FN2187 retweetledi

FN2187

542 posts

FN2187 retweetledi

Listen to this video.

Change the name of JPM for their real client that is US Treasury.

English

FN2187 retweetledi

If you bought $GOLD anywhere near this topping channel, I rate this as Extremely high risk.

I've had many stop by and say we are going to pull off a 1980's style run and overshoot the topping channel.

Let's entertain this idea for a second. If we do overshoot, the horizontal Gann Level 6 at $7638 will be a formidable resistance. This is just about 50% higher.

Even the most parabolic of bull runs I've never seen break through more than 2 Levels in one bull market. The 1970's run ended exactly 2 levels higher precisely at Level 3.

This information is for your perusal as you deem fit.

P.S before breaking out of the topping channel in 1980, there was a 9% correction at the topping channel first.

English

FN2187 retweetledi

🚨 IF SILVER HITS $130, THE OLD BANKING SYSTEM WILL COLLAPSE!!

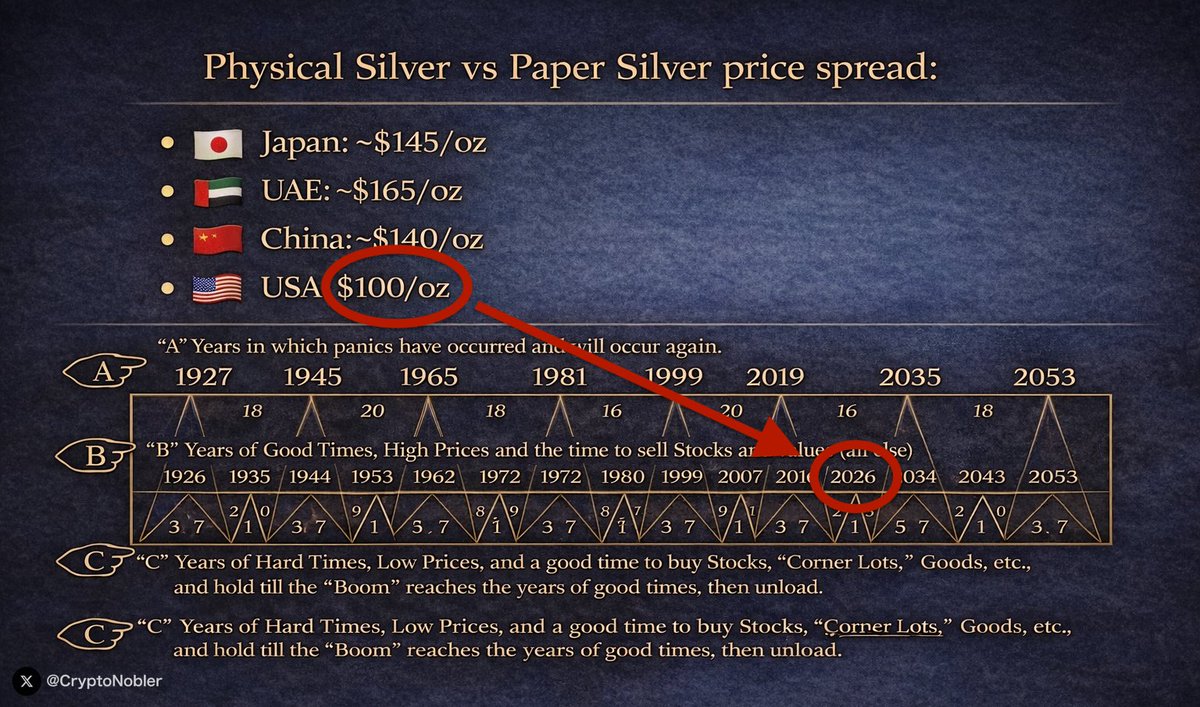

Silver just hit $100/oz for the first time in history.

But physical silver and paper silver are trading at totally different prices.

Physical vs Paper price:

🇺🇸 USA → $100/oz

🇯🇵 Japan → $145/oz

🇨🇳 China → $140/oz

🇦🇪 UAE → $165/oz

See the issue?

