Heath

47 posts

Heath

@HRinvests

Turned a server income into a 6-figure portfolio Sharing my investing journey publicly 📈 AMD | Growth stocks | Pilot ✈️

Katılım Eylül 2016

17 Takip Edilen23 Takipçiler

when somebody tries to hurt you but you’ve already been in $SoFi for 4 years

English

🚨Why $SOFI is a $30 stock RIGHT NOW 🚨

🟩2026 EPS guidance: $0.60

📈Growth: revenue and EPS >40% which is 5x(!!) the market, deserving of a MINIMUM 50FPE when the average stock has around a 21 FPE.

🟰Quick math: $0.6 x 50 = $30.

A double from here, TODAY. STEAL OF THE MOMENT.

English

@Cantal_Capital Hard not to be bullish on $SOFI long term. I’ve been adding too

English

$SOFI I’ve officially sold 20% of my dividend portfolio to buy SOFI. I’m confident this will pay off.

Like if you're with me

English

@FIREDUpWealth Mostly all deployed I have around 5% left picking up shifts left and right just to get my cash up

English

How much cash do you have in your portfolio right now?

English

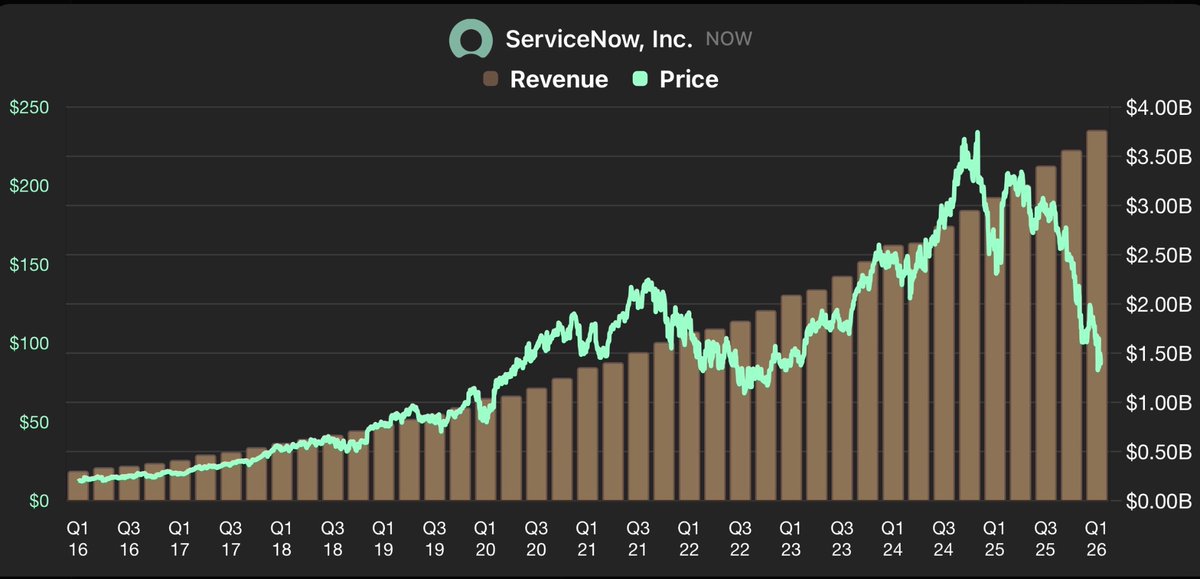

🚨 ServiceNow CEO Bill McDermott just dropped this on the AI hype:

“Most businesses don’t want to build workflow software for everything internally. They want one responsible AI Control Tower.”

ServiceNow is becoming the fabric connecting every hyperscaler, every LLM, systems of record and now full security (cybercrime = $1 Trillion/month problem).

True agentic enterprise is here: MoveWorks, VZA identity, Armis OT/security. Integrated major moves in just 20 days.

Jensen Huang ( $NVDA CEO) approves, they’re teaming up on the agentic future.

2030 Price Target: $1,200 – $2,000+ per share as they hit $30B+ revenue and own the enterprise AI operating system.

While others talk apocalypse, ServiceNow is building it.

$NOW to the moon.

Who’s loading up?

English

Holy sh*t

$SoFi can use the SEN network to do crypto lending

English

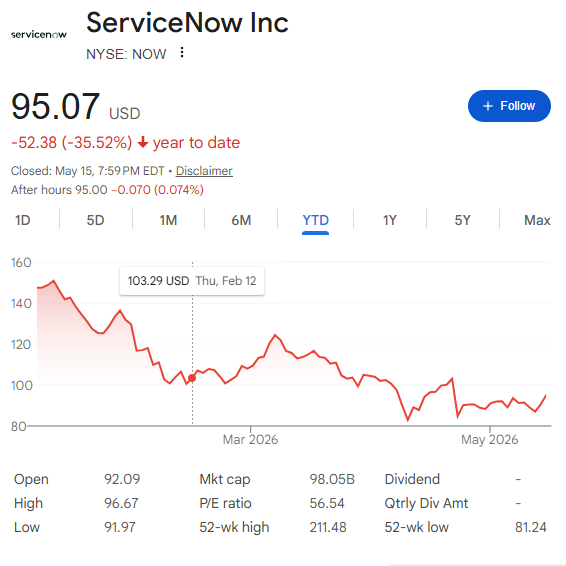

“ServiceNow $NOW is a dead company“

Meanwhile:

🟢 Revenue growing +29%

🟢 Margins Expanding

Who’s buying $NOW with me?

