Waldo

126 posts

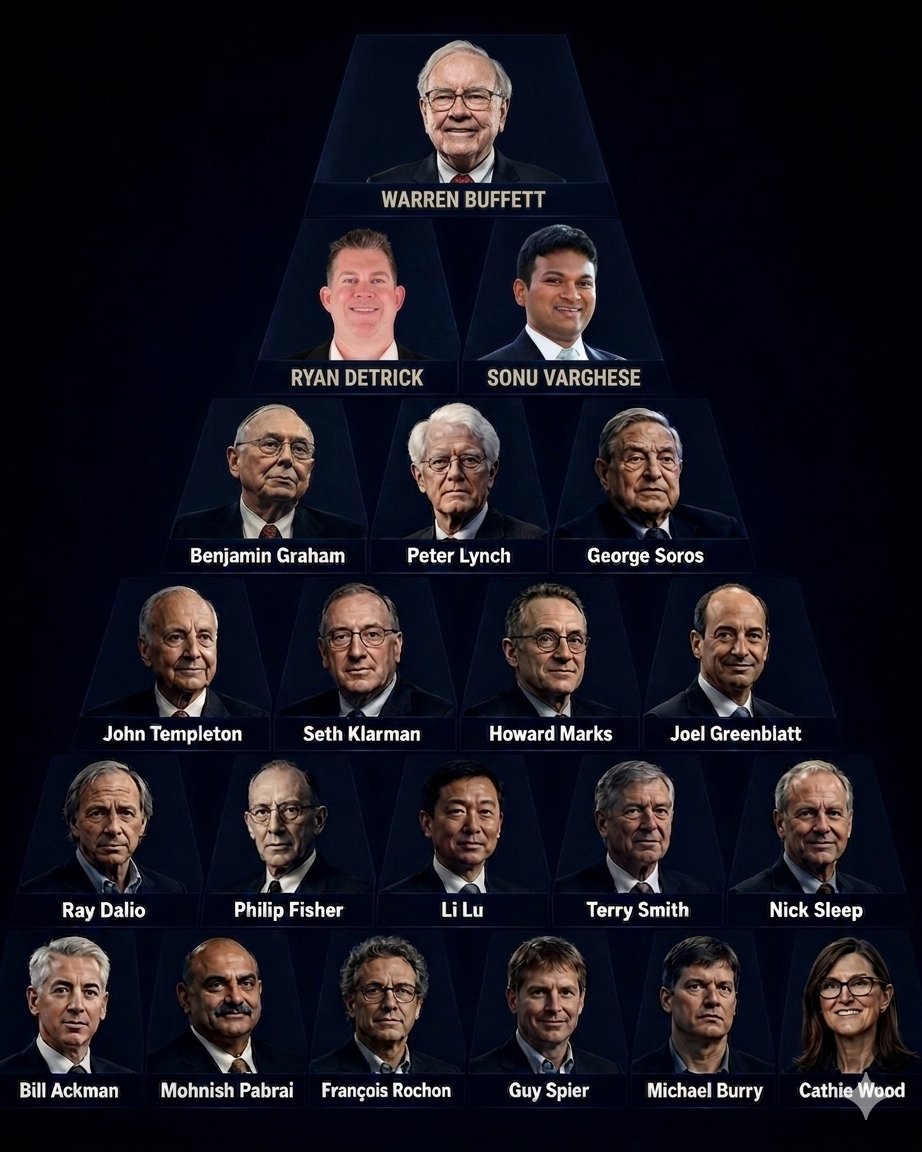

Pyramid of the best investors ever.

Who is missing?

English

@its_The_Dr Absolutely a dream team for Republicans. If any Republican couldn’t beat this ticket, they don’t deserve to be president.

English

The left call this the Dream Team, what do you call this?

English

@Ghade @Gosleepriya I think that’s the answer. I don’t know why there aren’t more people with that same answer kind of obvious so many of the other ones actually break the rules.

English

@porterstansb Always interesting to watch what Porter is up to. He doesn’t mention the size of his enterprises that are outside the MKTW umbrella.

English

Why I’m Buying MarketWise

Important Disclosures: I am the founder and the largest individual shareholder of MarketWise, Inc. (NASDAQ: MKTW). I am a current member of its Board of Directors. However, the views expressed below are my personal opinions. They have not been reviewed by the company. The factual statements are drawn from MarketWise’s public filings with the U.S. Securities and Exchange Commission and from materials the company has published, all of which are cited.

I am not soliciting any transaction in the company’s securities, and nothing here should be taken as investment advice. This statement contains forward-looking opinions about future business performance. Actual results will differ. The risk factors described in MarketWise’s most recent Form 10-K and Form 10-Q apply.