That’s a 45–80% gap between the paper price and where physical silver actually trades.

In a healthy market, arbitrage would close that gap fast.

The fact it hasn’t tells you one thing:

The paper market is capped.

Now ask why.

Why is COMEX suppressed?

Because bullion banks are sitting on massive net short positions.

Banks don’t need silver at $200 to blow up.

If silver reprices to where physical clears ($130–$150),

the mark-to-market losses on those shorts get ugly fast.

We’re talking billions in losses hitting bank balance sheets.

Tier 1 ratios get wrecked.

They’re not really trading silver anymore.

They’re trying to survive.

Now the endgame.

This is shaping up like a delivery squeeze.

People pull physical out of vaults.

Banks respond by printing more paper contracts.

Good money gets hoarded.

Bad money floods the market.

Eventually, registered inventory drops too low.

Delivery stress spikes.

And that’s when the system cracks - not because of price alone, but because delivery fails.

When that happens, paper prices stop mattering.

Price snaps to physical reality.

This isn’t just manipulation.

It looks like a desperate attempt to avoid a solvency event.

I’ve studied markets for over a decade and called most market tops.

Follow and turn notifications on.

I’ll post the warning before it hits the headlines.

Ignore at your own risk.

English

FN2187 retweetledi

Bitcoin is never going away.

Once something is invented, it cannot be uninvented.

Now you have 3 choices:

1) Learn about Bitcoin and develop an understanding of how it can benefit you and humanity in general

2) Ignore Bitcoin and try to avoid everything that has to do with it

3) Assume that Bitcoin won't work and bash the technology

IMO

- 5% of people choose #1

- 85% choose #2

- 10% choose #3

English

FN2187 retweetledi

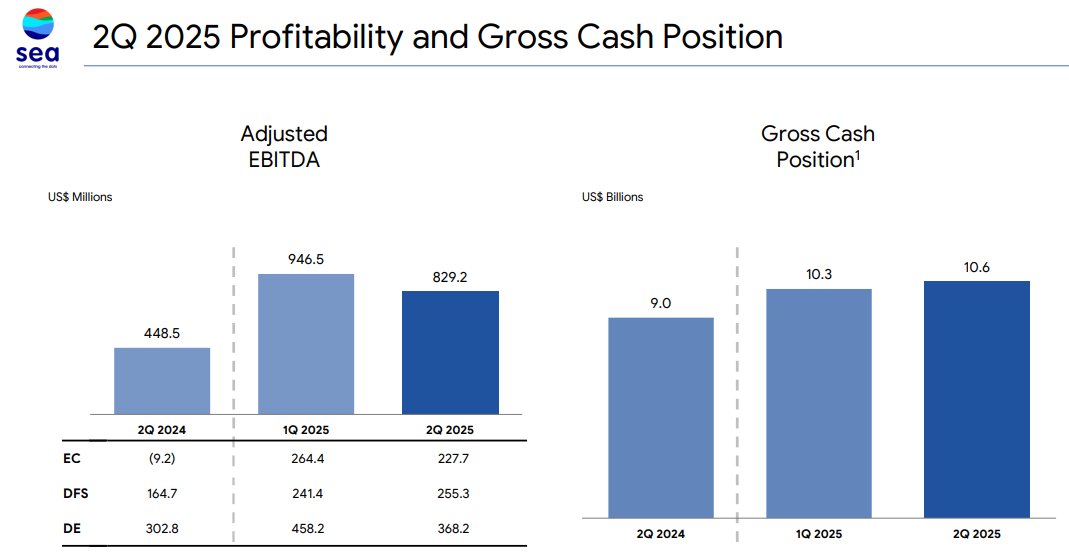

17/ Sea Limited

$SE unites three powerful growth engines.

- Shopee in e-commerce

- Garena video gaming

- Monee financial services

This AI-enhanced ecosystem delivers improved shopping, financial services, and gaming experiences. $SE leverages data and AI to engage hundreds of millions of users across the region.

