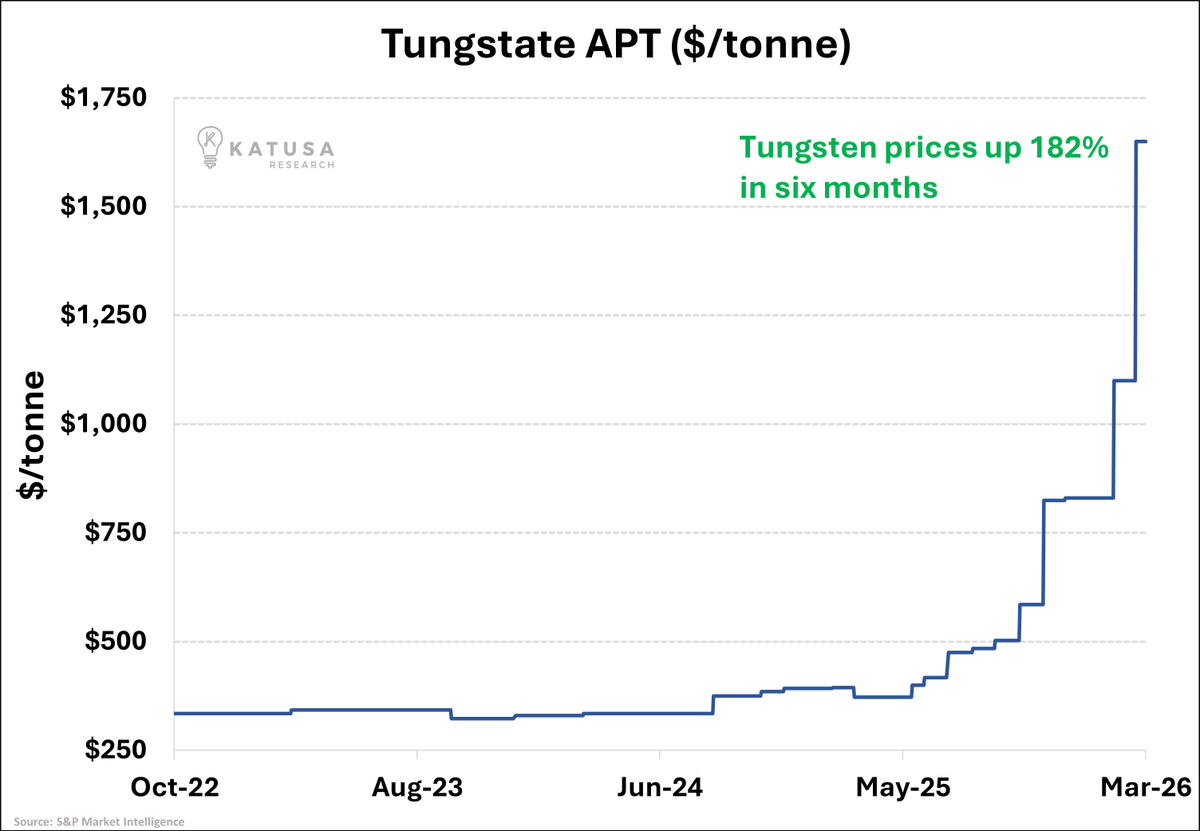

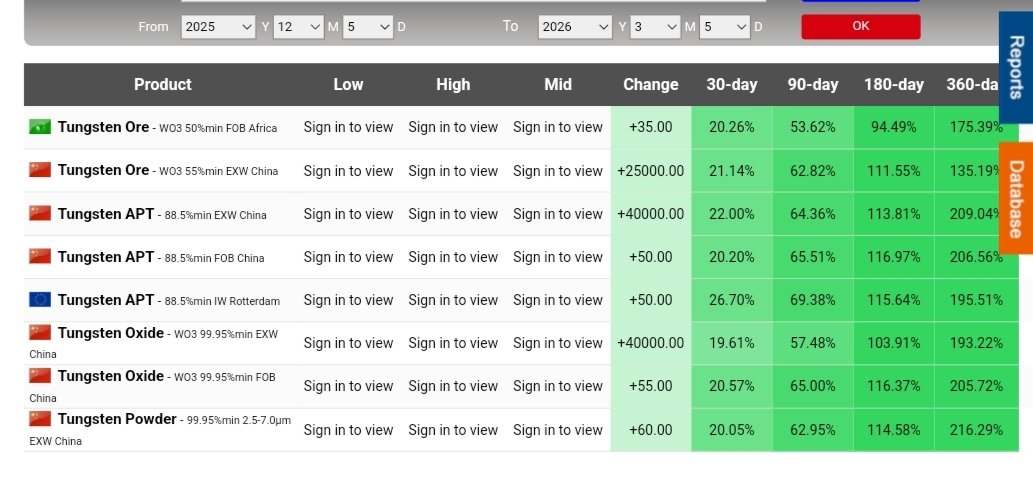

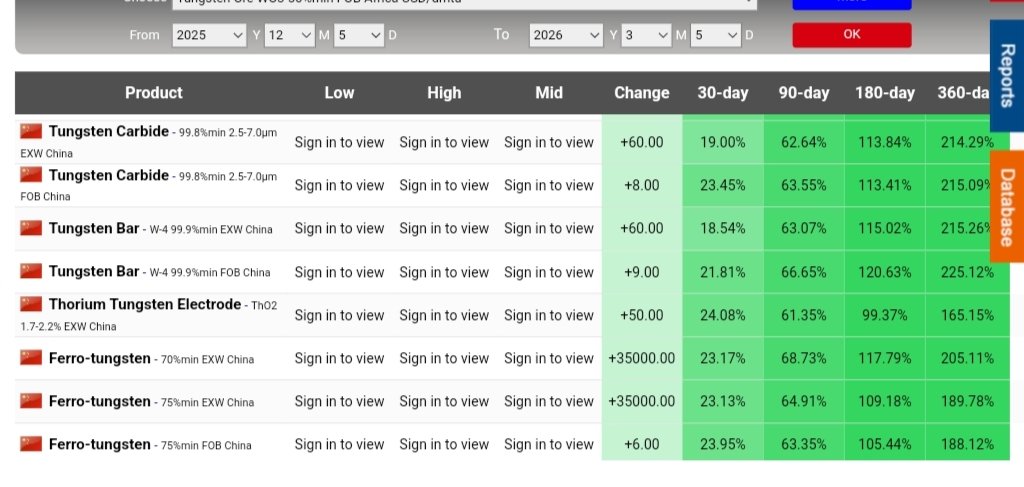

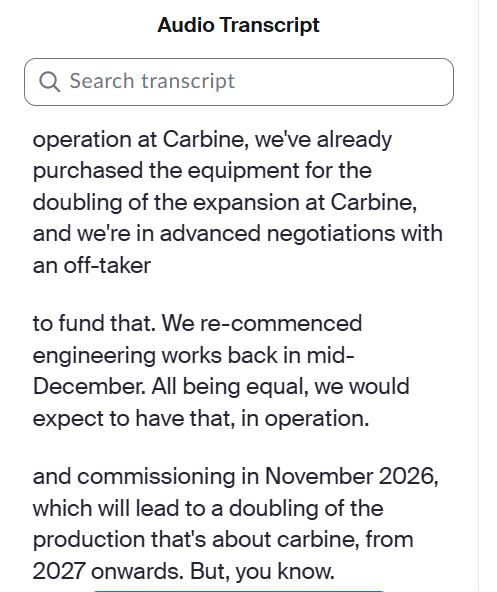

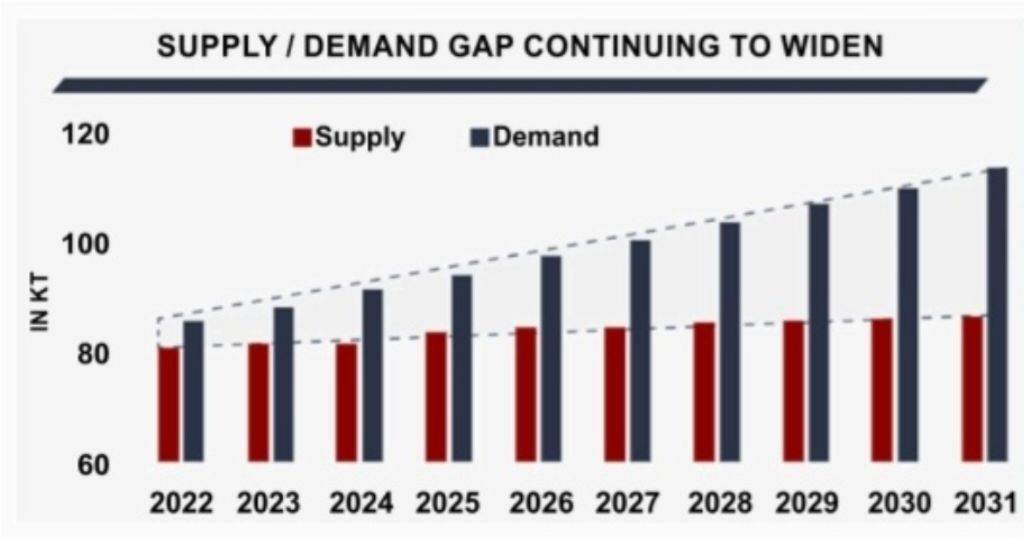

I have been seeing a lot of talk about $EQR.AX and once you dig into it the excitement makes complete sense. It is a tungsten mining company. Two operating mines. Mt Carbine in Far North Queensland and a second asset in Spain. Trading at A$0.30. Market cap A$1.6 billion. Backed by Oaktree Capital. Here is why tungsten is the most important commodity most investors have never thought about. China controls 79% of global tungsten production. In early 2025 they imposed export controls. By early 2026 exports dropped to effectively zero. China is now a net importer of tungsten for the first time ever. The supply backstop that capped the price in every previous cycle is permanently gone. APT price early 2025: $320. APT price today: approaching $3,000. A near 10x move in roughly a year and nobody is talking about it. The Iran war poured fuel on it. Tungsten is the metal inside armor-piercing tank rounds. Every round fired is tungsten that does not come back. Rheinmetall targeting 1.1 million shells by 2027. US Army targeting 100,000 rounds per month. None of it gets recycled. Supply gets permanently consumed. Then there is the January 2027 DoD procurement ban. Chinese and Russian tungsten banned from all US defense contracts from that date. Western production becomes legally mandated. $EQR.AX is one of two meaningful western tungsten producers in the world. 2026 production target: 3,000 to 4,000 tonnes. At current APT prices the revenue math is extraordinary relative to the market cap. Its closest peer ran 840% last year and trades at 8x the valuation of $EQR.AX on similar production numbers. A $0.30 stock. Operating mines. Production ramping. DoD mandate incoming. The tightest commodity market in a generation.