What I’ve Spent Thirty Years Doing

For thirty years I have worked to give individual investors a level playing field with Wall Street’s best firms. I’ve hired world-class experts — David Lashmet, Erez Kalir, Jeff Brown, Marty Fridson, David Eifrig, Stephen Sjuggerud, and many others — to share their expertise with self-directed investors. I’ve built whole-industry analytical frameworks (notably in property and casualty insurance). I’ve designed diversified portfolio strategies of my own, including my Permanent Portfolio and the Better Than Berkshire Index. I’ve written books — 2029: The End of America and Warren’s Mistakes — that lay out, in detail, how investors can succeed. I’ve also sponsored millions worth of database construction to build out analytical systems, like TradeStops, designed to provide individual investors with powerful and effective software tools.

Most of that work is still owned and published by a public company: MarketWise, Inc. (NASDAQ: MKTW). I founded it. I remain its largest individual shareholder. I retired from the operating business in 2020, after 20 years as the company’s Chairman and CEO.

I returned briefly as Chairman and CEO in August of 2023 when the company’s largest shareholders asked me to return. The company came off the rails during the COVID period. The problems were serious, and they included fraud at one of our subsidiaries. I cleaned house. I dismissed the people I knew were responsible and the people I believed should have done more to prevent what happened. The cleanup came at a real cost to revenues and margins in the short term, but it was necessary.

I also took steps designed to put the company back on the path to prosperity in 2024. I recruited Jeff Brown, who had been one of our most successful editors, to come back to the business. I restructured compensation so that every employee — not just senior executives — had an equity stake. I wanted everyone in the building to be an owner.

In August 2024 I resigned as Chairman and CEO following a strategic disagreement with the Board.

My chosen successor, David Eifrig — one of the company’s founding partners — has continued and significantly expanded the restructuring I began.

The results of that work are now showing up in the company’s reported numbers.

The Numbers Today

Sources: Form 10-K (filed March 2026); Investor Presentation (March 2026).

FY 2025:

• Billings (cash received from customers): $271.2 million, up 13% year-over-year — the strongest annual growth since the company became public in 2021.

• Q4 2025 Billings: $78.9 million, up 42% year-over-year — the strongest quarter on record since the post-COVID adjustment.

• Cash from Operations in 2025: $46.0 million, a $68.1 million improvement over the prior year, when CFFO was negative $22.2 million.

• Cash flow margin (CFFO / Billings): roughly 17%.

• Net Revenue Retention: 91%, a return to pre-pandemic levels (96% in 2017).

• ARPU: $670, up 70% year-over-year, reflecting a deliberate shift toward higher-value subscribers.

• Dividends paid: $1.90 per Class A share, representing a cash yield of approximately 13% to Class A shareholders at the year-end share price.

Q1 2026 actual results:

• Billings: $81.4 million, up 15% year-over-year — the strongest quarterly Billings growth since 2023.

• Paid Subscribers returned to growth in Q1 2026, after a multi-year period of decline tied to the shut-down of the Legacy Research subsidiary in 2024.

• ARPU: $738, up 76% year-over-year.

• Recurring quarterly dividend was raised 25%, from $0.20 to $0.25 per Class A share.

FY2026 outlook:

(reaffirmed by management on April 17, 2026):

• Billings of approximately $300 million (+11% year-over-year).

• Cash from Operations of approximately $50 million (~16% margin on Billings).

• Total dividend target of $1.80 per Class A share (regular plus special distributions).

*******

What follows is my opinion, based on what I see in MarketWise’s filings and on the economics that I observe in my own private firm, Porter & Company, LLC, which likewise serves investors with proprietary investment research, analytics, and conferences.

I believe MarketWise’s published guidance is conservative. I believe that as investors seek out serious research on the artificial intelligence and robotics boom, demand for MarketWise’s products will exceed the company’s own internal forecasts.

Specifically, I believe the company will produce more than $50 million in cash from operations in FY2026.

I know from past experience (running MarketWise) and from my current results at Porter & Co., that a financial-research subscription business of this kind, when run efficiently, can produce 25–30% cash margins at maturity.

The company’s fixed cost base — corporate G&A, technology, public-company costs — has a much bigger impact on results when revenues are below $300 million. But as MarketWise returns to substantial growth and regains its former scale, I expect its margins to improve.

My base-case view for MarketWise is:

• FY2026 Billings: at or above $300 million (the company’s guidance).

• FY2026 CFFO: in excess of $50 million (above the company’s $50 million guidance), with CFFO margin of roughly 20% on Billings in 2026, scaling toward 25%+ over the next five years as operating leverage takes hold.

