顺丰速运🧙

1.2K posts

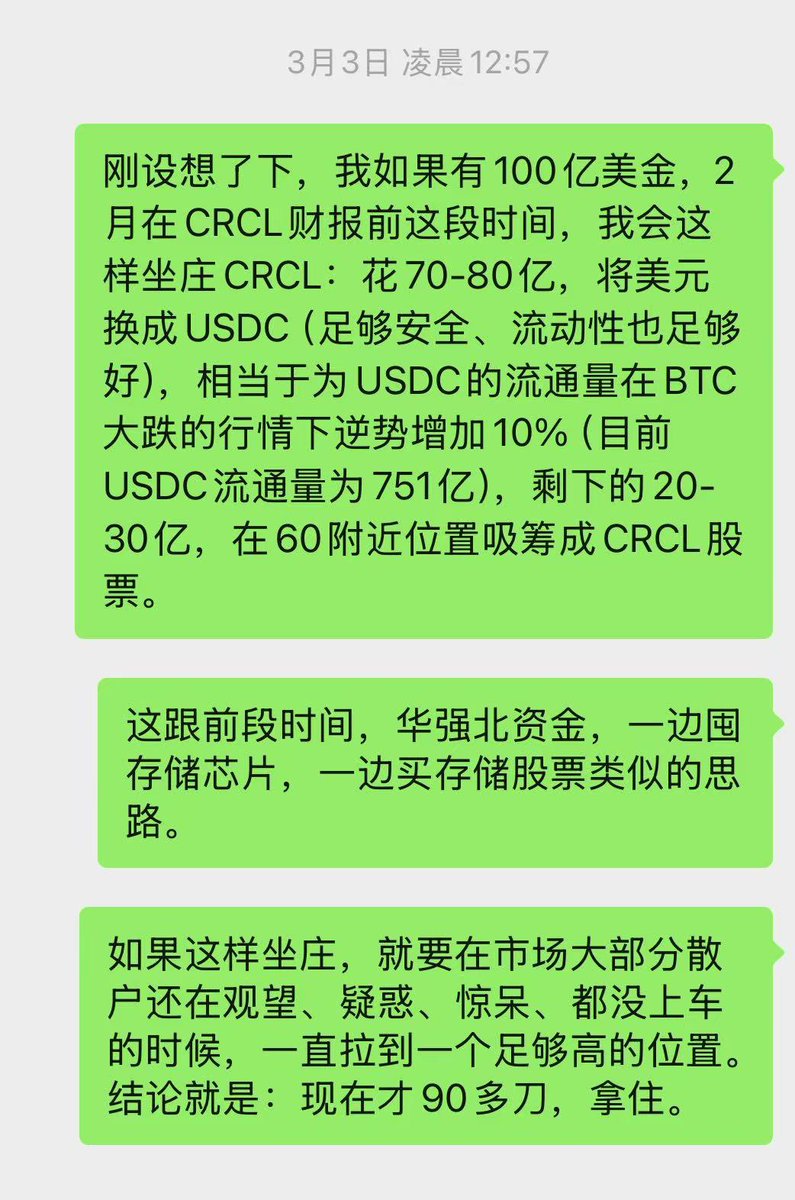

@Hoyooyoo 大哥 CRCL给个方向 上次你说的90非常准 感谢

史上最全!8个免费视频下载工具,基本覆盖主流平台! 🔥 以后刷到好视频,直接保存再也不用愁了,无广告、不追踪、纯工具属性拉满: 1️⃣ 抖音/小红书视频图片:savetik.co 2️⃣ 推特视频:x2twitter.com/zh-cn 3️⃣ YouTube 下载:v6.www-y2mate.com 4️⃣ YouTube 字幕提取:downsub.com 5️⃣ 多平台通用神器:cobalt.tools 6️⃣ 国内聚合下载狗:xiazaitool.com 7️⃣ 1000+站点支持:snapany.com(有Chrome插件,网页自动嗅探) 8️⃣ YouTube/Twitter/FB等:9xbuddy.com(粘贴链接即下,零门槛) 这些工具覆盖YouTube、Twitter、TikTok、Instagram、Reddit、SoundCloud等几十个平台,基本一网打尽。 快收藏!以后留素材、存视频、提取字幕都方便多了。

@AndyWin007 我晕,什么时候到期的期权啊?期权前几天不止盈吗。周线425之下都算反弹,但是日线今日向上突破,就进入多头。

@JKeynesAlpha @JoeyTphilly Yeah I know that’s why I’m worried how come the huge drop off of that great news

关注: 具有“AI数据飞轮效应”的公司。 之前总结的AI 数据飞轮效应的 5 大核心要素: 1.独特数据资产 不可替代、别人拿不到的数据。 2.客户高迁移成本 系统深度嵌入 / 长期合约 / 再集成成本高。 3.动态数据飞轮 数据能持续更新,并形成闭环:数据 → 模型 → 产品 → 新数据 → 更强模型。 4.合规与生态壁垒 在金融、医疗、保险等行业,合规本身就是护城河;生态网络效应能进一步强化。 5.可扩展的商业模式 SaaS / 平台订阅 / 交易抽佣,让数据和 AI 的价值可规模化变现。

憋了好久的一个吐槽: Google 的Gemini 3的幻觉,远大于ChatGPT 5.2和Claude Opus 4.6,根本没法用于投资分析。 幻觉大的表现,就是: 话说的很满、很自信、而且倾向于你的偏好。 很适合做资本市场的卖方,但是不适合买方。 用胡猛的话,就是“你这说的是融资和pitch的语言,不是投资的语言。”适合当KOL,不适合当投资人。 容易把投资人带到沟里。 当然,Gemini可以用来做简单问题的快速搜索,比如: 一个公司在1分钟前出了财报,这时候你问GPT财报最新数据,GPT会说“财报还没出,搜索不到”,但是Gemini 可以搜索得到最新的结果。

币圈牛市结束了 修正2022年6月以来一直看多的观点 调整到中性观点 不做空也不看多了

谷歌浏览器上的 Gemini 更新了,主要的更新内容有: - Gemini 打开方式变成了侧边栏 - 支持在后台运行,你看其他 Tab 他也会继续运行 - 支持使用 Nano Banana 编辑图像 - 自动浏览功能,支持多步骤任务 仅限美国,开启过程非常费劲,跟你网络账号、浏览器状态都有关系