Bhavish Aggarwal@bhash

Released our Q4 FY26 Shareholders’ Letter here: bit.ly/3RxJRoU

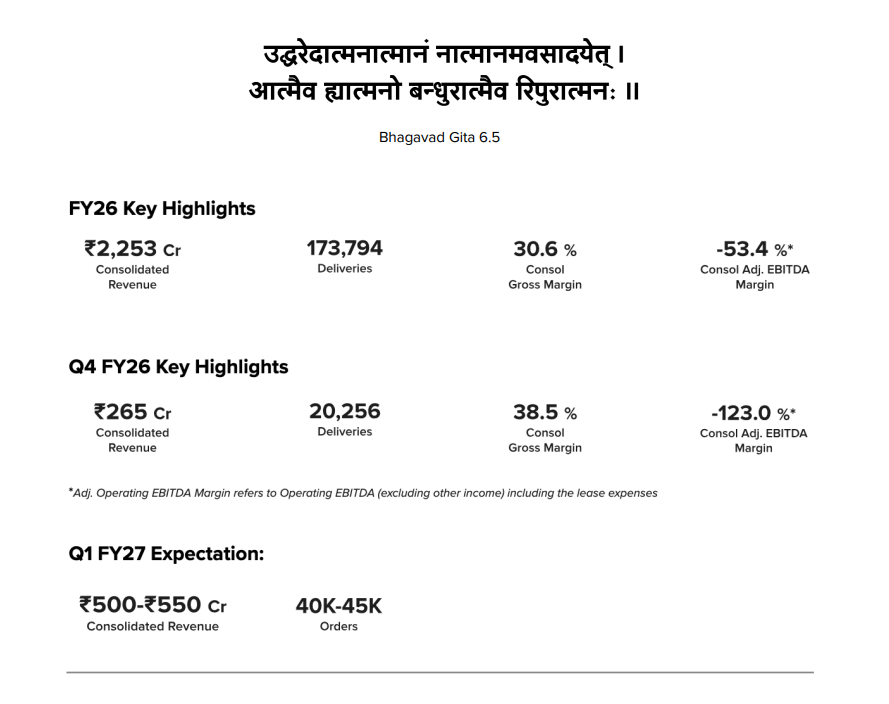

FY26 volumes were lower than where we want them to be, but FY26 was also the year in which the fundamentals of the company became much stronger.

We exited the year with industry-leading gross margins, a much lower cost base, sharply better service metrics, improving product quality, our first operating cash-flow positive quarter, and a Gigafactory now entering scale-up.

This comes at a time when India’s energy-security moment is here.

The next few years will be defined by two shifts happening together: mobility moving from ICE to EV, and energy moving from imported fuels to locally made batteries. Ola is building across both — electric mobility, cell manufacturing and energy storage — on one integrated platform.

In Q4, consolidated gross margin reached 38.5%, up from 34.3% in Q3 and 13.7% last year. This is now an industry-leading margin profile, ahead of most 2W OEMs including ICE incumbents. It reflects our structural advantages: vertical integration, Gen 3 maturity, pricing architecture and downstream control.

Q4 was also our first operating cash-flow positive quarter. Consolidated CFO was ₹91 crore. Auto delivered ₹213 crore CFO and ₹173 crore FCF. Ola is now moving from heavy build-out to disciplined scale-up.

We have reset the cost base. Consolidated opex reduced from ₹844 crore in Q4 FY25 to ₹428 crore in Q4 FY26, with a path towards ₹350 crore per quarter over the next couple of quarters.

Execution has improved meaningfully. Service TAT is down 88%, same-day closures are at ~87%, parts pendency is down 69%, and Gen 3 warranty cost is 70% lower than Gen 2.

As execution improved, sales have started responding. April registrations were up 20% MoM while the broader E2W industry declined more than 22%. We are working towards rebuilding national market share to 15–20% over the next six months.

For Q1 FY27, we expect 40,000–45,000 orders and consolidated revenue of ₹500–550 crore, nearly double Q4 levels. As volumes recover, we expect the auto business to move towards Adjusted Operating EBITDA and free cash flow positivity through FY27.

Roadster is becoming our second growth engine. Motorcycles are India’s largest 2W category and EV penetration remains very low. Ola now has 50% market share in electric motorcycles, and bikes contributed 15% of April gross orders. With up to 9.1 kWh battery and 500+ km certified range, Roadster is built for range, performance and reliability.

The Gigafactory is entering the scale phase. We have 2.5 GWh operational capacity. Installation to 6 GWh is largely complete, with commercialisation to be completed by the end of this quarter. Our 4680 Bharat Cell is already commercialised and deployed in vehicles. Around 15% of orders are already from products using our own cells, and we plan to transition the full vehicle portfolio to own cells by September 2026.

The same battery platform opens the next large opportunity: energy storage. Shakti is entering the market with 50k+ customer leads and strong B2B interest across telecom, petrol pumps, retail, dark stores and commercial backup. Mahashakti is being developed for C&I and utility-scale storage.

Ola is positioned across the two most important pillars of India’s energy future: electric mobility and batteries.

Vehicles create captive demand for the Gigafactory. Cells improve our vehicles through range, cost and supply-chain control. The same platform opens energy storage through Shakti and Mahashakti.

The heavy build phase is behind us. The next phase is disciplined scale.

FY27 is about recovering volumes, sustaining service consistency, holding margin leadership, reducing opex, ramping the Gigafactory, and scaling Shakti and Mahashakti.