What That Means for the Stock

At a recent price of approximately $20 per Class A share:

• Total shares outstanding (Class A plus Class B, as of May 5, 2026): 15,625,554.

• Implied market capitalization: approximately $313 million.

• Cash and equivalents (March 31, 2026): $52.7 million; total debt: zero.

• Implied enterprise value: approximately $260 million.

• Against the company’s own FY2026 CFFO guidance of $50 million, the stock trades at roughly 5x current-year cash from operations.

• Against my own base-case view of FY2026 CFFO at or above $54 million, the multiple is closer to 4.8x.

• The forward dividend of $1.80 per Class A share represents a cash yield of approximately 9% at $20 per share.

On the Capital Structure and Liquidity

When MarketWise went public in July 2021, only a small portion of the company’s stock was sold to the public. Today, Class A common stock (publicly traded) represents about 17% of total shares; Class B common stock (held by founding members and not publicly traded) represents the rest (10-Q for Q1 2026).

Earlier this year, the company repurchased shares from a former executive who led the business during the COVID-era problems; that transaction reduced the total share count by roughly 4%.

The two-class structure and limited public float cause some investors discomfort. In my opinion, it should be a source of confidence. The founders of the business, who built it and who ran it through difficult periods, still own substantially all of their original stakes. They have a much larger interest in the company’s success than they have in the short-term movement of the share price.

I would also note: in late 2025, a founding investor group submitted a non-binding proposal to take the company private at what I believed was a low valuation. That proposal was withdrawn in February 2026 (10-K, FY2025). The independent directors did their job by rejecting this proposal. The rejection of that proposal sets the stage for the company to remain public and for outside shareholders to participate in the company’s recovery.

Why I’m Buying

For 20 years, while I led this business, it grew sales and earnings at roughly 30% per year and required almost no capital to fund that growth. I started the business with a borrowed laptop and a $36,000 marketing budget provided by Bill Bonner. No additional capital ever went into the business. Since inception, the company has paid out more than $500 million in dividends.

When run correctly, this is a great business. It can provide outstanding value for its customers and earn large returns on its capital base. I believe — based on the company’s reported results, the economics of my own private firm, and what I see in the market — that MarketWise is back on the right track.

For these reasons, I have been a meaningful buyer of the stock during 2026 and I plan to continue acquiring shares. I hope, at some point soon, that all of my work in financial publishing will be reunited on a single balance sheet at MarketWise. That’s not a commitment, and it’s not a forecast. It is simply what I would prefer, as the value of my ownership stake at MarketWise represents most of my net worth. It would be better for me (and I believe for MarketWise’s shareholders too). But whether that happens or not, the stock is, in my opinion, deeply undervalued today. That’s why I’m buying.

A reasonable person would ask: why tell anyone how cheap the stock is today? My purchases have been (and will continue to be) filed publicly with the SEC. There’s no hiding the fact that I believe the stock is very attractive. And I believe this kind of transparency would be great in the market. I wish every time an insider is making large purchases in stocks they would share their reasoning. It would greatly increase the public’s understanding of public markets.

MarketWise Five-Year

Operating Model

FY26

Billings: 301M (+11%)

Direct exp: 151M

Contribution: 151M

Op overhead: 100M

Op income: 51M

CFFO: 55M (18.1% margin)

After-tax cash: 30M

Div/share: $1.92

Yield@$20: 9.6%

FY27

Billings: 343M (+14%)

Direct exp: 165M

Contribution: 179M

Op overhead: 104M

Op income: 75M

CFFO: 79M (22.9% margin)

After-tax cash: 43M

Div/share: $2.76

Yield@$20: 13.8%

FY28

Billings: 388M (+13%)

Direct exp: 178M

Contribution: 209M

Op overhead: 108M

Op income: 101M

CFFO: 106M (27.4% margin)

After-tax cash: 59M

Div/share: $3.75

Yield@$20: 18.7%

FY29

Billings: 434M (+12%)

Direct exp: 191M

Contribution: 243M

Op overhead: 112M

Op income: 131M

CFFO: 137M (31.6% margin)

After-tax cash: 76M

Div/share: 4.83

Yield@$20: 24.2%

FY30

Billings: 478M (+10%)

YoY: 10%

Direct exp: 201M

Contribution: 277M

Op overhead: 116M

Op income: 161M

CFFO: 168M (35.2% margin)

After-tax cash: 93M

Div/share: $5.92

Yield@$20: 29.6%

Notes on the model:

• "Billings" is cash received from customers in the period — the leading indicator for a subscription business. GAAP Net Revenue lags Billings by 12 to 24 months and is therefore not the most useful current-period measure.

