave NATO

Peter St Onge, Ph.D.@profstonge

Trump threatens to quit NATO. We spend $300 billion a year defending Europe — including their war in Ukraine. But when we need them they don’t lift a finger. What it would take to leave.

English

This is the most SHAMELESS structural manipulation of a major index I've ever seen.

SpaceX is preparing what could be the largest IPO in history.

Target valuation: $1.75 trillion.

That would make it the sixth-largest company in America on day one.

And Nasdaq wants the listing so badly they're literally CHANGING how the Nasdaq-100 works.

In February, Nasdaq published a "consultation" proposing sweeping changes to how companies enter the index. The timing is pure coincidence, of course.

Just like it's pure coincidence that SpaceX has reportedly made fast index inclusion a CONDITION of listing on Nasdaq.

Here's what they're proposing:

A new "Fast Entry" rule would let any newly listed company whose market cap ranks in the top 40 of current Nasdaq-100 members get added to the index after just 15 trading days.

No seasoning period. No liquidity requirements. Completely exempt from the standards every other company had to meet.

Currently, new public companies typically wait up to a year before they're eligible for major index inclusion.

That waiting period exists for a reason. It lets the market establish real price discovery. It protects passive investors from being forced into untested, illiquid stocks.

And Nasdaq wants to throw all of that out. For ONE listing.

But the Fast Entry rule isn't even the worst part...

The real scandal is the 5x float multiplier.

Right now, the S&P 500 uses a free-float adjusted methodology. If only 5% of a company's shares are available for public trading, the index weights you at 5% of total market cap.

That's common sense. You weight a company based on what investors can actually buy.

Nasdaq's current methodology already uses total market cap rather than free-float for weighting. But for very low-float stocks, they at least had a 10% minimum float threshold.

Under the new proposal, that threshold DISAPPEARS entirely.

Instead, any stock with less than 20% free float gets weighted at FIVE TIMES its actual float percentage, capped at 100%.

Do the math on SpaceX:

If SpaceX IPOs at $1.75 trillion and floats 5% of its shares, there would be roughly $87.5 billion worth of stock available for public trading.

Under Nasdaq's proposed 5x multiplier, the index would weight SpaceX at 25% of its total market cap. That means passive funds would be forced to buy as if SpaceX were a $437.5 billion company.

But only $87.5 billion of stock actually exists in the market.

You are forcing hundreds of billions in passive buying into a $87.5 billion float.

QQQ alone manages nearly $400 billion. The total Nasdaq-100 ecosystem represents over $1.4 trillion in exposure across ETFs, mutual funds, structured notes, and derivatives.

Every single passive vehicle tracking this index would be REQUIRED to buy SpaceX at whatever price the market dictates.

On Day 15.

With zero price discovery. Zero track record as a public company. And a float so thin you could read through it.

So what this actually does is it creates a structural wealth transfer mechanism.

The passive bid from index funds pushes the stock price higher. That higher price benefits exactly one group of people: the insiders and early investors who own the other 95% of the shares.

And when lock-up periods expire 90 to 180 days later? Those insiders sell into the artificially inflated passive bid. Your 401(k) is the exit liquidity.

This is the fundamental corruption of indexing.

Indexing used to be brilliant. Low cost. Efficient. You were free-riding on the price discovery done by active managers. The index reflected the market.

Now the index IS the market. Trillions of dollars flow blindly into whatever the index tells them to buy. And the people who control the index methodology are changing the rules to serve the interests of a single IPO candidate.

The S&P 500 requires companies to have at least 50% of shares available for public trading. It requires 6 to 12 months of seasoning. It uses free-float adjusted weighting so passive investors aren't buying phantom liquidity.

Nasdaq is doing the exact opposite. 15 days. No float requirement. 5x multiplier on insider-held shares.

Every passive investor in QQQ, QQQM, and every fund benchmarked to the Nasdaq-100 should understand what's about to happen:

The rules are being rewritten to benefit IPO issuers and early-stage insiders, and your capital is the tool being USED to enrich them.

45 years in this business and I've watched Wall Street find creative new ways to separate retail investors from their money in every cycle. But usually they at least try to be subtle about it.

This one they put in a PDF and called it a "consultation."

What's your take?

English

Prices are the result of socialized highly leveraged financing, where losses are socialized, and gains are privatized... Corporate RE investors are free riders on a system for life-necessities, exploiting the commons and the socialized pricing mechanisms. END all government intervention in housing finance!

English

Private property rights are the foundation of capitalism and are part of what made America great.

Restricting property rights is a terrible idea.