For people of Southeast Asia, that means convenience, affordability, and access to services once out of reach.

For small merchants and gaming developers, it opens new markets and growth opportunities.

As the Southeast Asian booming economy leads to 200M people joining the middle class, $SE will see steady and continuous growth.

English

FN2187 retweetledi

$GRAB CEO Anthony Tan on the Vay Technology investment:

“We believe the future of mobility in Southeast Asia will be a hybrid model that relies on the expertise of our driver-partners alongside autonomous vehicles and remote driving services.

This initial investment will help accelerate Vay’s remote driving technology development and create valuable technical and operational synergies for Grab’s long-term mobility strategy.

It will also support Vay’s expansion in the U.S., where they serve a growing segment of consumers who prefer not to be car owners and are looking for more flexible, affordable, mobility options.”

English

FN2187 retweetledi

FN2187 retweetledi

BREAKING $GRAB Citing busy business Q4 season🔥

Grab, the Southeast Asian SuperApp, has been actively addressing driver supply challenges to handle peak demand during the busy Q4 season (October–December), which typically sees surges from holidays, year-end travel, and events like Christmas and New Year's. With Aggressive tourism expansion, it is estimated Grab needs 10-15% more drivers to achieve above 40% revenue growth from Q4.

~Grab partnered with GIATMARA (a Malaysian government skills agency) to offer free Technical and Vocational Education and Training (TVET) for drivers and delivery partners. Courses cover vehicle maintenance, EV basics, logistics, digital skills, customer service, and financial management.With Malaysia's festive season driving 20–30% demand spikes, this initiative accelerates onboarding for holiday surges.

~Grab Philippines and MOVE IT, in partnership with the Department of Information and Communications Technology (DICT), have opened the Asenso Center. Grab said the center will help it meet its goal of creating 500,000 livelihood opportunities for the government, having already achieved 73 percent of its target. Community merchant participation rose 30 percent year on year. Grab Philippines also

~Grab partnered with @BYDCompany to provide up to 50,000 electric vehicles (models like Denza D9, Atto 3, Seal, and M6) to drivers via fleet partners at competitive rates, including extended battery warranties and IoT integration for app features like navigation. This reduces upfront costs by up to 50% and fuel expenses, targeting 10-15% growth in active drivers across Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam.

~Ngee Ann Polytechnic (Ongoing, expanded mid-2025): Joint Driver Training program offering six-month courses on professional skills, starting June 2025. It includes career support portals for 2,000-3,000 drivers, focusing on digital roles and upskilling to retain talent and convert part-timers to full-time.

~Tourism Authority of Thailand (TAT) & Business Alliances Formed a Tourism Taskforce for airport pick-up zones, secondary city expansions, and campaigns promoting tourism. This includes incentives for drivers in high-volume areas, supporting 20%+ ride growth and recruiting via flexible hours and bonuses.

Mike@MikeLongTerm

BREAKING $GRAB MASSIVE BUY 🚨🚨🚨 13F Filing- Massachusetts Financial Services(A massive $700B Fund) started a brandnew position on $GRAB with 3,766,358 shares

English

FN2187 retweetledi

$GRAB Map is The New @googlemaps(B2B)🧵

Here is your Free.99 analysis on GrabMap, for those that selling courses for $50-$500/m, if you are using my $GRAB and other analyses, I don't ask for much, at least give me some credit/cite. And yes 99.999% of my posts are Free.99. If you want to support my work, slap the like/repost, as I don't choose to write "Grab or any Ticker is going to x10 x100-x1000" kind of threads or "mark my words" to please the X Algo. Consider Subscribe($0.33/day) if you want to support my work further and get more in-depth analyses!

TLDR: GrabMap could generate $7B-$15B a year alone for Grab B2B segment. That is why you are seeing @AnthonyPY_Tan is mad excited abt this massive opportunity. And it also significantly boost GrabAds long term globally. This precisely proved my point that, Anthony is going to expand to 5B people and we are only 14% thesis realized right now. Grab doesn't have to be just Ride-share/Delivery when expanding!

