Abraham Ifkovics

867 posts

Abraham Ifkovics

@IfkovicsA

Interests: geopolitics, stock market, volatility

Budapest, Hungary Katılım Kasım 2018

1.1K Takip Edilen190 Takipçiler

@yaireinhorn @FT @TimOpler @SamFazeli8 @BiotechCH @BiopharmIQ @bioinvestor24 But sir, respectfully

$ 7bn for a $1 tn company is very low, we are just yet to see larger free cash flows.

What allows Lilly to be a monster is its huge market cap & expected free cash flow

Other BP keep waaaay more cash & liquid assets.

English

Another sign of $LLY unprecedented dominance in the BioTech and Pharma ecosystem - especially when compared to other Big Pharma companies - $PFE $JNJ $NVS $NVO $BMY $ABBV $MRK $SNY and others, can be seen in this excellent FT chart👇which shows the staggering dry powder that $LLY has accumulated due to the immense profitability of its weight-loss and diabetes drugs like Mounjaro & Zepbound. By the end of 2025 Eli Lilly had amassed cash and other highly liquid assets worth $7.3B - a 121% year-on-year rise, giving it the dry powder to invest heavily in diversifying its business before its blockbuster weight-loss drugs start to come off patent over the next decade.

Yair Einhorn@yaireinhorn

This interview of Jake Van Naarden $LLY head of corporate business development, by @angelicapeebles - CNBC’s excellent Pharma reporter, has demonstrated once again just how far-sighted Eli Lilly’s strategy really is and how it helps Eli Lilly to strengthen its dominance in the BioTech and Pharma ecosystem. I was especially interested to learn more about the rationale behind Eli Lilly’s staggering deal-making pace and that there is much more to come M&A-wise. Definitely worth your time! $XBI

English

Abraham Ifkovics retweetledi

$ABVX CEO Marc giggled after induction data

Now he’s laughing and smiling when asked about M&A

“Top 10 drug”

“Pharma needs revenue”

“Efficacy second to none”

DoctorDueDiligence@DueDoctor

I don’t know who needs to hear this but $ABVX has already showed their cards 1. ATM was oversubscribed, essentially a sweet heart deal 2. Closed in one day (not standard) 3. The MGMT basically said they want to sell if price is right 4. If/when Crohns hits it essentially becomes too big to buy for most companies I don’t see a way forward unless it is a quick sale Reuters reported before latest data follow up multiple buyers The one holdback is - what price? This holdback is solved by one fact and one fact only Multiple bidders = FOMO Biotechs don’t sell, they get bought If you have Crohns hit it is a $10BN revenue It’s basically pay less now vs pay more later if you expect it to hit I absolutely expect one or more pharmas to bid heavily and see Crohns as a call option So what will Abivax MGMT do? You absolutely sell if you can get $220 or more a share For the sweetheart ATM that’s a 76% increase in short time There’s just too much at stake and a MGMT that imo does NOT want to launch a drug

English

@IfkovicsA @Andre_AGTC Potential CD peak sales is $5B but at this point in time can only be a multiplier of 1. UC is most likely 5B X 3, so about a $20B current value. If major bidding, then MAYBE 22-23B.

English

$ABVX relevant

Here is the list of some BO and projected peak rev to BO price multiples

$CRNX 10B/4.2B ->2.4

$KRTX 14B/6B -> 2.3

$RXDX 11B/4.8B -> 2.3

$MRTX 5.8B/2.3B -> 2.5

$BPMC 9.5B/4B -> 2.4

$IMGN 10B/4.5B ->2.2

Andre-ACGT@Andre_AGTC

$ABVX Piper listed the following for the upgrade -recent gastroenterologist survey of KOL -malignancy concerns have been put to rest Of cource Piper is supposed to be bullish bc they were book running manager of the recent capital raise

English

@Andre_AGTC Or 2-3y before LoE. Anyway, thats not my main point. UC should be around $5 bn peak sales - bit less or more idk.

But you fully ignore the CD indication, thats the real issue.

English

@IfkovicsA Historically drugs peak 7-8 year post approval

And don't forget we will get generic competion in UC in mid 2030s

Not on Obe but on some other UC drugs. So 2039 EOL is irrelevant

English

@Andre_AGTC Dude Im on the buyside…

1) 2035 is not peak sales, not even for the UC. More like 2037-2038, based on the 2039 LoE.

2) peak sales est. does include the pipeline (CD), just as you include the projected sales of assets currently in P2 or P3.

Lazy sellside is non-answer…

$ABVX

English

@IfkovicsA Yes. Where you get this number?