Elizabeth Warren’s Housing Coup wsj.com/opinion/housin…

English

@DarioCpx What should naturally happen when the physical backing (implied security) for a futures contract is decreasing?

English

This is one of the most absurd charts I have ever come across: the silver futures market, rather than benefitting from higher prices, with participants rejoicing for more business because of the growing relevance of the commodity, is dying instead.

JustDario@DarioCpx

Is anyone else out there harbouring the same gut feeling that silver price suppression might have ended now that the focus shifted on keeping crude oil prices down at any cost? Just curious to know 😊

English

@KarelMercx Why does the decrease of backing (or implied security) for futures contracts, as a percentage of the open interest, necessitate higher ATH prices for physical?

English

In the past 30 days, silver backing futures in Shanghai and COMEX have dropped by 25 million ounces.

Combined, only 88 million ounces remain.

A new all-time high in silver is just a matter of time.

Karel Mercx@KarelMercx

English

In theory, underwriting is predicting forward 3 years. So AI should tell itself now it's going to eliminate a staggering number of jobs in the economy, and perhaps not to make loans today in advance of pending job and income losses. There should be a predictive score for that risk...

But, in practice, underwriting is mostly BS compliance for fast gain on sale, that doesn't itself predict or prevent defaults at all. Historically credit scores are the #1 single most accurate predictor of future loan performance (payment history), and accumulated personal savings is number #2 (skin in the game).

English

Mortgage lender Better has teamed up with OpenAI to "fully underwrite a mortgage loan" in as little as 47 seconds.

This sounds like great news for borrowers, especially if costs are cut and passed to consumers.

It doesn't paint a bright future for underwriters and LOs though.

Initially, LOs feed consumer application data and documents into the Tinman AI app.

How long before consumers just do it all themselves?

English

@KarelMercx @adam702989 @KarelMercxTA one Contrathesis is a War-path to Re-dollarization through increased control of Oil; death-spiral of the Dollar exaggerated (or reversing) after acute war issues resolve.

English

The only thing that scares me is that I have never been this certain about an investment thesis, and I have been investing for almost 30 years. The more I dig, the more convinced I become. That is dangerous, because knowing a lot can create the illusion of control, while markets remain uncontrollable.

