GiuGiu

1.3K posts

GiuGiu

@GiuGiust

An open forum on investment theory, italian food and coffee

Katılım Aralık 2013

409 Takip Edilen110 Takipçiler

Not even SaaS is performing this poorly

unusual_whales@unusual_whales

BREAKING: OpenAI recently missed its own targets for new users and revenue, per Bloomberg.

English

@Brian_Stoffel_ @AbbasR87 This reminds me of the transition from point of sale software to the SAAS model. These transitions are always rocky

English

@AbbasR87 Absolutely correct.

The point is, you have to see how fast the:

👇 high-margin side (seat-based) is decelerating

and weigh it against how fast the:

👆lower-margin side (usage-based) is accelerating

English

A little back-of-the-envelope $NOW math:

If we strip out Armis and Moveworks, assume $280 M in NowAssist revenue in 2025, and $1 billion in 2026

Traditional, seat-based revenue (constand currency) is only expected to grow 13% in 2026.

Before 2025, was always 20%+

English

An episode on Fairfax would be interesting. Especially on why you think the company has fundamentally changed and the narrative that they are only doing well because this is a “insurance hard market “ and not due to any fundamental change in the company which is many people’s view

English

recording a podcast soon - anything you want us to talk about? @ErnestWongBWM

English

@CapexAndChill How is it long term focused to cut and run on logistics and distribution. He talks of the 100 year company but Meli walks the walk

English

Just finished listening to this awesome interview with Tobi Lütke, the CEO of $SHOP. If you love how $MELI's management is highly reactive and long-term focused, you will enjoy studaying Tobi. He runs Shopify with a very singular, engineering-driven mindset.

Tobi talks about how he almost killed Shopify by trying to act like a traditional corporate executive. He was trusting the process too much and delegating poorly. When COVID hit, he did a massive reset. He reviewed every single project himself, canceled ~60% of them, and turned over his entire executive team. He replaced them with former founders because founders do not settle. They have a natural irritation for bad products. He stopped managing the company and started engineering it.

This is a massive mental model shift. Tobi hates competitive analysis because it just leads to mimicry. You do not create a masterpiece by copying a competitor. Instead, he treats others as rivals. Rivalries inspire you to push your own boundaries. It is exactly like the current battle in Brazil with Shopee fighting MercadoLibre for parcel volume dominance. $MELI thrives because that intense rivalry forces them to innovate from first principles, rather than just copying a playbook. Tobi views e-commerce the exact same way. He demands differentiation.

When Shopify stock dropped 80% a few years ago, Tobi did not panic. He looked at the core incentive issues and restructured compensation completely. Instead of rigid corporate plans, he built an internal system with sliders. Every quarter, employees choose their own mix of cash, RSUs, and stock options. It gives the team full agency. This filters out the corporate climbers and brings in high-agency people who want to build long-term value.

Tobi has absolutely zero nostalgia for his past success. He writes hit pieces on his own past work 🤣. He actively roasts old systems and code so his team feels no emotional attachment to them. The sunk cost fallacy kills corporate growth. Tobi kills the sunk cost fallacy by making sure his team feels free to tear down old ideas to build better ones.

You want to own businesses where the founders treat the company like an active simulation. They constantly tweak the inputs, adapt fast, and obsess over the details. They do not care about industry standards. That is where true long-term compounding lives.

English

@MoS_Investing @TimothyBuffett Yeah. What happens when his appendix bursts or he breaks a leg surfing. These rules work only because you got a pile of cash cushion to fall back on. These rules rest of us keep grinding

English

@TimothyBuffett these things are said by multimillionaires to gain favor. he owns many fancy ass things.

English

@EricBalchunas @TrungTPhan How do you stay belted for random turbulence?

English

@TrungTPhan Yeah, but you have to pay for three seats? At what point is just cheaper to fly business?

English

Holy crap.

United Airlines now sells entire 3-seat rows in economy that can turn into a bed. Can’t imagine any parents with kids under 5 picking another airline if given choice.

United Airlines@united

The entire row is alllllll yours. Welcome to United Relax Row, three adjacent United Economy seats with adjustable leg rests that can each be raised or lowered to create a cozy lie-flat space for stretching out... You'll also get a mattress pad, blanket and two pillows. If you’re traveling with kids, a plushie too! United Relax Row will be available starting next year on more than 200 of our 787s and 777s, each with up to 12 of these brand-new rows. united.com/Elevated

English

@DrewCohenMoney Honestly in 20 years of investing this company has almost every red flag for a bad investment and it’s hard to ignore this

English

Not the clearest quote from Alex Karp, but what he is getting at I think is very important.

