Dylan@dylan_teeter

Here is a little write up I did using Grok AI for fun the other day:

Bullish Thesis: Cipher Mining and IREN - The Convergence of Bitcoin and AI Powerhouses

Bitcoin mining stocks like Cipher Mining (CIFR) and IREN Ltd (IREN) are poised for a transformative rally, driven by their undervalued assets, strategic power pipelines, and the explosive convergence of Bitcoin and AI infrastructure demand. These companies, originally built for mining, are sitting on real-world infrastructure that mirrors the early days of cell towers and data centers—sectors that delivered 100x-200x returns over decades. With hyperscalers racing to secure power for AI and HPC, Cipher and IREN’s large-scale sites position them as critical players in a multi-year capital expenditure (CAPEX) cycle.

#### Historical Parallels: Infrastructure Wins Long-Term

Tom Lee’s analysis of the 1990s wireless broadband boom offers a compelling analogy. That 20-year CAPEX cycle saw cell tower companies like American Tower (AMT) and data center operators like Equinix (EQIX) emerge as the biggest winners. AMT, trading at $2.50 in early 2000, now sits at $225 (a ~90x return), while EQIX, at $3 in 2002, has soared to $900 (~300x off its bottom). These gains peaked around 8-10 years into the cycle, fueled by real-world infrastructure that scaled with demand. Dan Ives pegs the AI buildout at 8-10 years from ChatGPT’s 2022 debut, suggesting a 2030-2033 peak. If Bitcoin miners follow a similar trajectory, stocks like CIFR and IREN could see outsized gains by 2030, leveraging their power assets for both mining and HPC.

#### The Power Bottleneck: Why Miners Matter

The AI arms race is real, and power is the bottleneck. Sam Altman recently highlighted at a Morgan Stanley conference that hyperscalers need energy now—not in 2030. McKinsey projects data center power demand will hit 35 GW by 2030, up from 17 GW in 2022, while Morgan Stanley echoes similar growth. Pre-AI, 30 MW sites were standard; now, hyperscalers like Meta and Stargate demand gigawatts. Jensen Huang of Nvidia recently noted computation needs for AI are 100x higher than anticipated a year ago. Where will this power come from? Bitcoin miners, with their foresight in securing large-scale sites, hold a first-mover advantage.

Hyperscalers could buy sites directly, but energization timelines are a chokehold—many recent purchases won’t come online until 2029 or later. Nuclear power, once hyped, won’t deliver until 2030 at earliest, and contracts often have opt-out clauses with no upfront cash, limiting downside for buyers but delaying deployment. Meanwhile, miners like IREN and CIFR have sites energizing in 2025-2027—rare and valuable real estate. Open AI’s choice of Abilene, Texas, for its first major data center (a site originally secured by a miner) proves HPC can thrive in non-metro areas like West Texas, debunking pre-ChatGPT assumptions and validating IREN’s strategy.

#### IREN: A Misunderstood Powerhouse

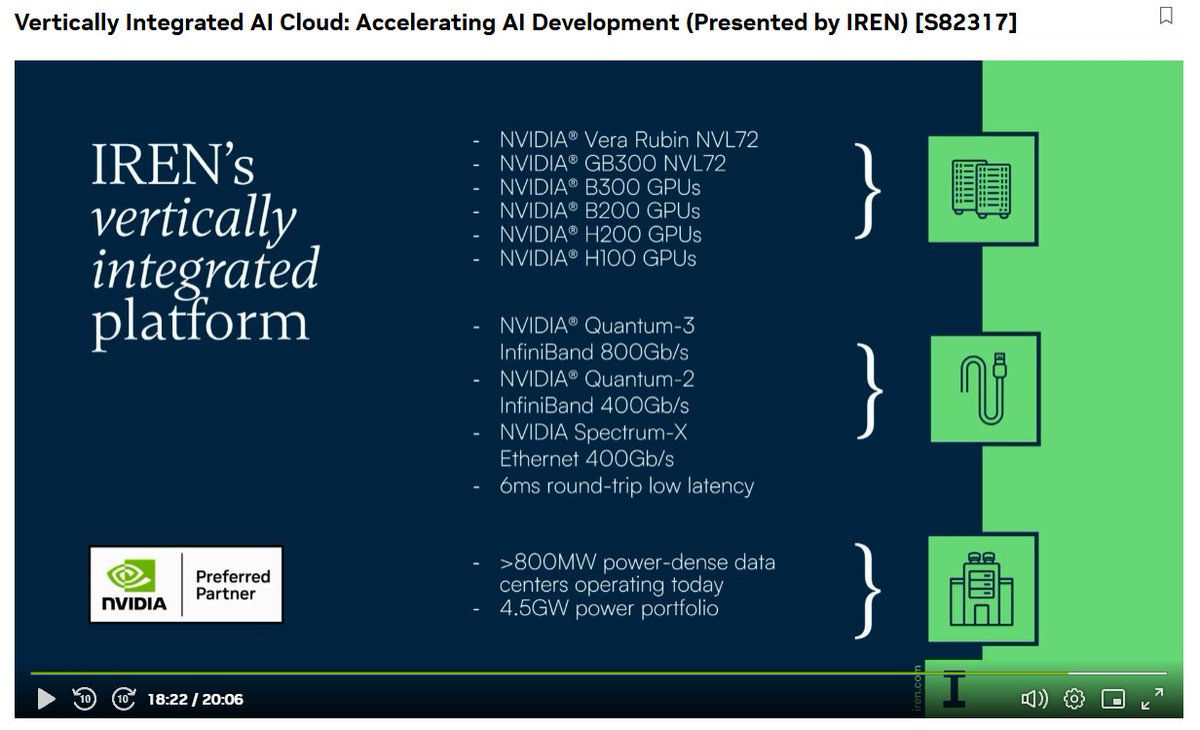

IREN’s early bets on massive greenfield sites, like its 2 GW Sweetwater Data Center Hub near Abilene, have ballooned in value—potentially 100x since acquisition, as noted in discussions with Mike Alfred. Before AI went mainstream, IREN saw the potential in scalable, remote power. By June 2025, IREN will hit 50 EH/s in mining capacity, projecting $500 million in annual cash flow at $80,000 Bitcoin—with zero debt. Its 75 MW liquid-cooled AI data center, set for delivery soon, and ongoing customer diligence for its Horizon 1 project signal HPC traction. The market undervalues these assets; IREN’s enterprise value likely exceeds its current market cap, especially as narratives shift from “just a miner” to a dual Bitcoin-HPC play, akin to Amazon’s pivot from bookstore to AWS.

Pt 2 ⬇️