@molusol @FabianoSolana They should buy/team up with bulk or phoenix. Would be blockbuster

English

Jon.sol

1.1K posts

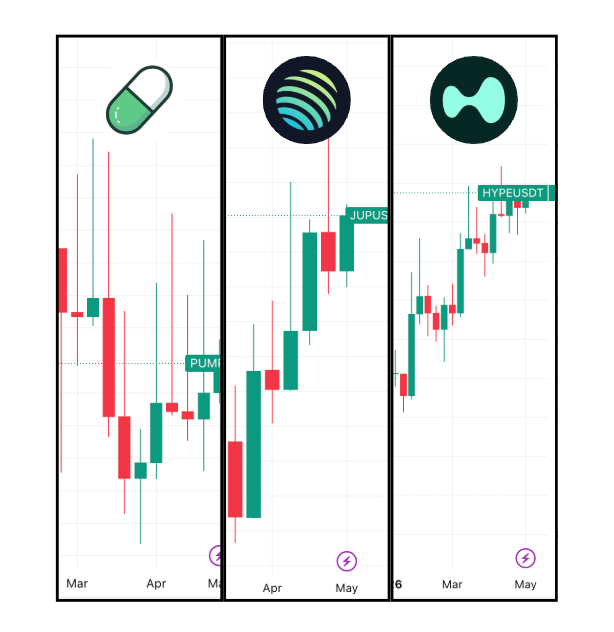

Our new report "Jupiter: A Gassed Up Giant" is Live and Free to read! @JupiterExchange did $184M in protocol revenue in 2025 with no venture funding and a near-zero capital base. JUP now trades at roughly 9x annualized revenue while Aave trades at 20x. The disconnect comes down to categorization. The market sees a cyclical DEX aggregator, but the team has spent the last 18 months shipping 10+ new product lines while defending 80% of Solana spot aggregation. What makes this durable is the product flywheel underneath it. Perps auto-route collateral swaps through the aggregator, generating billions in spot volume as a byproduct. JLP earns yield from perp fees and a third of its AUM flows into Jupiter Lend as collateral. Jupiter ranks as the third-largest perp earner behind only Hyperliquid and EdgeX. When JupNet goes live and GUM opens access to equities, commodities, and forex, every new asset class feeds volume across the entire stack.

every coin wants to be listed on @solana > ripple (XRP) > hyperliquid (HYPE) > avalanche (AVAX) > monad (MON) > bitcoin (BTC) > ethereum (ETH) > sui (SUI) > paradex (DIME) > lighter (LIT) > infinex (INX)

JUST IN: 🇺🇸 Treasury Secretary Bessent calls for Congress to pass crypto market structure legislation before it's too late. "Time is scarce, and now is the time to act."

I rarely talk about politics but I also stand up for my beliefs Anyone celebrating this war is sick in the head

BREAKING: 🔴🔴 U.S. PRESIDENT DONALD TRUMP: "A SHORT TIME AGO, THE UNITED STATES MILITARY BEGAN MAJOR COMBAT OPERATIONS IN IRAN."