BioSniper retweetledi

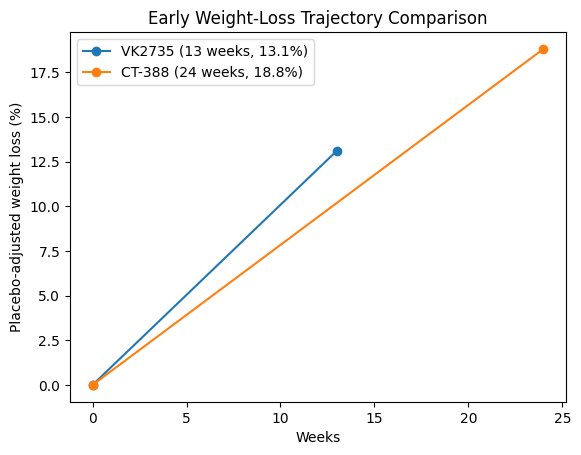

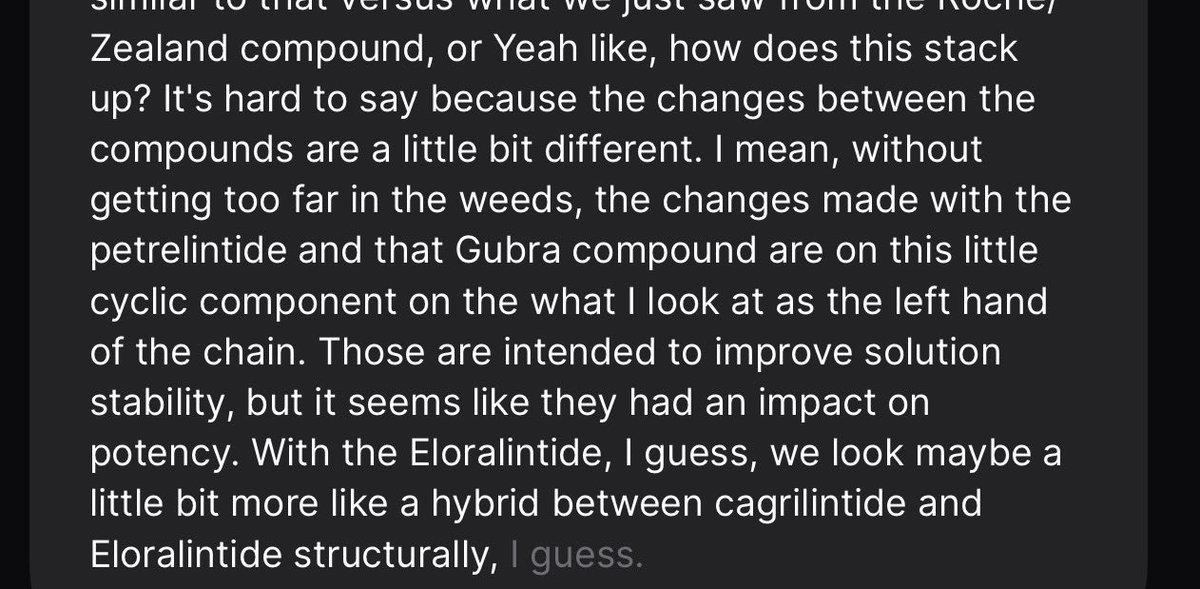

$VKTX CEO today comparing different amylin structures. He commented on $zeal & $ABBV GUBRA structures , that attempts to improve solution stability might have harmed efficacy ( I would call this potential indirect hit to ABBV that was defending its compound within the same conference)

Viking DACRA is a structural hybrid of $LLy Eloralentide and $NVO cagrilintide

And more potent than VK2735 in obese monkeys.

English