• Direct expenses include affiliate marketing commissions, salesperson commissions, fulfillment costs, royalties, and direct labor. The model assumes the direct-expense ratio declines from 51% of Billings in FY2025 to 42% by FY2030, reflecting operating leverage on a largely fixed editorial and content base.

• Operating overhead grows roughly with inflation; the company has already taken significant cost out of the business as part of the post-COVID restructuring. • Working capital adjustments reflect the net positive cash inflow from deferred subscription revenue.

• A note on the tax line: MarketWise has an unusual capital structure that produces a high effective cash tax rate. MarketWise, Inc. is a holding company that owns roughly 16% of MarketWise, LLC; the remaining 84% is owned by founding members through Class B units. Under the LLC operating agreement, MarketWise, LLC is required to make tax distributions to all of its members — including the C-corporation parent — at the highest combined federal, state, and local individual tax rate. For 2025, that rate was 49.75%. Because MarketWise, Inc.'s actual corporate tax liability is materially lower than its proportional share of these LLC tax distributions, the excess cash is paid to Class A shareholders as special dividends. In aggregate across all owners, the company's effective combined tax rate on Cash from Operations runs at roughly 45%. In FY2025, MarketWise, LLC paid out $49.8 million in tax distributions and $12.2 million in regular distributions to noncontrolling interests, plus $4.8 million in dividends to Class A shareholders. "After-tax cash to all owners" represents the cash available for distribution after the LLC has satisfied its tax distribution obligations. In practice, this cash is split between regular dividends to Class A shareholders, special dividends to Class A shareholders (funded by the excess of MarketWise, Inc.'s tax distribution receipts over its actual corporate tax liability), and regular profit distributions to LLC unitholders. The "Dividend per share equivalent" line shows what the per-share number would look like if 100% of after-tax cash were distributed to all owners on a per-share basis — which approximates MarketWise's actual practice. The FY2026 model figure of $1.92 is closely consistent with the company's stated FY2026 dividend target of $1.80 per Class A share.

• Share count is held flat at 15,625,554 (Class A plus Class B, as of May 5, 2026). Buybacks under the company's authorized $50 million repurchase program could reduce this materially.

This model expresses my opinion. Actual results will differ.

Forward-looking statements are subject to the risks described in MarketWise's most recent Form 10-K and Form 10-Q.

Sources:

MarketWise, Inc. — Form 10-K for fiscal year ended December 31, 2025 (filed March 2026)

MarketWise, Inc. — Form 10-Q for the quarter ended March 31, 2026 (filed May 2026)

MarketWise, Inc. — Definitive Proxy Statement (Schedule 14A, filed April 17, 2026)

MarketWise Investor Presentation — March 2026

MarketWise news release archive

This statement reflects my personal opinions and the financial information available to me as of May 2026. I do not undertake to update it. The forward-looking statements expressed here are subject to risks and uncertainties, including those described in MarketWise’s most recent annual report on Form 10-K and quarterly report on Form 10-Q. Actual results may differ materially.

English

Brook Farm stands as one of history's most perfect controlled experiments in voluntary socialism; and its spectacular failure proves every principle of free market economics.

Picture this: 1841 Massachusetts. The brightest minds of the Transcendentalist movement, including Nathaniel Hawthorne as an investor, decide to escape "capitalist drudgery" by creating their perfect commune. These weren't your typical utopian cranks. They were educated elites who genuinely believed intellectual superiority could overcome economic reality.

The experiment started as a joint-stock egalitarian community where residents rotated between farm work and domestic duties. Manual labor for Harvard types. When that predictably struggled, they pivoted to French socialist Charles Fourier's "phalanx" model — shared labor, shared profits, shared everything. The intellectuals attracted other luminaries who bought into the romantic vision of escaping market-based work allocation.

Reality had other plans. Financial losses mounted as bookish idealists discovered that good intentions don't harvest crops efficiently. Internal squabbles erupted when people faced the eternal socialist problem: who decides who does what, and who gets what? The final blow came when their massive Phalanstery building burned down with zero insurance coverage. By 1847, they sold everything at auction.

Brook Farm collapsed despite every advantage socialism could ask for: voluntary participation, educated residents, shared ideology, and zero government coercion. Collectivist economics cannot work even when willing, intelligent people attempt it. The iron laws of human action and economic calculation operate in their purest form.

English

@royrubio123 @BoringBiz_ The same reason that they always have is that they need somebody to hold their hand during both good and bad times.