English

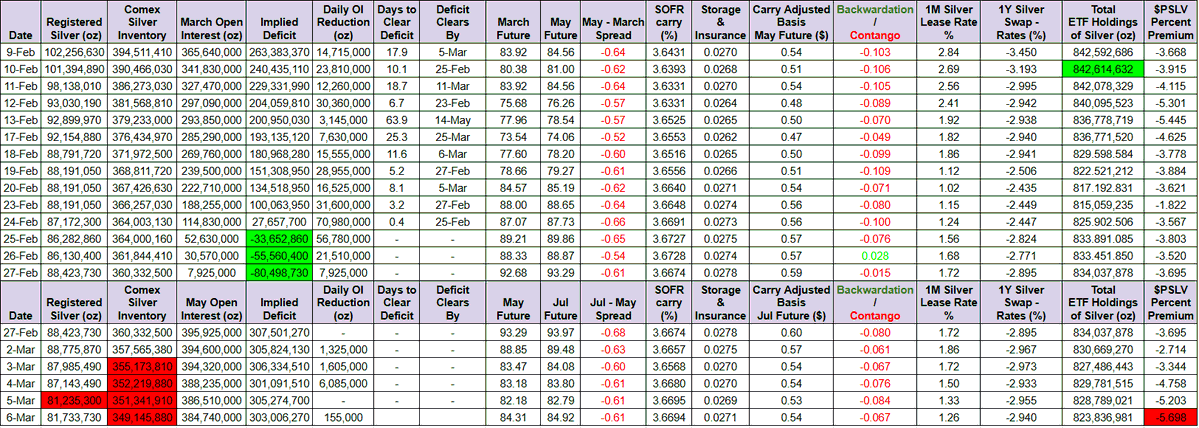

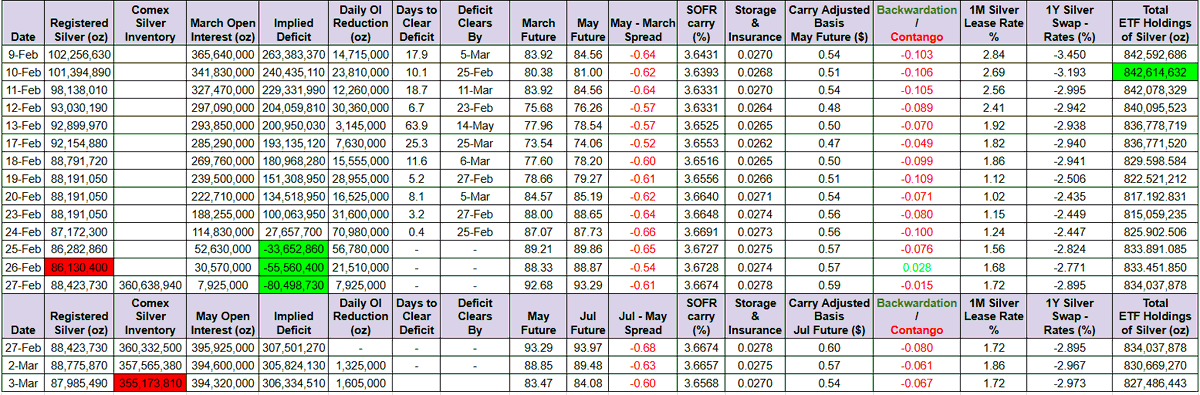

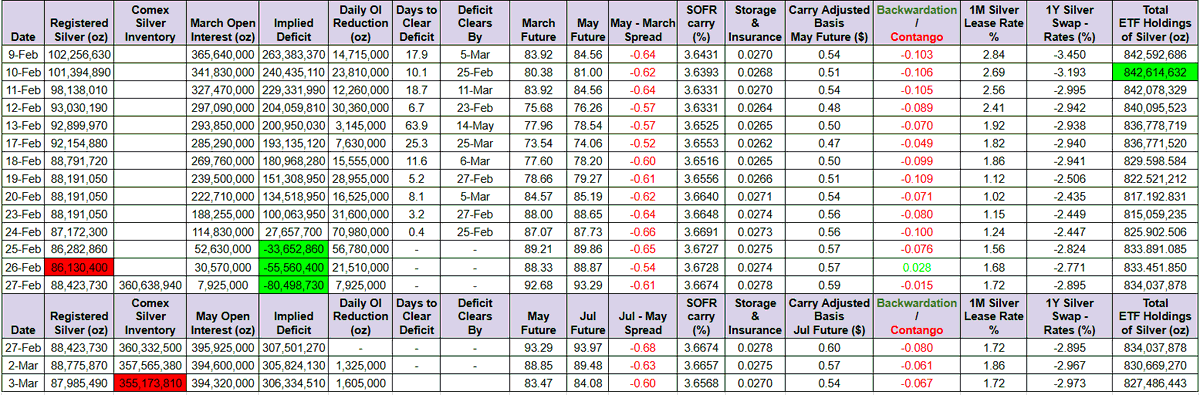

Silver is leaving the COMEX every trading day. That means professional buyers are taking physical silver out of the COMEX.

What makes it fascinating is that, at the same time, retail investors are getting more negative on silver. In the new $PSLV Percent Premium column, you can see that Sprott Physical Silver Trust is trading at a 5.7% discount. That discount shows retail investors still do not want silver.

The key point is that investors can buy and sell $PSLV without the amount of silver in the trust changing. In a real silver bull market, investors pay a premium instead. In 2011, the average premium for the full year was 17.3%.

That tells you a lot. This bull market is not being driven by Western investors. The 2011 bull market clearly was.

If Western investors do come back, $PSLV can deliver returns that are 23% higher than the move in the physical silver price alone, simply because the discount can turn into a premium like it did in 2011.

I think this bull market can become even more extreme than in 2011. There is more debt, the dollar is losing influence, and silver is more important than ever for industry. That means the premium at the top of this bull market can also go much higher.

Karel Mercx@KarelMercx

English

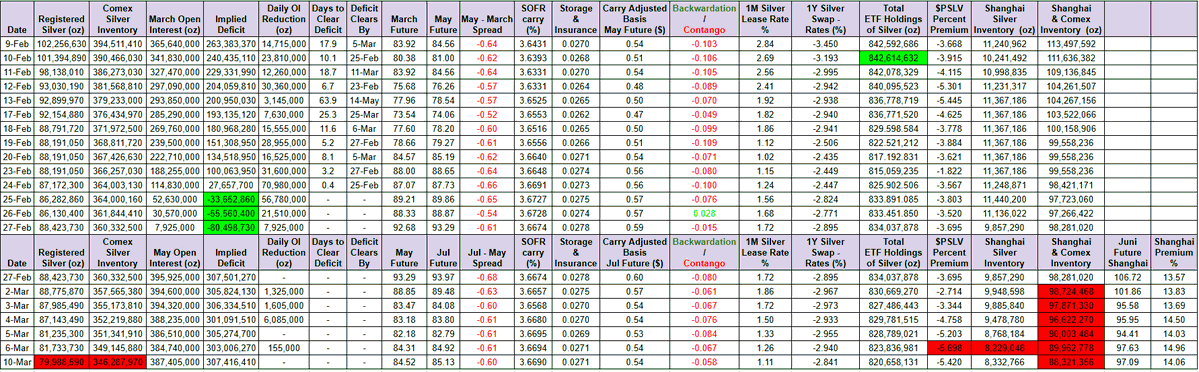

I want to start tracking in the table the daily gap between the silver price in the East and the silver price in the West.