My read of this is that the real value creation with AI will flow to the chip makers and then the layer that sits on top of the AI models

The AI models themselves will be commoditized.

We can look at what is happening with Anthropic being pulled from government work as a supply chain risk as a case study.

While $PLTR wasn't immediatly able to swap out the models, they are already replacing Anthropic with OpenAI for government work after it was deemed a "supply chain risk" by the U.S. government.

Maybe Anthropic's Claude was ahead of OpenAI, but the difference wasn't so large that is they can't accomodate a model swap.

And while the dispute was more to do with ideology than economics, the same thing can play out in economic discussions in the future.

This will really limit the AI model providers pricing power so long as there isn't one clear winner.

The AI models can still make a margin (like AWS, GCP, Azure all do), but it greatly reduces their leverage in pricing negotiations.

English

@DrewCohenMoney Prem Watsa thought it was a steal because it was selling at book value. People were thinking that you could not get real work done on an iPhone and that a keyboard was necessary for a serious business device. The app economy was not a thing yet

English

Seeing a lot of people compare software companies that are down a lot to BlackBerry

Just curious, anyone actually know what BlackBerry investors thought at the time?

I know Steve Ballmer was famously dismissive of the iPhone, but were investors too?

English

@GiuGiust @CapexAndChill Not really. The only difference is accounting. You could own 10% and consolidate the financials if you have the votes.

English

$CSU's Q4 earnings call revealed their new capital deployment strategy referred to as "permanent engaged minority shareholder". Instead of buying entire businesses, they will buy minority stakes in public companies, hold the shares forever, and actively help govern them. The first big investment using this strategy is in Sabre. Management promised they are using the exact same return standards for these minority investments as they do for their traditional buyouts.

Management also stated their real long-term advantage is their deep customer relationships, exclusive data, and specific market knowledge.

The board decided against a stock buyback program because they still see plenty of highly profitable ways to invest their cash, which should be good news.

CapexAndChill@CapexAndChill

The actual engine for $CSU is doing well, with Q4 operating cash flow jumping 16% to $788 million and they deployed over $1.5 billion into acquisitions throughout 2025. There is still a tail risk of the Optimal Blue antitrust lawsuit but looks like business as usual.

English

@DukeInShadows Berkshire owns a small railroad I think. Also a few other businesses

English

@CJ0pp3l_Sub What was total percentage return for 2025? Many high quality portfolios are flat for the year and I’m in that bucket

English

What’s one thing you spent over $1,000 on and didn’t regret for a second?

English

Do you have any concerns that the buildout of infrastructure in data centres could result in a bust with BN holding the bag. Lots of money being spent here but return on capital for AI is not clear for the end users and this could mothball a lot of these data centres with mass bankruptcies even though they may later turn out to be required in 5-10 years

English

@TheDrugMoney You can have the best coffee machine, but it’s the beans that make the brew.

English

This beautiful latte cost me about $1.28 to make.

You can have as many as you want, whenever you want.

Making great coffee at home might just be the best investment you’ll ever make.

English

@TheDrugMoney Make sure you include accurate depreciation costs on the equipment and cleaning and maintenance costs

English

@BrianFeroldi This strategy works best with a guard rail of 3% as well as absolute dollar limit. If one stock in the portfolio goes up 10x then the 3% becomes a lot of cash to put into one position especially if that 10x later crashes down to a 3x

English

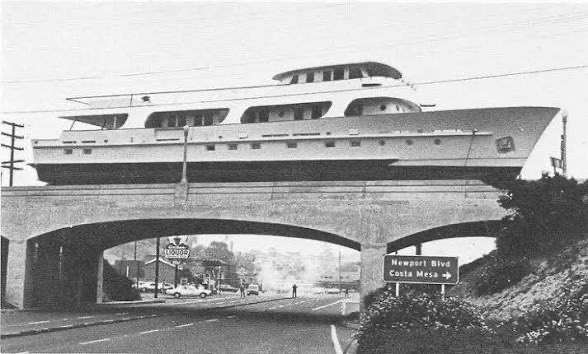

@trengriffin That $2 million stake in the company would be worth $70 million today. Nice boat though

English

1/ Harry See bought the Silverado with some of the money Warren Buffett paid for See's Candy. Two years after its 1974 launch the yacht was for sale for $2 million. The available buyer Max Wyman only wanted to pay $1 million (which was lot of money then).

English

@sidecarcap Clearly he didn’t understand the ChatGPT/AI rebubble trade

English

“You don’t have to make it back the way you lost it. In fact, it’s usually a mistake to try to make it back the way you lost it.”

English