English

@BoringBiz_ I asked you in an earlier post. Do you think AI could kill the wealth management industry? Why will middle class families that have 100k to 2mil continue to lose a percentage for mutual funds and half decent advice?

English

Mom, how did we get so rich?

Your dad charged 2 and 20 to underperform the S&P 500

English

Can you guess what kind of car this is? 95 percent will not get it right!

English

@BillKristol Nice trolling Bill. Nobody can pronounce someone Christian or not.

Your TDS can be medicated.

English

This is one of the most shameless displays of financial gaslighting I've seen in 45 YEARS.

This week Blue Owl Capital disclosed that investors demanded 41% of their money back from one fund and 22% from another.

$5.4 BILLION in total redemption requests in a single quarter.

Blue Owl's response? They capped withdrawals at 5%.

Meaning if you had $1 million in Blue Owl's tech fund, you asked for $410,000 back, and they gave you $50,000.

Then they put out a LinkedIn post blaming "heightened negative sentiment" and insisting their fund performance is "robust."

That's like a restaurant blaming Yelp reviews while the kitchen is on fire.

Here's what they don't want you to focus on:

70% of Blue Owl's lending book is concentrated in software companies. They admitted this on their own earnings call.

These are the exact businesses most at risk of being disrupted or destroyed by AI.

And when the Wall Street Journal investigated further, they found Blue Owl's flagship fund reported 11.6% software exposure in public filings. The Journal's own analysis found it was actually closer to 21%.

That's not just a rounding error...

The timeline tells you everything:

In February, Blue Owl sold $1.4 billion in loans to meet redemptions. They claimed 99.7 cents on the dollar.

Sounds great right?

Except one of the buyers was Kuvare - an insurance company whose asset management arm Blue Owl ACQUIRED for $750 million in 2024. Blue Owl manages their money.

They sold assets to a company they control and called it an arm's length transaction.

Barclays downgraded the stock. Shareholders filed a lawsuit. Congress is now demanding disclosures on sales practices, leverage, and risk management.

The stock hit a record low of $7.95 - down over 60% from its 52 week high.

And through all of this, Blue Owl's CEO went on the earnings call and said: "We don't have red flags. We don't have yellow flags. We actually have largely green flags."

$5.4 billion in redemption requests. 60% stock decline. Gated exits. Congressional scrutiny.

All green flags, apparently.

I've been warning about private credit for months.

The sales pitch was always the same: equity-like returns with bond-like stability. No volatility. No correlation to public markets. Safe. Predictable.

Except when investors actually want their money, they discover the exits are bolted shut.

You can't eliminate volatility. You can only HIDE it.

And that's exactly what Blue Owl has been doing - hiding risk behind opaque valuations, related-party transactions, and withdrawal gates.

This isn't "negative sentiment."

This is what happens when the tide goes out.

Are you listening?

English

@BillAckman @X I completely agree and support you. I admire you in many ways that occasionally disagree with you. But you need to fight fight fight.

English

I am reaching out to the @X community for advice with the likely risk of sharing TMI. I have been sufficiently upset about the whole matter that I have lost sleep thinking about it and I am hoping that this post will enable me to get this matter off my chest.

By way of background, I started a family office called TABLE about 15 years ago and hired a friend who had previously managed a family office, and years earlier, had been my personal accountant. She is someone that I trusted implicitly and consider to be a good person.

The office started small, but over the last decade, the number of personnel and the cost of the office grew massively. The growth was entirely on the operational side as the investment team has remained tiny. While my investment portfolio grew substantially, the investments I had made were almost entirely passive and TABLE simply needed to account for them and meet capital calls as they came in. While TABLE purchased additional software and other systems that were supposed to improve productivity, the team kept increasing in size at a rapid rate, and the expenses continued to grow even faster.

While I would periodically question the growing expenses and high staff turnover, I stayed uninvolved with the office other than a once-a-year meeting when I briefly reviewed the operations and the financials and determined bonus compensation for the President and the CFO. I spent no time with any of the other employees or the operations. The whole idea behind TABLE was that it would handle everything other than my day job so that I would have more time for my job and my family.

Over the last six years, expenses ballooned even further, employee turnover accelerated, and I became concerned that all was not well at TABLE. It was time for me to take a look at what was going on.

Nearly four years ago, I recruited my nephew who had recently graduated from Harvard and put him to work at Bremont, a British watchmaker, one of my only active personal investments to figure out the issues at the company and ultimately assist in executing a turnaround. He did a superb job.

When he returned from the UK late last year after a few years at Bremont, I asked him to help me figure out what was going on with TABLE. When I explained to TABLE’s president what he would be doing, she became incredibly defensive, which naturally made me more concerned.