Grab , Southeast Asia's leading AI SuperApp for ride-hailing, food delivery, financial services,Tourism, Dine-Out and more, has developed its proprietary mapping platform, GrabMaps, a massive B2B revenue potential over the next long term, not just in Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, Cambodia, and Myanmar but expanding beyond SEA markets/Customers.

1. GrabMaps: A Strategic Asset

GrabMaps is not merely a technological tool but a critical component of Grab's ecosystem, powering its ride-hailing, food delivery, and financial services. Developed in-house, GrabMaps leverages data collected from Grab's vast network of driver-partners across eight SEA countries. This data-driven approach ensures hyper-local customization, addressing the unique challenges of SEA's urban environments, such as narrow alleys, informal roads, and rapid infrastructure changes.

The recent announcement of KartaCam2, an upgraded street-level imaging device, marks a significant technological advancement. KartaCam2 enhances data collection by providing higher quality images and more precise location data, which are crucial for maintaining the accuracy and freshness of maps. This breakthrough is part of Grab's broader 2025 AI push, including integrations with @OpenAI 's GPT-4o for vision-based mapping and the establishment of an AI Centre of Excellence. These innovations position GrabMaps as a formidable competitor to Google Maps, especially in regions where localized data is paramount.

2. Revenue implications long term

The expansion of GrabMaps into B2B services opens up new revenue streams, which could significantly impact Grab's financial performance over the long term. But GrabMap is a brandnew B2B product, and GoogleMap generates around $13-$20B globally.

A. Market Opportunity in Southeast Asia

~The SEA market presents a substantial opportunity for GrabMaps. The foodservice market alone is projected to grow from $223.8 billion in 2025 to $416.3 billion by 2030, indicating a robust demand for services that enhance operational efficiencies. Businesses in logistics, e-commerce, and urban planning could benefit from GrabMaps' precise mapping and navigation capabilities, potentially generating revenue through licensing fees, subscription models, and advertising.

~Grab's existing user base of over 46 million monthly transacting users provides a strong foundation for cross-selling B2B solutions, thereby increasing revenue without significant additional marketing costs.

B. Competitive Advantage of a Future $500B MC AI SuperApp over Google Map

Google Maps, while dominant, may not be as finely tuned for SEA's unique challenges. GrabMaps' hyper-local data and AI-driven enhancements offer a competitive edge, attracting businesses that require accurate and cost-effective mapping solutions.

Revenue from B2B services could include:

Licensing Fees: Enterprises can license GrabMaps' APIs and SDKs to integrate mapping functionalities into their operations.

Subscription Models: Continuous updates and premium features could be offered on a subscription basis.

Advertising Revenue: GrabAds, which leverages mapping data, could generate additional income through targeted advertising.

C. Global Expansion is Inevitable

~The partnership with Tino in Mongolia is a strategic move to scale GrabMaps internationally. This marks Grab's first major mapping partnership outside SEA, indicating potential for revenue growth in other regions where Google Maps' dominance is less entrenched or where local data needs are acute.

~The use of IoT devices like KartaCam2 and KartaDashCam for real-time data collection could further enhance GrabMaps' value proposition, potentially increasing revenue through premium service offerings in new markets.

D. Synergies w/ other businesses

Grab's ecosystem approach allows for synergies between GrabMaps and other services like GrabPay, GrabFood, and GrabTransport. For example, businesses using GrabMaps for logistics could also adopt GrabPay for transactions, creating a revenue multiplier effect.

3. Google Map Revenue in Asia

~Total Revenue in Asia-Pacific (2018): Google APAC, based in Singapore, reported $20.24 billion out of the total $21.37 billion revenue in the Asia-Pacific region. This indicates that a significant portion of Google's revenue in Asia is attributed to Singapore, likely due to its role as a hub for Google’s operations.

~Advertising Revenue: In 2018, Google APAC generated $15.8 billion from advertising alone, compared to $4.4 billion from other activities like Google Play. Advertising on Google properties, including Google Maps, is a major revenue driver.

