Alidemi retweetledi

Alidemi

132 posts

Alidemi retweetledi

Alidemi retweetledi

Alidemi retweetledi

English

$INFQ 가 상장하고 맥을 못 추고 있는데요,

기술이 흥미롭기에 아티클 만들어보려고 합니다.

Chip scale의 Integarted Photonics 기술을 활용한 회사라 더욱 관심이 가기에요,

주말 안으로 완료하여 포스팅 해보려고 합니다.

혹시라도 읽어보고싶은 분은 "Notify" 설정을 해두시거나, 댓글에 간단한 메세지 남겨두시면 제가 아티클 작성 이후 mention 드리겠습니다.

Mooni Insight 💫@Semicon_player

@PhotonCap 양자 센싱 시장에 대해서 아티클 부탁드립니다 🥰 이 영역은 왠지 쏘니 주력 일것 같습니다. 앞으로 시장도 기대가 크구요 특히 방산쪽에서요

한국어

@BoringBiz_ The timelines are wrong for sure, but the long-term view of things has a strong possibility of being right.

English

Exactly my thought as well

2028 will roll around. Not a single thing that was said in that article will have happened

Everyone will look back and laugh at the fact that the market sold off some of the greatest companies ever built off a random thought article

Greatest market ever to be a stock picker

As much as I hate the phrase, the baby is literally being thrown out with the bath water

If you care enough to do your own research, you can pick up incredible assets at some of the lowest multiples in many years

Pratyush@pratyushbuddiga

Whenever this cycle ends, the Citrini “report” will be an extremely funny relic of the mania like a Bored Ape or Peloton’s stock chart. The DoorDash analysis is a third grader’s understanding of marketplaces.

English

Alidemi retweetledi

Alidemi retweetledi

@TradexWhisperer RAM is cyclical, you fucking idiot. Historically, it has a high P/E when the price is low and vice versa. Yes, this time ram is different but doesn't make it untrue

English

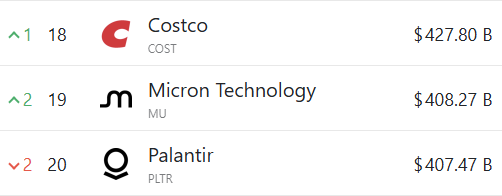

$MU Micron is now the 19th largest company in the US, bigger than $PLTR

Yet it trades at one of the lowest forward P/Es:

Palantir: 170x

Costco: 46x

AMD: 34x

Micron: 9.6x

Memory sits at the very heart of AI growth and we're still very early in this revolution.

Trade Whisperer@TradexWhisperer

$MU Bargain of the Century PE Ratio: 15.5 Sales Ratio: 2.33 50% Increase in HBM (AI Memory) Sequentially. DRAM/NAND prices are surging.

English

Alidemi retweetledi

The software (SaaS) sector is facing an "Apocalypse". leaders like Salesforce ($CRM), ServiceNow ($NOW), Veeva ($VEEV), and Constellation Software ($CNSWF)are down 40% to 50% from their highs over fears "Agentic AI" will eat their lunch by automating the very tasks these platforms manage.

However, history suggests that markets repeatedly declare industries "dead," only to realize later that incumbent leaders are far more adaptive than expected.

Before selling in panic, remember times when the market predicted a "Kodak moment" and was wrong:

1) The "Death of Retail" (2015–2016):

Investors feared Amazon would make physical stores obsolete. Instead, leaders like Walmart and Target integrated the threat, using stores as "edge warehouses" for same-day pickup (BOPIS). Both eventually hit all-time highs.

2) The Cloud vs. On-Premises Crisis (2010–2012):Markets assumed legacy giants like Microsoft and Adobe were finished when AWS took off. They pivoted to SaaS models and captured the majority of the cloud's value, becoming the best-performing stocks of the decade.

Why Agentic AI is a Catalyst, Not a Killer for SaaS Leaders

The market currently overestimates the speed of

disruption and underestimates incumbent adaptation.

SaaS giants are already pivoting away from human seat licenses to Outcome-basedpricing.

Software Leaders are Adapting and Integrating Agentic AI into their Revenue Models

They are moving away from "per-seat" pricing to capture the value of automated "digital labor".

1. Salesforce ($CRM): Introduced Agentforce with a "Flex Credit" model. Instead of just seats, they charge roughly $0.10 per action. If an AI agent does 5x the work of a human, revenue can actually double per unit of work.

2. ServiceNow ($NOW): Using a "Pro Plus" SKU with a 30%+ premium to unlock "Now Assist". They are betting on "Agentic Fabric," where AI agents talk to each other across departments—a complex workflow startups can't easily replicate.

Bottom Line:

Markets systematically underestimate switching costs and regulatory friction. While the "Software Apocalypse" narrative is loud, the "SaaS Pivot" to AI agents may actually make these platforms more indispensable and more profitable.

