Sabitlenmiş Tweet

Doubled my $IREN position this week. I think a re-rating is imminent. My gut says they’ll be ordering a second, even bigger batch of Blackwells soon. That’s when the real fireworks begin IMO.

English

Jacques B.

1.2K posts

@JacquesBahou

Exploiting the disconnect between secular trends and asset pricing.

$IREN is executing one of the most elegant capital arbitrages in the history of digital infrastructure. 1. The Macro The investment thesis starts with a fundamental truth: The demand for compute is infinite. We are attempting to decode the source code of reality—solving biology, physics, and economics with math. To do that, we need uncapped intelligence. But intelligence runs on electrons. While the demand for answers is infinite, the supply of power is capped by physics and bureaucracy. We are entering an era where Power is the currency of discovery. The value of a committed electron in 2030 will be multiple times what it is today. $IREN is a leveraged long position on this specific physical constraint. 2. The "Triple Arbitrage" (The Real Engine) Most investors are missing the Capital Stack Arbitrage that the Roberts brothers (ex-Macquarie infrastructure bankers) have built. They are exploiting pricing inefficiencies across three different markets simultaneously: Arbitrage A: The WACC Gap (Debt vs. Equity) IREN borrows capital at Infrastructure Rates (low-cost debt backed by hard assets like land/substations) but deploys it into Tech Yields (20-30% ROIC on AI/Cloud). Most companies pay Tech costs for Tech yields. IREN pays Utility costs for Tech yields. The spread is pure profit. Arbitrage B: The "Float" (OPM) Microsoft is prepaying billions to secure capacity. A prepayment is a 0% interest loan. They are using the customer’s balance sheet to fund the CapEx. When your Cost of Capital is 0%, your Return on Equity (ROE) effectively approaches infinity. Arbitrage C: The Developer Spread They execute Greenfield Development at Replacement Cost (Commodity pricing for steel and chips). Once that center is stabilized with a hyperscaler tenant, it re-rates to an Infrastructure Platform (trading at ~24x EBITDA like Equinix). They capture the massive valuation spread between the risk of construction and the value of stabilization. 3. The “Terminal Value” Kill Shot Conventional analysis depreciates the infrastructure (Land, Power, Substations) to zero over time. This is financial malpractice. In a power-starved world, an Interconnection Agreement is one of the most appreciating assets on the planet. Amazon paid ~$677k per MW to Talen Energy for a hollow shell just to get the power access. IREN owns the "Grid Valve" in a world where the line to get a new valve is 7 years long. The Verdict $IREN is securing one of the scarcest assets in the world (Power) using the cheapest capital in the world (Microsoft’s Float) to generate one of the highest yields in the world (AI Compute).

$IREN is building a layered capital structure in which each completed project increases the company’s borrowing capacity for the next wave of growth. The first layer of that model is already visible. For the Microsoft contract, IREN said the GPU financing plus the customer prepayment covers about 95% of GPU-related capex, and that the facility is expected to be secured by the related GPUs and contracted cash flows. That shows the compute layer is increasingly financed at the asset and contract level rather than through equity. The second layer begins once construction risk is removed. After a data center shell starts generating stable cash flow, it becomes a fundamentally different credit asset than it was during development. At that point, IREN can borrow against the infrastructure itself, whether at the project level, portfolio level, or eventually corporate level. In the same Q2 FY26 materials, IREN explicitly said its financing workstreams include GPU financing, data center financing, and select corporate-level initiatives. Management is clearly building this stack in layers. The third layer is where the model compounds. As IREN’s asset base grows and cash flows diversify across more tenants, sites, and geographies, its credit profile strengthens. A broader and more diversified pool of hard assets and recurring revenues commands better financing terms than a single project standing alone. In other words, a larger and more diversified IREN gets to refinance and raise debt on better terms over time than a smaller, more concentrated IREN. That is the core insight: debt capacity is not static. It expands as the platform matures. First, debt is secured by GPUs and contracted project cash flows. Then, debt is layered onto completed and stabilized infrastructure. Later, broader corporate or portfolio debt is supported by the combined cash flows and hard assets of the platform. So each completed project does not just add revenue. It adds borrowing capacity for what comes next. IREN is essentially arbitraging cost of capital across different layers of the stack, using its vertical integration and growing asset base to move from narrow, asset-specific financing toward broader, lower-risk platform-level debt over time. This is also where the $6 billion ATM fits best. The ATM should not be viewed only as a dilution threat. In IREN’s case, it is optional firepower, not urgent need, especially given that the company is already cash flow positive and clearly has access to other forms of capital. Within this framework, a large unused ATM still strengthens the financing machine. Even if it is not tapped immediately, it increases balance sheet flexibility, improves counterparty confidence, and strengthens IREN’s hand when negotiating the next layer of debt. Lenders like knowing the borrower has an equity backstop available, even if management intends to use it only opportunistically. Put simply, IREN is building a self-reinforcing capital flywheel. It finances the compute layer with customer-backed and asset-backed structures. It then de-risks the infrastructure layer and adds debt against stabilized assets. As the portfolio matures and diversifies, it gains access to broader and cheaper corporate or portfolio debt. The ATM sits on top of that structure as optional equity capacity, supporting negotiations and giving management flexibility to issue shares selectively when the cost of equity is attractive. In that model, the same equity dollar funds multiple growth cycles instead of being trapped inside a single project. That means lower dilution than the market assumes and better returns on equity over time as mature assets are refinanced into new growth. If management keeps turning contracted GPUs into asset-backed debt, completed shells into refinanceable infrastructure, and a growing asset base into lower-cost platform-level borrowing, then IREN’s capital structure becomes one of its biggest competitive advantages.