My nephew went to work by first meeting with each employee to understand their roles at the company and to learn from them what ideas they had on how things could be improved. He got an earful.

Our first step in helping to turn around TABLE was a reduction in force including the president and about a third of the team, retaining excellent talent that had been desperate for new leadership.

Now here is where I need your advice.

All but one of the employees who were terminated acted professionally and were gracious on the way out (excluding the president who had a notice period in her contract, is currently still being paid, and with whom I have not yet had a discussion).

The highest compensated terminated employee other than the president, an in-house lawyer (let’s call her Ronda), told us that three months of severance was not enough and demanded two years’ severance despite having worked at the company for only two and one half years.

When I learned of Ronda's request for severance, I offered to speak with her to understand what she was thinking, but she refused to do so. A few days ago, we received a threatening letter from a Silicon Valley law firm.

In the letter, Ronda’s counsel suggests that her termination is part of longstanding issues of ‘harassment and gender discrimination’ – an interesting claim in light of the fact that Ronda was in charge of workplace compliance – and that her termination was due to:

“unlawful, retaliatory, and harmful conduct directed towards her. Both [Ronda] and I [Ronda’s lawyer] have spoken with you about [Ronda’s] view of what a reasonable resolution would include given the circumstances. Thus far, TABLE has refused to provide any substantive response. This letter provides the last opportunity to reach a satisfactory agreement. If we cannot do so, [Ronda] will seek all appropriate relief in a court of competent jurisdiction.”

The letter goes on to explain the basis for the “unsafe work environment” claim at TABLE:

“In early 2026, Pershing Square’s founder Bill Ackman installed his nephew in an unidentified role at TABLE, Ackman’s family office. [His nephew]—whose only work experience had been for TABLE where he was seconded abroad for the last four years to a UK watch company held by Ackman—began appearing at TABLE’s offices and conducting interviews of employees without a clear explanation of his role or the purposes of these interviews. During this period, he made a series of inappropriate and genderbased [sic] comments to multiple employees that created an unsafe work environment. Among other things, [his nephew] made remarks about female employees’ ages (“Tell me you are nowhere near 40”), physical appearance (“Your body does not look like you have kids”), as well as intrusive questions about family planning and sexual orientation (“Who carried your son? Who will carry your next child?”). These incidents were reported to senior leadership at TABLE and Pershing Square. Rather than being addressed appropriately, the response from senior management reflected, at best, willful blindness to the inappropriateness of [his nephew]’s remarks and, at worst, tacit endorsement.”

The above allegations about my nephew had previously been brought to my attention by TABLE’s president when they occurred. When I learned of them, I told the president that I would speak to him directly and encouraged her to arrange for him to get workplace sensitivity training. The president assured me that she would do so.

When I spoke to my nephew, he explained what he actually had said and how his actual remarks had been received, not at all as alleged in the legal letter from Ronda’s counsel. I have also spoken to others at the lunch table who confirmed his description of the facts. In any case, he meant no harm, was simply trying to build rapport with other employees, and no one, as far as I understand, was offended.

Ironically, Ronda claims in her legal letter that TABLE didn’t take HR compliance seriously, yet Ronda was in charge of HR compliance at TABLE and the person who gave my nephew his workplace sensitivity training after the alleged incidents. In any case, Ronda, as head of compliance, should have kept a record or raised an alarm if indeed there was pervasive harassment or other such problems at the company, and there is no evidence whatsoever that this is true.

So why does Ronda believe she can get me to pay her nearly $2 million, i.e., two years of severance, nearly one year of severance for each of her years at the company? Well, here is where some more background would be helpful.

Over the last two months, I have been consumed with a major family medical issue – one of my older daughters had a massive brain hemorrhage on February 5th and has since been making progress on her recovery – and I am in the midst of a major transaction for my company which I am executing from a hospital room office next to her . While the latter business matter is publicly known, the details of my daughter’s situation are only known to Ronda because of her role at our family office.

Now, let’s get back to the subject at hand.

Unfortunately, while New York and many other states have employment-at-will, there has emerged an industry of lawyers who make a living from bringing fake gender, race, LGBTQ and other discrimination employment claims in order to extract larger severance payments for terminated employees, and it needs to stop.

The fake claim system succeeds because it costs little to have a lawyer send a threatening letter and nearly all of the lawyers in this field work on contingency so there is no or minimal cash cost to bring a claim. And inevitably, nearly 100% of these claims are settled because the public relations and legal costs of defending them exceed the dollar cost of the settlement. The claims are nearly always settled with a confidentiality agreement where the employee who asserts the fake claims remains anonymous and as a result, there is no reputational cost to bringing false claims.

