$HFG at <2x EV/adjusted EBITDA seems worth another go. Unrelated, but they must wish they had a higher-margin business they could leverage their customer base in, ad business is really transforming other previously low-margin retail businesses these days.

@jacobsogaard@PerNordnet no "subject to agm approval"

Just the board and the management deciding to do this on their own. They should be fired, the whole lot.

@jacobsogaard@PerNordnet Pretty tone deaf of the board and management to make a deal selling the most valuable asset of the company, without asking any shareholders and without any "out" - wont comment on breakup fee, wont comment on lockup and says this is a "done deal" with no chance of a higher bid

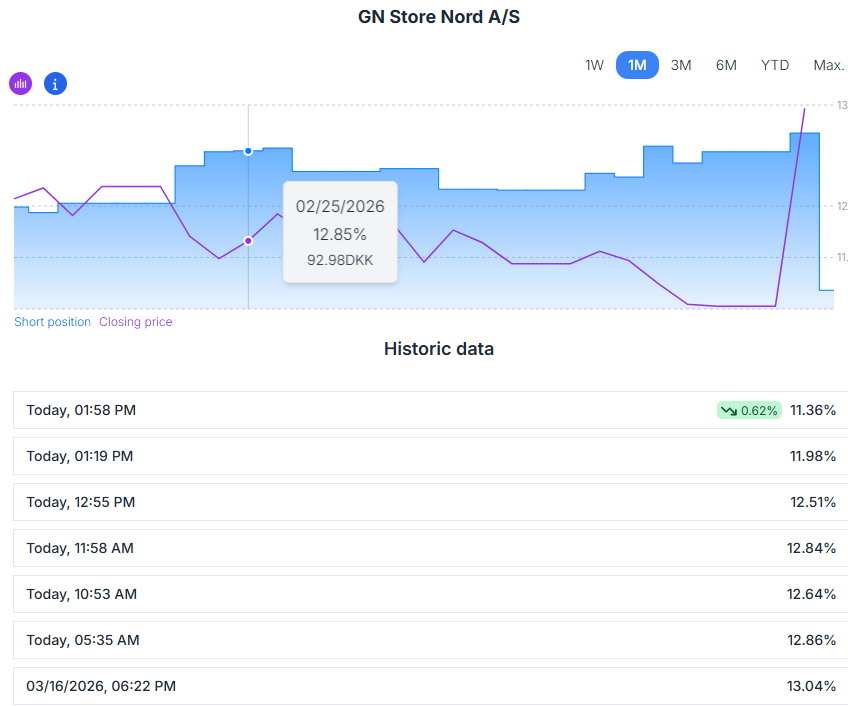

Investortræthed i GN Store Nord? Oh, yes! Investorerne er udmattede efter for mange fejlskud. Der er gang i short nedlukningen. Tankevækkende, at der kan købes mere end 250.000 aktier tilbage uden at det har nogen som helst kurspåvirkende effekt #aktier#dkbiz

Figur: GN Store Nord - aktiekurs vs shortsalg

Kilde: zirium.dk/short-watch-de…

@Spsk2000@financeamir i mean sure but flat guidance YoY and one quarter doesnt really matter

They have yet to return to anything that isnt mid to high single digit revenue decline while they "churn through low value customers" (how long should they be allowed to use that excuse for?)

@JohnnyP31915@financeamir It is better than it looks.

"FCF highest level since 2021."

"We grew MK AEBIT from EUR 365 million in 2024 to EUR 486 million in 2025" +33%

"Regarding RTE, while the full-year margin was slightly negative at -1.2%, the category returned to a positive 6.6% margin in Q4."

@Spsk2000@financeamir Their buybacks has been mostly been funded by cash already in the company, not cash flow, and their "efficiency reset" continues by shedding revenues and barely having positive fcf

GN Store Nord sells Hearing Aid business, almost half of their turnover and profits, and, for most people, the best division within their company

And the decision was made purely by mgmt & BoD. And shareholders have absolutely no say in this although the CEO "respects them"