English

Alidemi retweetledi

Alidemi retweetledi

Alidemi retweetledi

Alidemi retweetledi

251124_Multi-year Demand Visibility Supports Structural Growth Outlook; Raise TP to W830k – CITI

[Key Takeaways]

(1) Multi-year demand visibility supports SK Hynix’s structural growth. TP raised from 770,000 won → 830,000 won.

(2) Despite extremely strong demand for server DRAM and eSSD for AI inference, the memory market’s supply shortage is expected to deepen as suppliers focus CAPA expansion almost entirely on HBM.

(3) Global DRAM/NAND ASP growth forecasts are raised from YoY +37%/+39% to +53%/+44%. As a result, SK Hynix’s 2026 OP is revised up by +12%.

⸻

[Contents]

(1) We expect that in 1H26, global commodity memory supply will fall short of total demand based on *FPO, and will be able to meet only about 60% of total demand.

*Firm Purchase Order

(2) The remaining 40% of customers will not receive supply, and we believe they will move to secure memory chips—paying higher premiums if necessary—to avoid supply disruptions.

(3) Moreover, since next year’s capacity additions are almost entirely focused on HBM, global DRAM ASP in 2026 is expected to increase YoY +53% [previous +37%], and NAND ASP to increase YoY +44% [previous +39%].

(4) As highlighted at Citi Korea Corporate Day, we believe SK Hynix’s demand visibility has expanded to as much as 2–3 years, compared to the 2017–18 memory upcycle.

(5) Even for commodity DRAM, major customers have already been allocated CAPA based on FPOs, and some customers have even communicated purchase intentions for 2028 volumes in advance.

(6) With server DRAM/HBM accounting for 80% as of end-3Q25, the volatility that used to arise from consumer-facing memory has also been significantly reduced.

(7) We believe the memory market has entered the early stage of a structural upcycle driven by the explosive increase in data/tokens generated by AI inference demand.

(8) Reflecting our DRAM/NAND outlook, we revise up SK Hynix’s OP forecast by +12%, and apply 3.3x to 2026(F) BVPS, raising our TP to 830,000 won.

English

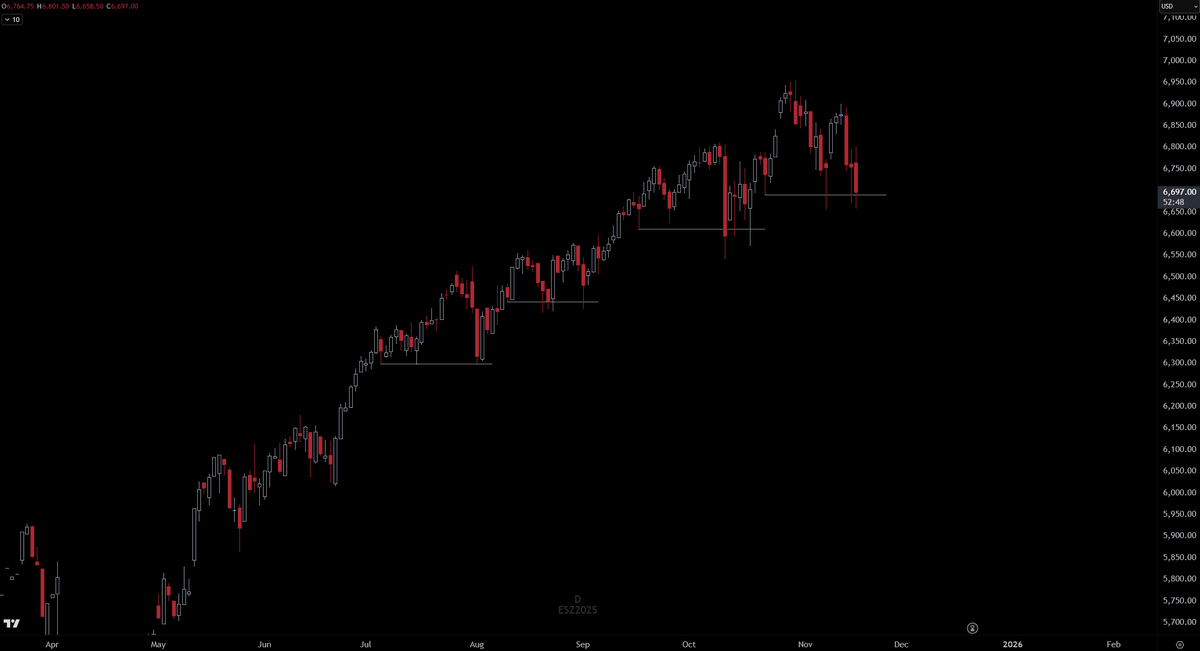

@Crypto_Chase After the dump today, it is at a support level, but the fact that it broke the EMA 50, which it regained in May of this year, suggests to me that the correction will likely continue. Macro also doesn't help.

English

Alidemi retweetledi

Alidemi retweetledi

Are you sure Peter Thiel runs your streets, white boy?

English

Alidemi retweetledi

Sometimes, we see bubbles.

Sometimes, there is something to do about it.

Sometimes, the only winning move is not to play.

English

Alidemi retweetledi