The consequences of this sleazy system (let’s call it ‘the System’) are the increased costs of doing business which is a tax on the economy and society. There are other more serious problems due to the System. Unfortunately, the existence of an industry of plaintiff firms and terminated employees willing to make these claims makes it riskier for companies to hire employees from a protected class, i.e., LGBTQ, seniors, women, people of color etc. because it is that much more reputationally damaging and expensive to be accused of racism, sexism, and/or intolerance for sexual diversity than for firing a white male as juries generally have less sympathy for white males.

The System therefore increases the risk of discrimination rather than reducing it, and the people bringing these fake claims are thereby causing enormous harm to the other members of these protected classes.

So what happened here?

Ronda was vastly overpaid and overqualified for the job that she did at TABLE. She was paid $1.05 million plus benefits last year for her work which was largely comprised of filling out subscription agreements and overseeing an outside law firm on closing passive investments in funds and in private and venture stage companies, some compliance work, and managing the office move from one office to another. She had a very good gig as she was highly paid, only had to go into the office three days a week, and could work from anywhere during the summer.

Once my nephew showed up and started to investigate what was going on, she likely concluded that there was a reasonable possibility she would be terminated, as her job was in the too-easy-and-to-good-to-be-true category. The problem was that she was not in a protected class due to her race, age or sexual identity so she had to construct the basis for a claim. While she is female and could in theory bring a gender-based discrimination claim, she reported to the president who is female and to whom she is very close, which makes it difficult for her to bring a harassment claim against her former boss.

When my nephew complimented a TABLE employee at lunch about how young she looked – in response to saying she was going to her 40-year-old sister’s birthday party, he said ‘she must be your older sister’ – Ronda immediately reported it to our external HR lawyer. She thereby began building her case.

The other problem for Ronda bringing a claim is that she was terminated alongside 30% of other TABLE employees as part of a restructuring so it is very difficult for her to say that she was targeted in her termination or was retaliated against. TABLE is now hiring an external fractional general counsel as that is all the company needs to process the relatively limited amount of legal work we do internally. In short, Ronda was eminently qualified and capable and did her job. She was just too much horsepower for what is largely an administrative legal role so she had to come up with something else to bring a claim.

Now Ronda knew I was a good target and it was a good time to bring a claim against me. She also knew that I was under a lot of pressure because on March 4th when Ronda was terminated, my daughter had not yet emerged from consciousness, she was not yet breathing on her own, and my daughter and we were fighting for her life. I was and remain deeply engaged in her recovery while at the same time I was working on finishing the closing for the private placement round for my upcoming IPO.

Ronda also knew that publicity about supposed gender discrimination and a “hostile and unsafe work environment” are not things that a CEO of a company about to go public wants to have released into the media. And she may have thought that the nearly $2 million she was asking for would be considered small in the context of the reputational damage a lawsuit could cause, regardless of the fact that two years of severance was an absurd amount for an employee who had only worked at TABLE for 30 months.

She also likely considered that I wouldn’t want to embarrass my nephew by dragging him into the klieg lights when her claims emerged publicly.

So, in summary, game theory would say that I would certainly settle this case, for why would I risk negative publicity at a time when I was preparing our company to go public and also risk embarrassing my nephew.

Notably, she hired a Silicon Valley law firm, rather than a typical NY employment firm. This struck me as interesting as her husband works for one of the most prominent Silicon Valley venture firms whose CEO, I am sure, has no tolerance for these kinds of fake claims that sadly many venture-backed companies also have to deal with. I mention this as I suspect her husband likely has been working with her on the strategy for squeezing me as, in addition to being a computer scientist, he is a game theorist. My only advice for him is to understand more about your opponent before you launch your first move.

All of the above said, gender, race, LGBTQ and other such discrimination is a real thing. Many people have been harmed and deserve compensation for this discrimination, and these companies and individuals should be punished for engaging in such behavior.

Which brings me to the advice I am seeking from the X community.

I am not planning to follow the typical path and settle this ‘claim.’ Rather, I am going to fight this nonsense to the end of the earth in the hope that it inspires other CEOs to do the same so we shut down this despicable behavior that is a large tax on society, employment, and the economy and contributes to workplace discrimination rather than reducing it.

Do you agree or disagree that this is the right approach?

English

@petersavodnik Conflating anti-Israel as being anti-Semitic is fueling real antisemitism. Israel is a country. Zionism is a political ideology. These things are not religion or race exclusive.

English

Democrats are piling on AIPAC with the hope that the Jew hate will stop with AIPAC, that they can excise this one organization from the body politic and appease the antisemites and move on. They are wrong. This is the beginning, not the end.

