Sabitlenmiş Tweet

Sohra Peak's Q4 2025 partnership letter is now available here:

sohrapeakcapital.com/partnership-le…

English

Jon Cukierwar

777 posts

@JonCukierwar

Founder of Sohra Peak Capital Partners, where we invest in businesses with intelligence far surpassing my own. Disclaimer here: https://t.co/C1dK5tzAej

@HYcorps DBOX is laughable here. Apparently people don’t realize they can track the box office in near real time.

Paramount Says It Will Release 15 Warner Bros. Movies a Year in Theaters, Reaffirms 45-Day Theatrical Window variety.com/2026/film/news…

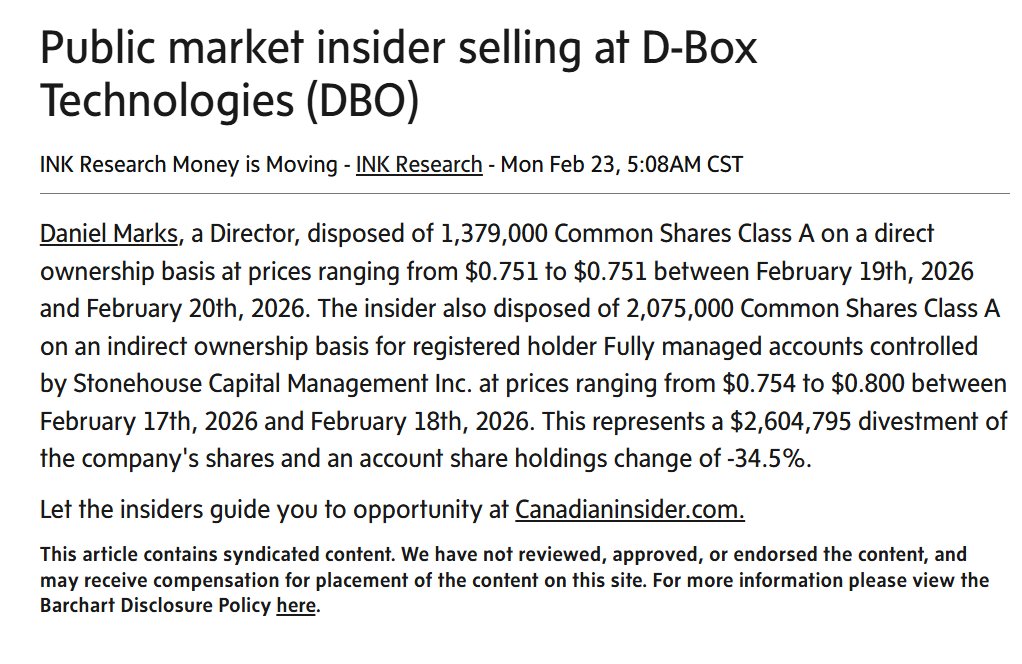

Thanks @DrJebaim for sharing this. $DBO.TO BoD member Dan Marks has sold D-BOX shares -- at $0.63/sh in Nov, $0.90s in Dec, $0.70s last week, and I wouldn't be surprised if continuing this week. While certainly not to be dismissed, I think this is an action to be considered on balance with other related facts: - Marks's average cost basis is likely between $0.10-0.20/sh. - Marks is an investment manager, and D-BOX is still likely a highly concentrated portion of his portfolio. - CEO, CTO, CCO, and 2 other BoD members have all made insider purchases over the past 6 months, many at or above current prices. We don't know exactly why Marks is selling, but given CEO Naveen's positive comments last week in his MicroCapClub interview (youtube.com/watch?v=rRQW7E…), I'd be surprised if Marks's sales were due to some negative surprise that the BoD is privvy to - and that other BoD members and C-suite executives seem to be buying in to. A few quotes from Naveen's presentation: - "Scott as a Chief Commercial Officer, we are talking to everybody" discussing theater chains. - “There are absolute signals that we have more room to grow [with Cinemark U.S.]” - "there was a focus on growing product sales across broad markets. We are refocusing. They are long lead periods for sales. So I'll leave it at that." Implying to me the potential for future theater chain wins. - "We do see an opportunity for financing and we want to make sure that we are exploring as a priority something that will continue to grow our profitability and compound that royalty revenue." D-BOX mentioning for the first time financing as a tool to accelerate screen count growth. Disclaimer: This information is not intended to be and does not constitute investment or financial advice. You should not make any decision based on the information presented without conducting independent due diligence. Sohra Peak Capital Partners LP and/or its affiliates including myself hold a position in the security mentioned and may change that position at any time. Please carefully read the disclaimer included and linked in my profile biography.

$DBO.TO $DBOXF Large insider purchase of 130k shares at $0.80/share