English

You in 2035 when you bought:

$META under $700

$NOW under $100

$SOFI under $20

$ZETA under $20

English

Building wealth starts with investing your first $100

Stop waiting — Start investing

English

@C_Reilly5 $SOFI . Feels like the better growth play from here, but I do like Nike’s dividends $NKE

English

Which beaten down stock would you rather dump $55k in (if you were forced to, bow and arrow aimed at your head)

Nike $NKE or SoFi $SOFI?

English

@JordInvests Probably $SOFI too honestly. Still feels like one of the better long term growth plays if they keep executing.

English

What is the one stock you’re looking to buy tomorrow when the market opens?

For me it’s $SOFI

Unfortunately I sold a load of this for $8 a year or two ago. Shame! Buying back in at $15 tomorrow.

English

@marketswithmay People still underestimate how valuable the ecosystem becomes if rates ease and mortgages ramp back up. The optionality with stablecoins + financial services all under one roof is what makes $SOFI interesting long term.

English

$sofi. Love this though for my opinion, 3 nuances.

1/ ya’ll know I don’t care on the tech platform, esp given all the massive current tech changes.

2/ I love the flywheel and add the nuance that if rates at all lower, mortgages will be huge. The size of mortgages is far larger. Hence you’ll see numbers look insane if it happens

3/ prob he’s focused on near term as I know he knows the stable coin story. I def -at this point- love the stablecoin optionality. Wanted to give it a shoutout.

Shay Boloor@StockSavvyShay

WHY $SOFI IS A TOP 3 POSITION FOR ME The market is overpricing the credit fear and underpricing the platform optionality when it comes to SoFi which is why I think it's one of the weirdest setups in the market right now. The business is still executing very well but the stock is stuck in one of the worst sentiment buckets since the market clearly doesn't want exposure to credit-sensitive stocks in a higher-for-longer rate environment and SoFi still gets treated like a bank-like lender even though the business is becoming much broader than that. The Loan Platform Business (LPB) is more important than people realize since SoFi originated $3B of personal loans on behalf of third parties through LPB in the quarter and added another $3.6B of capital commitments from three new partners. That matters because it gives SoFi flexibility so they can choose which loans to keep on the balance sheet and which loans to push through partners for fee revenue without taking the same balance sheet risk (very different model than being a traditional lender that is stuck holding everything). This is also why the private credit fear looked less scary if you listened to the actual earnings call. One of the biggest bear arguments was that funding partners would pull back if credit conditions weakened but Noto said they're not seeing issues in performance or partner demand and LPB demand was actually above what they chose to fulfill. The member flywheel is still the main reason this is a top 3 position for me because this is a real moat the market is overlooking. SoFi added over 1M members in the quarter, ~45% of new products came from existing members and 50% of SoFi Plus sign-ups took another product. The more members they add, the more products they cross-sell, the more deposits they gather, the more revenue they generate per member and the more efficient the platform becomes (how SoFi becomes more valuable over time). SoFi Plus becoming a paid subscription is also great to see because recurring fee revenue on top of a growing user base can improve unit economics over time. The biggest thing I want to see next is the Tech Platform turning around which is obviously the weakest link. Technology Platform revenue fell 27% YoY to $75M, contribution profit fell 61% and total accounts declined because of the large client that transitioned off the platform. Management is rebranding it as SoFi Tech Solutions and breaking it into processing, banking core ledgers, payment hub, and risk and fraud. If that platform starts growing again then great but I view this more as a free call option on owning SoFi. I truly believe SoFi is a good business trapped in a bad sentiment bucket. The market is focused on rates, credit risk and the weak Technology Platform while I'm focused on members, deposits, cross-buy, loan platform flexibility, operating leverage and the long-term path toward becoming a top financial institution. It can absolutely trade lower if the market sells off or if credit fears come back but I think the business is much stronger than the stock action suggests and I have no problem keeping this a top 3 position for me.

English

$SoFi is strong, books are still strong. Tech stack is stacking their chips, in time they will catch a bid, still growing like a weed. Love my $SoFi shares, not worried about it this year and I think next year they start ripping… a couple of rate cuts and a couple of “big boys” getting onboard with their enterprise banking, and the stock moons.

English