Tom Steyer@TomSteyer

AIPAC is a dark money organization that should have no place in our politics.

English

@Nas_tech_AI I have been watching this development for a few years now and don’t see them growing in market share so maybe it’s not as perfect as it appears

English

A Spanish architect has developed a revolutionary interlocking brick system that fits together just like puzzle pieces. By eliminating the need for mortar, these structures remain flexible and remarkably strong even during earthquakes. It’s a brilliant blend of ancient logic and modern engineering.

English

@compliantvc Did you acquire consent from those persons to publish their photos on the internet in accordance with EU privacy regulations?

English

Europe doesn't need Iranian oil

This brand new windmill in a scenic park in Cologne, Germany marks the beginning of the European energy independence movement

We just need to install 11 million more of these over the next 3 months to achieve full energy autonomy

So far, we have 7 new ones permitted and another 2 under construction

We are right on track to bring down energy costs for all Europeans!

English

@MatthewWielicki Who knows more about risk than reinsurance companies. They have been the best barometer of the climate change issues.

Kind of like Polymarket for grown-ups

English

This chart demolishes one of the central claims of the climate cult.

It comes from Munich Re, one of the world’s largest reinsurance companies. Their entire business depends on accurately pricing risk.

What does it show?

Weather disaster losses as a percentage of global GDP from 1990–2025.

Not raw dollars.

Not media headlines.

Losses normalized to the size of the global economy.

And the trend?

Flat… if anything slightly declining.

If climate change were causing an explosion in extreme weather damages, losses should be rising faster than global wealth.

They aren’t.

What we see instead are occasional spikes (1993, 2005, 2017) surrounded by long periods of normal variability. Weather fluctuates. The long-term trend does not show escalating catastrophe.

So why does the public constantly hear about “record climate disasters”?

Because the climate industrial complex almost always cites raw dollar losses. As the global economy grows and more infrastructure exists, of course the total cost of disasters rises.

That’s not climate.

That’s propaganda.

Normalize the data properly, and the panic narrative falls apart.

The truth is simple: despite rising CO₂ and endless climate alarmism, weather disasters are not consuming a larger share of global wealth.

The climate cult needs people to believe the world is spiraling into chaos.

The data keep saying otherwise.

English

@RockChartrand It is terrible and left unchecked will lead to ruin. Nobody will buy anything if all assets and consumables are deflating at the same time.

Own assets that appreciate and sell all others.

English

Can someone explain to me why deflation is bad? If it is bad.

English

@I_found_myself_ @om_patel5 I think it more efficiently monitors stealing and bad behavior. Honest people have known for years were being monitored.

English

@om_patel5 This is efficient, sure, but don't you think constant monitoring can seriously impact trust and morale?

English

this is insane

a coffee shop is using AI to monitor every employee and customer in real time

> how many cups each barista has made

> how long every customer has been waiting

> who's working fast and who's falling behind

walmart already does this across all their stores.

it's only a matter of time before every small business has access to this kind of tech.

English

@porterstansb @MrGlass2025 @Porter_and_Co I am very happy with my Berkshire Hathaway. Over 20% of my portfolio. I want to continue to sleep at night.

Why don’t we focus on getting Greg Able some great companies that he can acquire cheap that are exceptionally good.

Just spinning your wheels, pushing breaking it up.

English

In any given year, yes, of course that's true. But I'm measuring Berkshire's earnings by the decade. And, in that regard, I'm fairly certain Buffett would agree.

And of course, there are plenty of other signs of a material decline in the quality of the assets, including: major write offs at ALL OF Berkshire's largest take-private aquisitions since the GFC (Kraft, PCC, BHE) and a 30% (!) decline in operating earnings in the 4Q last year. In regards to the take-private deals, Buffett has cost Berkshire shareholders billions in losses. It's long past time for the Board to step in and restructure.

Berkshire used to beat the S&P 500 virtually every single year. Buffett long said the standard for retaining capital was to beat the S&P 500 over all rolling 5-year periods.

But today, Berkshire has only beat the S&P in 13 of the last 20 calendar years. And only once (by 0.5%) in the last three years.

As a result, Berkshire hasn't outperformed he S&P over the last decade.

And, more worrisome, Berkshire's performance (over the last decade) was largely the result of Berkshire's amazing investment into Apple Computer, which is unlikely to be repeated.

If Berkshire hopes to beat the S&P over the next 5, 10, and 20 years it must unlock the value of its insurance companies and its equity portfolio from the anchor of its poorly managed wholly-owned operating business -- most especially BHE and BNSF.

English