This may be one of the most misleading indicators out there. A lot of people compare the US close with the China close, even though there are hours between them.

Silver is volatile, so that creates big distortions. During the silver crash, people on X were shouting that paper silver was being dumped in the West because the gap had suddenly blown out to $40, while China simply caught up on Monday.

I also find it irritating when people compare prices in dollars instead of percentages. A 10% premium at 50 is 5, and a 10% premium at 100 is 10. The percentage premium is identical, but the dollar gap is twice as big. That can easily give the wrong impression.

Then there is the question of what to compare. The active futures month in the West is May, while the active futures month in the East is June. That is a one-month difference. I do not want to use spot, because I do not find the spot market transparent in the West, and the same applies in the East.

So I want to use a moment when both markets are open. For COMEX I use settlement, which is between 12:24:00 and 12:25:00 Central Time. For the Chinese futures price, I take the average price during that same minute and divide it by the average USD/CNY exchange rate during that minute. After that, I divide everything by 32.1507, because the West uses troy ounces and China uses kilos.

For May COMEX I get $84.92, and for China I get $97.63. That gives a premium of 14.96%. What I find even more interesting is the trend over the past few days, because it is moving higher:

13.57%

13.83%

13.69%

14.50%

14.03%

14.96%

I am very curious what you think.

Karel Mercx@KarelMercx

Silver is leaving the COMEX every trading day. That means professional buyers are taking physical silver out of the COMEX. What makes it fascinating is that, at the same time, retail investors are getting more negative on silver. In the new $PSLV Percent Premium column, you can see that Sprott Physical Silver Trust is trading at a 5.7% discount. That discount shows retail investors still do not want silver. The key point is that investors can buy and sell $PSLV without the amount of silver in the trust changing. In a real silver bull market, investors pay a premium instead. In 2011, the average premium for the full year was 17.3%. That tells you a lot. This bull market is not being driven by Western investors. The 2011 bull market clearly was. If Western investors do come back, $PSLV can deliver returns that are 23% higher than the move in the physical silver price alone, simply because the discount can turn into a premium like it did in 2011. I think this bull market can become even more extreme than in 2011. There is more debt, the dollar is losing influence, and silver is more important than ever for industry. That means the premium at the top of this bull market can also go much higher.