The most bullish analyst, running recent capital raise, is saying 4.2B peak revenue based on KOL survey and you say - no no no I know more

Whit this attitude you will never make money in the stock market

English

@Andre_AGTC 1) in Phase3 vs post-P3

2) include (risk adjuated) Chrone if you want to go for estimated revenue…

English

$ABVX

Piper ups the 2035 UC revenue from 3.7 to 4.2B

$CRNX was just aquired for 10B with estimated peak rev 4.2B (4.5B $VRTX projection)

ABVX current MC is 12.2B

Either CRNX get aquired 20% below the fair price or ABVX is by 20% overpriced

quantumup@Quantumup1

Piper Sandler⬆️ $ABVX's PT to $175 from $165,⬆️U.S. 2035 UC revenue est to $4.2B, reiterated Overweight and said -- Updating Model, Raising UC Estimates; Continue to See Upside CRVS $SYRE PTGX - JNJ APGE - $ABBV PALI RHHBY MRK TEVA Piper Sandler added—We remain Overweight rated on ABVX shares, raising our UC obefazimod revenue estimates and price target following the Part 2 maintenance readout and recent equity financing. With malignancy concerns now definitively put to rest and obefazimod's best-indisease efficacy, and supported by our recent gastroenterologist survey work and KOL work, we are raising our UC revenue estimates and now model 2035E US UC revenue of $4.2B (vs. $3.7B prior), increasing our PT to $175/sh. Thus even with the recent stock move (+44% since Part 2 data) we believe there's significant upside that can make its way into the stock heading into upcoming events including presentation of full Part 1 UC maintenance data at UEGW in October, preclinical combo data ~early-2027, and Crohn's data mid-2027. Takeout is not contemplated in our thesis but remains a topic of ongoing investor discussion, which we address in more detail below. We remain buyers here.

English

This man must be stopped

Vlad Tenev@vladtenev

Only 62% of Americans have exposure to US stocks I’d like to get that to 100

English

@Mike10947310 What is this latest development around 200E?

If not corruption, idk…

English

If you’ve been following the $PESI situation, this is important reading. Especially regarding grouting 200E waste.

Basil Alsikafi@Balsikafi

tri-cityherald.com/news/local/han… Not THE news, but it's news. $PESI

English

@limpozzman @TOWiU2 @MarkWhittier1 @A_May_MD Quite fair, although our cult leaders hope for better term.

180/sh is approx 17bn, so thats like 3x multiple on a $ 5bn UC sales + cash on hand (+$ 1.5bn)

$ 40/sh for CD in CVR like $ 4bn.

Seems to be a bare minimum.. if auction is competitive then it should be higher

English

@TOWiU2 @MarkWhittier1 @A_May_MD I think based on Marc’s history of CVRs and the ambiguous value of Chron’s at this stage, it will most likely be a 180 cash + 40 CVR buyout, instead of an all cash deal.

English

American markets may have been closed Friday, but The Euronext was open, and $ABVX continued its run in Europe, closing at the US equivalent of ~$154.50.

That'd be another 7% rally and an all time high for $ABVX tomorrow should the US markets reflect what Europe showed (on reasonable volume, for the Euronext) on Friday.

I still feel that this $ABVX rally should continue, and I strongly believe that people have made the mistake to anchoring to the prices we saw on this recent dip.

The reason for the dip has now been entirely debunked. Not only were the cancer cases well within background rates, but several of them other occurred so early or had such strong evidence suggesting that they were pre-existing that the FDA isn't even going to look at them twice. The cancer BS is over, end of story.

Meanwhile, nobody debated that the efficacy data that $ABVX showed, both in part 1 and part 2, blew away every single expectation anyone had going in - even the very most bullish.

So what we have now is $ABVX significantly underperforming the $XBI over the last month despite releasing what is arguably the greatest IBD readout of all time.

Since the $ABVX data release:

↪️$ABVX +9%

↪️$XBI +20%

🙄Oh, and don't even get me started on the YTD performance...$XBI +32% vs $ABVX +8%!

$ABVX is underperforming the index by ~11% during the period where it released 2 absolutely blue sky scenario readouts.

Sure, $ABVX looks like it is up a lot over the last couple weeks if you want to start your analysis at the nadir of a stock crash that was driven by some mass delusion about cancer rates. But we can rather objectively see now...that entire escapade was just absolute bullshit 🤷♂️

There never was any legitimate cancer signal, and the prices at which the stock traded during that period of insanity are equally as illegitimate. I think it's quite easy to argue that these numbers can be entirely ignored.

In that case, shouldn't $ABVX be outperforming the index since its data were released? It certainly stands to reason.

It's hard to stress how far beyond the bullish expectations the efficacy data resulted, and there wasn't a SINGLE safety issue to discuss AT ALL once we were able to talk sense into people about the cancer nonsense.