~Market Share in Search Marketing: Google Maps holds a 62.34% market share in the search marketing category, competing with tools like Wix (26.54%) and Google Ads (4.14%). This dominance suggests that a considerable portion of Google’s advertising revenue in Asia is linked to mapping services.

For the full fiscal year 2024, Alphabet (Google's parent company) generated $56.82 billion in revenue from the Asia-Pacific (APAC) region. This represented approximately 16.24% of the company's total revenue for the year.

If we take a conservative estimate at 25% of $56.82B of Google's total advertising revenue in Asia is related to mapping services= $14.2B.

=> If GrabMaps secures even 50% of this market share in SEA, it could generate around $7B annually from this segment alone.

GrabMap is 4x lower error rate, 10x lower latency, 75% fewer mapping mistakes, and much cheaper than GoogleMap. With @OpenAI GPT-4o fine-tuning, GrabMaps hit 80% accuracy for speed limits and lanes13-20% above prior levels excelling in occlusions ( rainy monsoons) where Google relies more on satellite data.

Now do you understand why Google and HSBC are clapping $GRAB on search and downgrade? Yes, because GrabMap is a massive threat and Grab @AnthonyPY_Tan refused to buy $goto since 2020.

Conclusion:

Grab's expansion of GrabMaps into B2B services represents a strategic move to challenge Google Maps' dominance in Asia, particularly in SEA and future expansion. The revenue implications are substantial, with potential gains from licensing fees, subscription models, advertising, and international expansions. While Google Maps generates billions in revenue, primarily through advertising, GrabMaps' localized and AI-enhanced approach could carve out a significant niche, especially in regions where precise, real-time mapping data is critical.

The success of this strategy will depend on Grab's ability to scale internationally, maintain technological superiority, and effectively monetize its B2B offerings. However, the opportunity is clear, and Grab's ecosystem approach positions it well to capitalize on the growing demand for advanced mapping solutions in a rapidly digitalizing world. This move not only enhances Grab's revenue potential but also solidifies its role as a key player in the global tech landscape.

Not Financial Advice!

Source: Grab Dot Com.

Mike@MikeLongTerm

BREAKING $GRAB Breakthrough on GrabMap🔥🔥 To learn more: Tue, 28 Oct, 2025, 10:00 AM - 12:00 PM (GMT+8.0) AI Centre of Excellence Lab Crawl 3 Media Close, Singapore 138498, (At MPH C) Grab Holdings Limited, Southeast Asia's leading AI SuperApp for ride-hailing, food delivery, financial services, and more, has developed its proprietary mapping platform, GrabMaps, as a critical in-house technology to power its ecosystem. Unlike many competitors that rely on third-party maps like @Google Maps, GrabMaps is built from the ground up using data collected from Grab's vast network of driver-partners across eight countries (Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, Cambodia, and Myanmar). This approach not only reduces dependency and costs but also enables hyper-local customization for Southeast Asia's complex urban environments, including narrow alleys, informal roads, and rapid infrastructure changes. Grab today announced a breakthrough on GrabMap, "KartaCam2", the rollout and enhanced capabilities of an upgraded street-level imaging device.KartaCam2 enables "saving higher quality images and more precise location data for mapmaking," positioning it as a significant advancement in data collection for mapping. GrabMap is expanding its AI-assisted mapping and IoT sensor technologies beyond Southeast Asia. Titled around the partnership with Tino (Mongolia's pioneering superapp), the announcement details deploying GrabMaps' advanced toolkit including upgraded IoT devices like KartaCam 2 and KartaDashCam to map Ulaanbaatar and beyond. This marks Grab's first major international foray for GrabMaps, leveraging AI for automated data extraction and IoT for real-time sensor fusion. The post traces the evolution from "store-bought cameras on motorcycle helmets" to a "suite of cutting-edge mapmaking tools and tracking IoT devices," emphasizing continuous delivery of superior SEA-centric data now scaled globally. This breakthrough aligns with Grab's 2025 AI push, including GPT-4o integrations for vision-based mapping and the AI Centre of Excellence launched in May. It's especially timely amid rebounding tourism (projected 25% YoY growth in Mongolia/SEA) and Grab's Q3 earnings focus on tech efficiencies. Full event link: gevme.com/lab-crawl--gra…