English

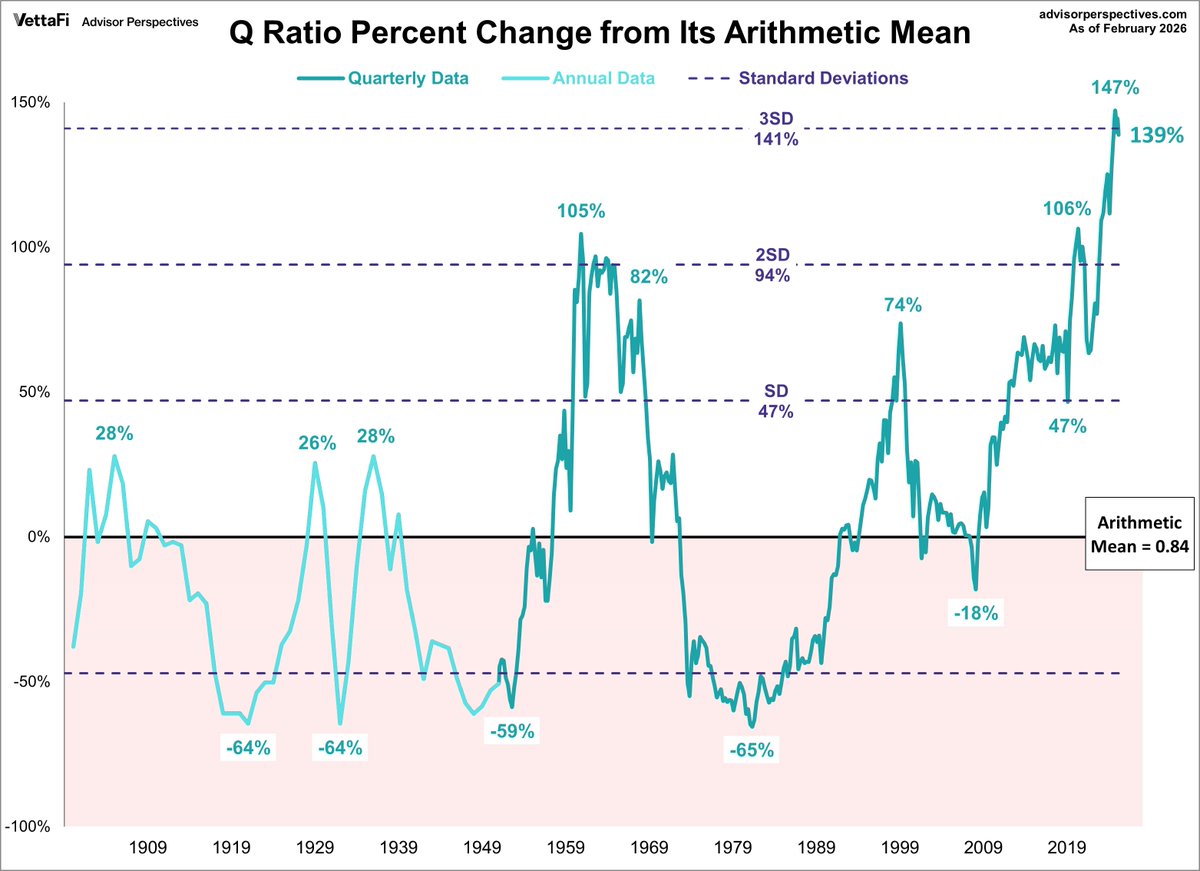

@TheELongWave @Grok Tell us more about the Q ratio and this post

English

139% Above Its Mean. Every Prior Peak Collapsed."

This is the Q Ratio — the broadest measure of US stock market valuation vs. the replacement cost of assets.

Right now? 139% above its long-run average.

We just touched 147% — above the 3 Standard Deviation line.

Here's what history shows every single time this chart got extreme:

1929 peak → -64%

1937 peak → -64%

1968 peak → -65%

2000 dot-com peak → bottomed at -18% (cushioned by Fed intervention)

Mean reversion isn't a theory. It's the most reliable pattern in 120 years of market data.

The arithmetic mean is 0.84.

We are not at 0.84.

Markets don't stay at 3 standard deviations.

They never have. The only question is timing!

Source: VettaFi / Advisor Perspectives — February 2026

English

🔥1-MONTH SILVER LEASE RATE ~ 3% INDICATES

💥"IT'S ONLY A MATTER OF TIME BEFORE SILVER PRINTS A NEW ALL-TIME HIGH" ‼️

Karel Mercx@KarelMercx

No matter how you look at the silver price, it has to go higher. Since Feb 9, retail investors have sold roughly 15 million ounces of physical silver. Yet the market did not get relief. The 1 month silver lease rate is still extremely high, and the 1Y Silver Swap -Rates (%) is still extremely distorted. I call it extreme for a reason: a 1 month lease rate should round to zero, and the 1Y swap rate should always be positive. At first glance it looks like the market is getting some breathing room because Registered silver stopped falling. Look under the hood and you see the opposite: silver is still leaving COMEX on a net daily basis. Now ask yourself what happens when retail comes back and buys more than 15 million ounces via ETFs. Exactly: the market gets tighter than ever, instantly. It is only a matter of time before silver prints a new all time high. This bull market is far from over.

English

@KarelMercx Yes, generally, but Else: Silver-lease rates are down, gold-lease to silver-lease spread is down, GSR around 60 is low, SO at what point or level may the relative lease rates indicate relative future performance+/-. Why not 70 GSR?

English

@Endogenous_i The higher the lease rates, the lower the gold/silver ratio. There’s plenty of gold in the world and not enough silver, so if silver rises more than gold, the ratio falls. Or did you mean something else?

English

No matter how you look at the silver price, it has to go higher.

Since Feb 9, retail investors have sold roughly 15 million ounces of physical silver. Yet the market did not get relief.

The 1 month silver lease rate is still extremely high, and the 1Y Silver Swap -Rates (%) is still extremely distorted. I call it extreme for a reason: a 1 month lease rate should round to zero, and the 1Y swap rate should always be positive.

At first glance it looks like the market is getting some breathing room because Registered silver stopped falling. Look under the hood and you see the opposite: silver is still leaving COMEX on a net daily basis.

Now ask yourself what happens when retail comes back and buys more than 15 million ounces via ETFs. Exactly: the market gets tighter than ever, instantly.

It is only a matter of time before silver prints a new all time high. This bull market is far from over.

Karel Mercx@KarelMercx

English