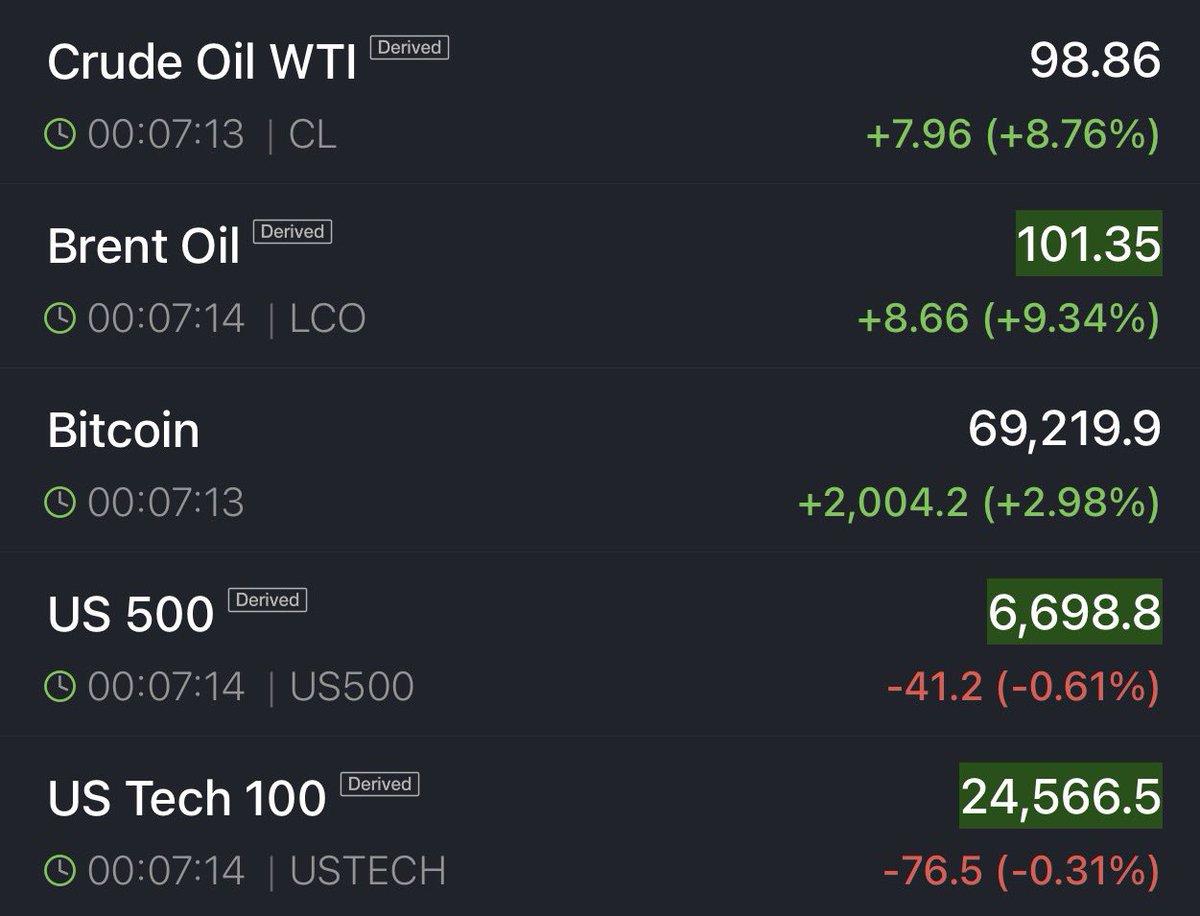

Am I the only one that just flipped bullish when: - Retail on X - Regards on WallStreetbets - Jim Cramer Are now all doomposting indexes and are: Either are long crude oil contracts or think oil is going to $150-$200?

$IREN $6 Billion ATM is massive. For the people who hold $IREN, the truth you might not want to hear is: -> Wait until existing holders get diluted to oblivion -> Use them to "buy the dip" of $6 Billion in new shares for you. -> Go long after. If you're long now: That inevitable $6B in new shares + selling pressure structurally caps upside in your equity and serves as a overhang in any rally. Companies don’t file a $6B ATM not to use it. They will, and as much as they can on any rally. The reality is that there are other financing methods, but ATMs are the most destructive ones to retail shareholders. $IREN itself is a solid company unlike movie theater stocks, but like excessive dilution referenced: You will likely see the marketcap of $IREN go up back toward $20B, but the your share prices tanking in value. TLDR: The harsh reality is $IREN might fundamentally succeed and build a massive DC footprint. But it's at the cost of heavily diluting retail shareholders. Retail investors should care more about the value of their own stock increasing over the company's value. Disclosure: I have zero economic interest or positions in the company, but I do care about prioritizing retail interest.