English

FN2187 retweetledi

Sea Limited: The Amazon Of Southeast Asia With Room To Run

( $SE Rating: By) | By Talha Quraishi

When I first traveled across Southeast Asia a few years ago, I noticed something striking whether it was Jakarta, Bangkok, or Manila, everyone seemed to be scrolling through the same orange app. That app was Shopee, the beating heart of Sea Limited $SE.

It wasn’t just another e-commerce platform; it was a digital lifeline for millions of small merchants and consumers. Fast forward to today, Shopee has cemented itself as the undisputed e-commerce leader in the region, commanding over 50% market share in nearly every Southeast Asian country a feat that even Alibaba’s Lazada and TikTok Shop can’t come close to matching.

But what truly fascinates me about Sea isn’t just its dominance it’s how this company has quietly positioned itself as the Amazon-meets-Tencent of emerging Asia, blending e-commerce, gaming, and digital finance under one roof.

Near-Term Prospects: A Market Still in Its Adolescence

Southeast Asia’s e-commerce story is still being written. Despite rapid adoption, online retail penetration remains around 20%, far below the 25–30% range in the U.S. and China. In other words, there’s still a lot of headroom for Shopee to grow before this market matures.

The region’s digital economy is expanding at a double-digit pace, fueled by smartphone ubiquity, logistics improvements, and young, mobile-first consumers. With roughly 15% CAGR growth in B2B shipments and internet usage barely above 60% in countries like Cambodia and Laos, the structural runway is enormous.

That’s why I view Sea as a long-term proxy for Southeast Asia’s internet boom a multi-decade wave of digitization, logistics buildout, and consumption growth that’s still in its early innings.

Sources of Sea’s Competitive Strength

What truly sets Sea apart, in my view, isn’t just its scale it’s its cultural fluency and operational localization.

Sea has built a playbook around understanding local nuances. Every Shopee app across Southeast Asia is customized for that specific market from user interface language to payment options and promotions tied to local holidays. That deep localization creates a sense of familiarity that foreign competitors often miss.

Then there’s Garena, Sea’s gaming arm. It’s not merely a game publisher it’s a regional gateway for global developers, handling everything from localization and server hosting to payments. Its flagship title, Free Fire, became a cultural phenomenon in Southeast Asia not because it had the best graphics, but because Garena understood what the market valued: low data usage, quick matches, and community engagement.

Finally, Sea’s ecosystem approach gives it a moat. ShopeePay and SeaMoney integrate seamlessly across the platform, reducing friction and enhancing loyalty. Combine that with Shopee’s proprietary logistics network and you have an Amazon-style “flywheel” one that turns faster the more users engage.

This local-first, integrated model is why Sea survived years of losses while competitors stumbled. It’s not easy to replicate.