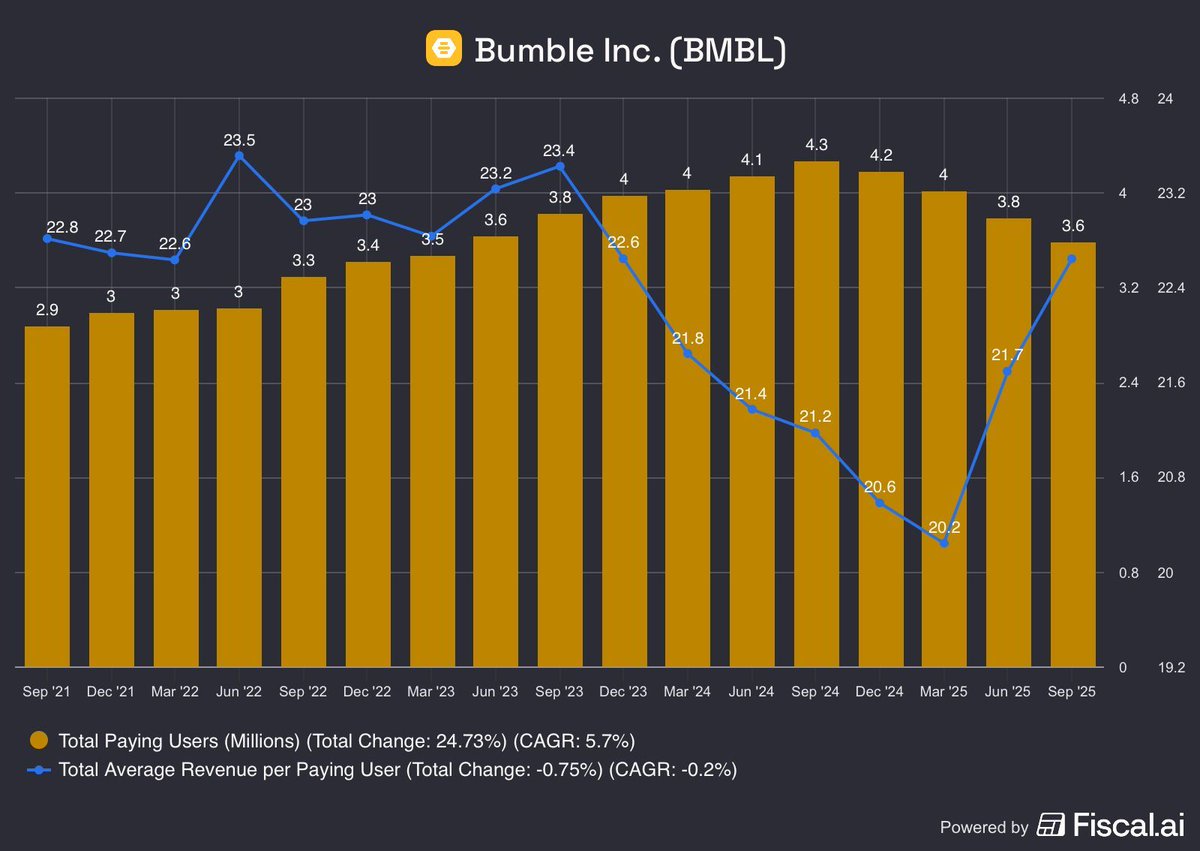

$BMBL is one of the most interesting potential turnaround plays on the market right now.

P/FCF: 1.73x

They generated $173.8M in free cash flow TTM on a $310M market cap. That’s not a typo.

I don’t own it yet. Here’s why:

🔴 The turnaround signal isn’t clear enough — outside of founder Whitney Wolfe Herd returning as CEO, there’s no definitive inflection point.

🔴 Total users are still declining steeply.

But the bull case is building:

🟢 17% FCF margin TTM — legitimately strong

🟢 Average revenue per paying user is recovering nicely

🟢 The returning founder/CEO owns ~15% of the company — serious skin in the game

From a pure valuation standpoint, this is one of the cheapest names I’ve seen.

The market is pricing in continued deterioration, but if Wolfe Herd can stabilize the user base and monetization keeps improving, the re-rate potential here is massive.

Watching this one closely.

@MultibaggerRsch@mauerstrasse if you search for "assuming the exchange of all outstanding common units" in the 10-qs, you will find the number. The number i use (for Q3) is 151m shs. vs the 100+ or so class A shs

Still "cheap" thou

@Jontaspontas@pensionspengar because it is the most secure and reduces the reliance on employees staying up-to-date? The product is for enterprise customers

Lyko vinstvarnar och inleder kostnadsbesparingsprogram, vd och grundare flyr till sociala medier för att krysta fram några av de vackraste krokodiltårar mänskligheten bevittnat

$yubico trading at 15.5x 24 earnings, 32.0x 25, 18.7x 26 and 14.2x 2028 earnings

Should be good revenue growth in the years ahead, and a lot higher margins (why is their target EBIT margin only 20%???? They already reached that in 2024)