The clinical remission rates were at the absolute top end of the bullish range for BOTH dose levels, and the endoscopic remission rates (often GI docs' preferred endpoint) were well above what most people even thought POSSIBLE to achieve with a monotherapy...DOUBLING the delta of the next highest ER rate from the 2nd best drug...completely unprecedented efficacy.

It does not seem controversial to me to think that these incredible beats on expectations should lead to market outperformance. I've never seen an I&I readout come so far above consensus results, ever.

How far should the rally go? IDK. I don't really "do" price targets, but:

↪️Just "market perform" (+20%) since the data brings $ABVX to $159

↪️Just outperforming the market by 10% (+30%) brings $ABVX to $174

I personally don't see $170s as unreasonable at all. In fact, I thought the $170s range was where the stock was headed on the original part 1 dataset, but part 2 seems to have upped the ante again by showing incredibly high rates of maintenance responses achieved in induction non-responders (a very big deal for time on therapy and market uptake, and thus for the revenue bottom line).

Maybe the stock goes there soon, maybe it doesn't, but it certainly wouldn't be unreasonable from my perspective. I now believe we are looking at a high probability of nearer term M&A that should land somewhere in the $200s. Would the M&A premium on $170 be 100%? Of course not. But the relatively high probability of near term M&A should be reflected in the open market price here, because there is already no secret that talks are ongoing.

IMO the stock should be pricing in:

1⃣Absolutely unprecedented maintenance data

2⃣Newfound M&A speculation (due to the Reuters article and the greenshoe breadcrumb that all but confirm talks have heated up)

3⃣A massive 20% rally in the $XBI

Even at the $154 level that the stock hit on the Euronext Friday...$ABVX still isn't fully pricing in any of those factors from my (BIASED) perspective.

Let's see where it goes! Speaking for myself, I'll be disappointed if it doesn't at least see the $160s this week. There has just been too much exceptionally positive news for this stock to underperform the $XBI like this, and I simply do not buy the idea that anyone should anchor themselves to prices that resulted from a "cancer scare" delusion that has been completely debunked. The "cancer signal" wasn't real, and neither were the temporary stock prices it generated.

Here's to hoping we finally see some OUTPERFORMANCE with $ABVX from here on out!

English

Abraham Ifkovics retweetledi

@Agent0088156721 @WallStSai @bioinvestor24 @HansGnt05391203 They have one of the largest leverage, but if they really want it, they can pay with shares.

Bigger fishes should circle around. If Lilly wants it, noone can outbid them.

Also: BP with large existing I&I assets should makes sure that $ABVX won’t be sold cheap!

@A_May_MD

$ABVX

English

@WallStSai @bioinvestor24 @IfkovicsA @HansGnt05391203 ROI and accretion drives these decisions. If PFE is constrained by price, they’ve got bigger issues

English

@IfkovicsA @HansGnt05391203 If $PFE Bourla was so stingy with massive obesity market to pay Metsera initially $4-5 B and then ends up paying $20 B for single drug from $ABVX in a smaller and more crowded market. Then he deserves all the blame that people cast on him.

English

@bioinvestor24 @WallStSai @HansGnt05391203 After this P3 part 2 data and price action and this huge raise…

I dont know what they think cheap os😂😂

My simple opinion: under $200/sh they wont even pick up the phone.

*Im biased and very long

**also I just can’t imagine why it won’t be competitive.

English

Bourla could be trying to get $ABVX cheap. He tried that with $VKTX in Feb 2025 and CEO told him F off. Then tried cheap with Metsera that cuved in ( management knew they were hyping assets and wanted to see ). So either ABVX getting competitive offers .. and then Pfizer efforts are waste. Or it is all hype on X.

English

@WallStSai @bioinvestor24 @HansGnt05391203 Legit. But what the f are they doing in Paris then.. very strange and noticable plane clustering.

English

@bioinvestor24 @IfkovicsA @HansGnt05391203 $PFE already overpaid for $MTSR Metsera deal by $3B due to bidding. I don’t think they are in a position to spend $20B on $ABVX and make another big blunder. Rather they would lean towards $MDGL which has built its pipeline by 10+ programs focused on MASH.

English

🚨 | 𝗕𝗥𝗘𝗔𝗞𝗜𝗡𝗚: Reports are circulating that Cristiano Ronaldo’s PR team has been privately messaging major sports media pages, offering paid promotions to push negative narratives against Argentina and Lionel Messi.

English

@bioinvestor24 @HansGnt05391203 Its already at $14-15 bn fully diluted mcap soo.. they either pay $ 20bn in EV or wont buy it.