Growth: From Scale to Sustainability

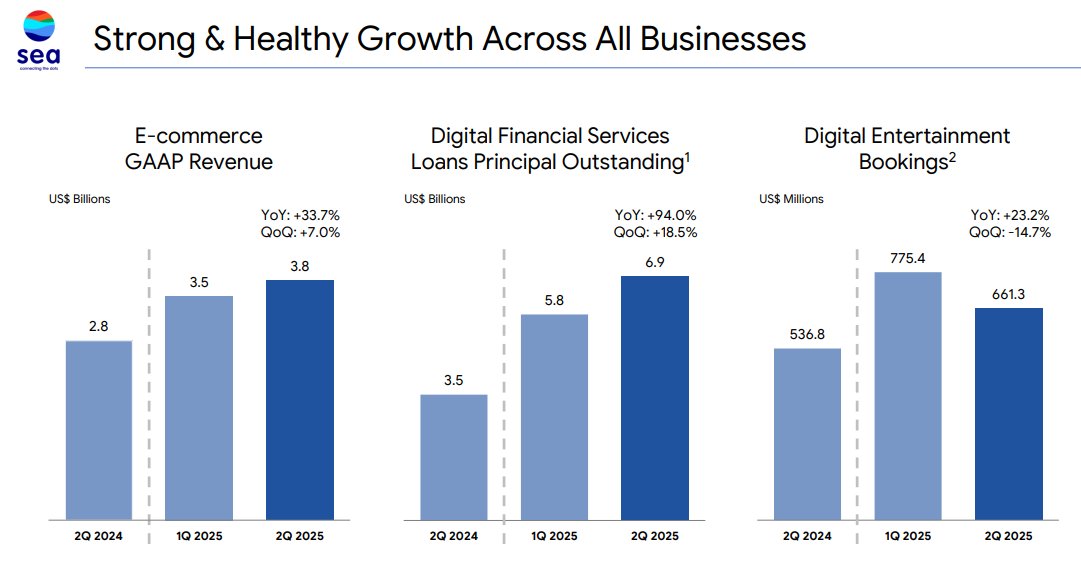

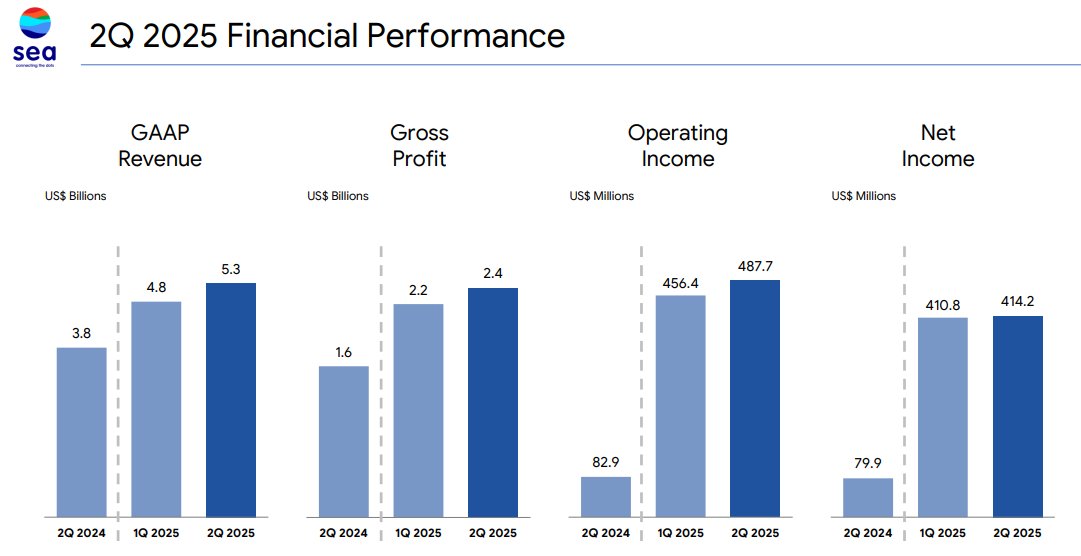

Sea’s financials tell a story of resilience. In the past 12 months, revenue grew 34%, operating income soared 149%, and operating cash flow climbed 132%. Those aren’t one-off numbers; they reflect a company transitioning from growth-at-any-cost to profitable scalability.

Yes, much of its past profit metrics were “non-meaningful” because Sea only recently swung into the black but that’s precisely the inflection point I like to see as an investor. Moving from negative to positive earnings isn’t just accounting math; it’s proof that the model now works at scale.

With e-commerce penetration still shallow, and internet connectivity broadening every year, I see a long runway ahead. In essence, Shopee’s best growth days might not be behind it they could just be starting to normalize into profitability.

Profitability: From Loss Leader to Cash Generator

Sea’s turnaround from a money-burning disruptor to a disciplined operator has been remarkable. The company now posts a 45% gross margin, 7.5% EBIT margin, and 6.2% net margin. Its return on equity (14.5%) and return on capital (7.2%) underscore a meaningful improvement in efficiency.