But the clustering of their flights to Paris is.. just really suspicious

$ABVX

English

@HansGnt05391203 I thought so. But $PFE is not going to spend > $10 B on $ABVX at least from what Bourla stated at GS. Although he changes his mind.

English

$PFE is getting ridiculously cheap vs peers. I am talking in comparison to $MRK $GILD or even $JNJ ….

Pfizer still has good assets and descent pipeline ( CDK4 inh , immunology , ADC). The deal with Innovent was very good and brings several ADC opportunities …

Market is unhappy with its BD and how much it spent. Metsera was really bad not that it will not sell the drug($) and get some ROI, but due to lost bigger opportunity as Pfizer been shouting about obesity for years.

Chatter about PFE interest in $ABVX probably real but how much Pfizer willing to pay for something with still some questions on safety ?

Watch also $SYRE or $IMVT .. but these not selling cheap either.

I honestly don’t see how MRK has better future vs Pfizer and how it deserves more than double valuation ?

Bioinvestor24@bioinvestor24

My gut feeling we arrived to critical stage in $PFE story and will see either a shake up in management or unusual size deal to rebalance the MC stark inequity with peers ? Even $AMGN and $GILD are much larger than Pfizer now ? Probably the time to consider a long term position.

English

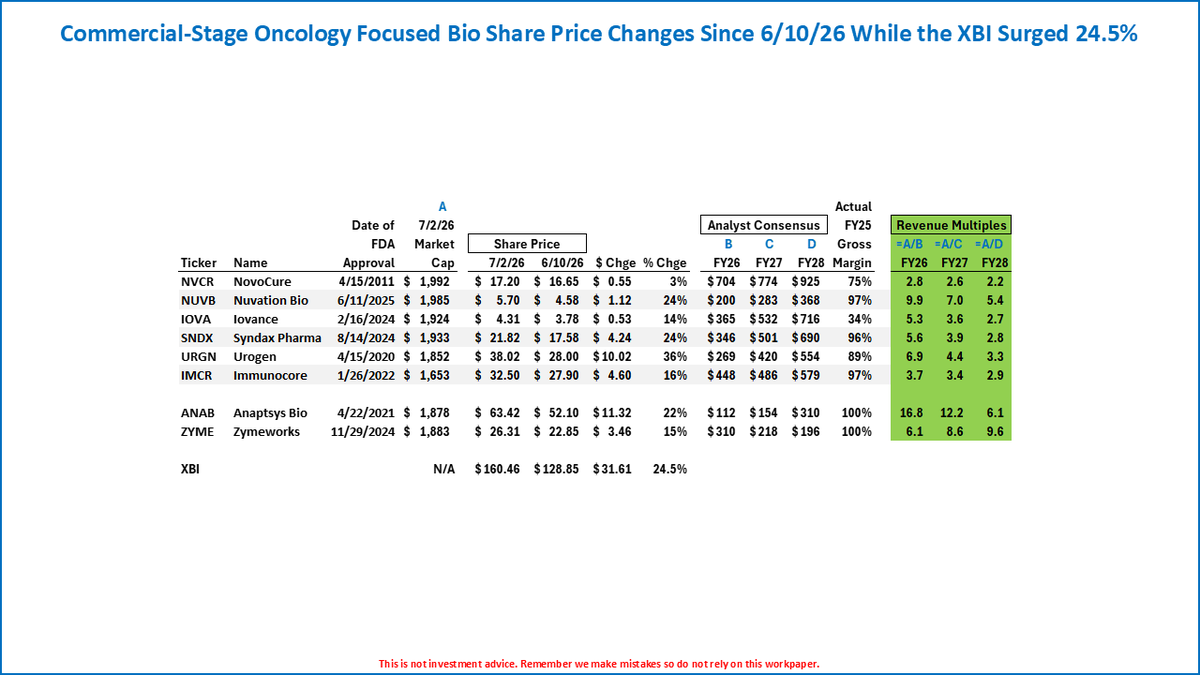

The now 8 commercial-stage oncology focused bios change in share price the last 15 trading sessions while the $XBI has surged 25%

We suspect a $URGN M&A exit may be imminent (but we've been very wrong before)

$IOVA $NVCR $NUVB $SNDX $IMCR $ZYME $ANAB

$IBB $LABU $NBI

English

@meremrtl @Cattletech @HansGnt05391203 @Duke0035 @SeekingAlpha See no fundamental idiosyncratic risk at least until the P2b CD readout

Worst thing that can happen is the fade in M&A pricing (just started imao). Then we fall back maybe around $ 120. Imao market should be patient at least until the end of summer

Then only top-down risk remains

English

$ABVX

Do we have an award for the worst-aging biotech post?

“Already recovered from the cancer scare” (this was in the $90’s)

Top-tier analysis over at @SeekingAlpha.

English