These aren’t astronomical numbers yet, but they’re directionally encouraging. What’s important is the trajectory every quarter, Sea is learning to do more with less. The free shipping blitzes that once crushed margins are now more targeted, supported by data-driven logistics and higher average order values.

In other words, Sea is no longer buying growth it’s earning it.

Valuation: Expensive or Early?

Here’s where many investors hesitate. At 61x earnings, 5.6x sales, and 10x book value, Sea doesn’t screen as cheap. But valuation alone doesn’t tell the full story.

For one, Sea is still in the early stages of profitability earnings are ramping, and high multiples naturally compress as profits scale. We saw the same pattern with Amazon and MercadoLibre during their transition years.

Second, Sea’s growth velocity and regional dominance justify some premium. When you control over half of Southeast Asia’s e-commerce traffic and have a growing fintech arm on top, you’re not just another online retailer you’re a digital infrastructure play for an entire region.

I’d argue that Sea’s valuation reflects potential energy more than froth and that’s often where long-term compounders are born.

Risks: Competition and Expansion Missteps

Of course, no investment is without risks. Shopee’s success has invited a surge of competition especially from TikTok Shop, which is aggressively subsidizing sellers. If rivals replicate Shopee’s early playbook of discounts and free shipping, customer retention could be tested.

Another concern is geographic overreach. Sea has tried to expand into markets like Brazil, but its progress there lags far behind MercadoLibre $MELI and Amazon $AMZN. Scaling beyond its cultural comfort zone could stretch management bandwidth and capital.

Finally, regulatory scrutiny around online lending and digital wallets could pressure its fintech margins, especially as Southeast Asian governments tighten oversight on digital transactions.

That said, Sea’s operational discipline and local know-how give it more levers to adapt than most competitors. The company has already proven it can pivot and survive through market cycles.

Bottom Line: A Long-Term Compounder in an Underpenetrated Region

Sea Limited isn’t just an e-commerce company; it’s a regional ecosystem that touches logistics, payments, and entertainment. The company has graduated from blitz-scaling to building a sustainable, profitable engine one that mirrors Amazon’s evolution in the 2010s.

The numbers suggest the turnaround is real. The market potential suggests it’s durable. And the local edge suggests it’s defensible.

At current levels, I see Sea as a high-quality compounder in one of the most promising digital economies in the world. It won’t be a straight line competition and volatility will test investors but over the long haul, I believe this is one of the few Southeast Asian names capable of scaling globally while maintaining profitability.

In short: Sea’s tide is rising again — and this time, it looks sustainable.

English

FN2187 retweetledi

FN2187 retweetledi

$GRAB is one of my highest conviction picks today.

In this deep dive article, I explain why.

You can access it through this link 👇🏻

rscapital.substack.com/p/a-deep-dive-…

Deep dive articles take 100+ hours to write, so I would appreciate a like, share, and subscribe.

Thank you and enjoy!

English

FN2187 retweetledi

Bitcoin July close RSI = 72.5 .. solid uptrend🚀

My analysis in this video: m.youtube.com/watch?v=hH5dJI…

English

FN2187 retweetledi

$MSTR is Amplified Bitcoin.

$STRK is Structured Bitcoin.

$STRC is Treasury Bitcoin.

English

FN2187 retweetledi

BREAKING: THE PRESIDENT OF THE UNITED STATES JUST POSTED A 3 MINUTE EXPLANATION OF #BITCOIN ON SOCIAL MEDIA

ABSOLUTELY EPIC 🔥

English

FN2187 retweetledi

Being a Bitcoiner is waking up every morning thinking:

“How can I explain to everyone I love that the entire global monetary system is a parasitic hallucination designed to extract their life energy and that hope exists in a cryptographic number embedded in an orange coin on the internet?”

English

FN2187 retweetledi

วันหยุดแต่เราทำงาน เจอกันในถกไม่เถียง วันนี้เวลา 17.20 ค่ะ มีหลายเรื่องราวจากเวทีคุณทักษิณเมื่อคืน

ไทย