Joshua Webster

2.5K posts

Joshua Webster

@JoshuaDWebster

Building Roll Up Vehicles and Consolidation Vehicles at @RollupsHQ

Katılım Haziran 2020

1.6K Takip Edilen396 Takipçiler

Of course, his spring break is the week of YC/HF0 demo days, RSA, and Hill & Valley

Big brother-ing for once instead of treating everything as more important than family

I’ve added golfing, clothes shopping, & dinner at Quince to the docket, but need something he’ll remember🤔

English

My little bro (18) is at Georgia Tech on a full ride for aeroeng. He’s staying with me all week in SF & I’m looking to experience-max while he’s here

All I have planned is soccer w my MLS friend at the stadium & a GSW game

Cos building cool stuff, events, etc. Please invite us!

English

English

English

My take on Delve and experience after 3 audit cycles as a founder ->

We've been a decently happy customer of @secureframe the last few years but were considering migrating to @getdelve this January (took some sales calls, got some data in to feel the experience). Here's my take on the situation:

I've done 3 audit cycles now where my team (and originally just me) spent weeks every quarter pulling data, filling out spreadsheets, etc to adhere to SOC 2 controls. This was followed by a painful 2-3 month audit period where I felt auditors and the underlying platform were heavily out of sync - auditors would request things that we had already synced/uploaded into the compliance tool, escalatory meetings would happen just to resolve to 'that is ok, sorry we missed it'.

The promise of Delve, for me, was AI-native compliance.

A platform that didn't just do 80% of the work (controls auto-synced to cloud infra, evidence pulled via vendor APIs) but got us to 95%: where agents did the annoying stuff that the other platforms couldn't handle (auto checking access roles in every vendor, filling out excel sheets first to then to hand over for human verification). Where auditors actually understood the platform holding the evidence they were auditing.

I was really onboard with the vision of Delve their team and sales folks pitched me.

My gripe with all the existing vendors (@TrustVanta , @DrataHQ, @secureframe ) was this:

They built their tech stack and process up up pre-AI. I felt their product roadmap moved very slow, lots of small bugs everywhere and so much silly stuff has to be done manually. One hour my team is orchestrating coding agents and the next hour huddled in a call filling out an Excel sheet - it felt like these existing platforms were 'on the wrong exponential'.

We're obviously sticking with Secureframe for now but the above facts still haven't changed. Im certain someone will disrupt the space by achieving the above vision - it's unfortunate that it probably won't be Delve.

English

Yesterday, 11 months after I started, I got the final commit for fund 1

I raised 525k in 2 days. I thought I was made. 6 mo later, on Oct 1, I’d only signed 1.7m

Fund returns helped, but the only change I made was to unapologetically be me. Being authentic pays, it’s just hard.

English

@aashaysanghvi_ ngl I didn't know jasper was still around

English

The companies with the most mindshare in AI: OpenAI, Anthropic, and Jasper.

English

Capital, like people, goes where it is welcome and stays where it is well treated.

Treat capital badly, it leaves.

So then the people in govt (+ those who elected those people in govt) who treated capital badly need to treat capital even worse.

so dumb

Joe Lonsdale@JTLonsdale

In CA this month, we’re literally required as a venture firm to ask each of our CEO’s in a survey if they are gay. Meanwhile today in Texas the voting machine is like, Y or N, “Ban gender nonsense in K-12?” “Ban sharia law?” 🇺🇸

English

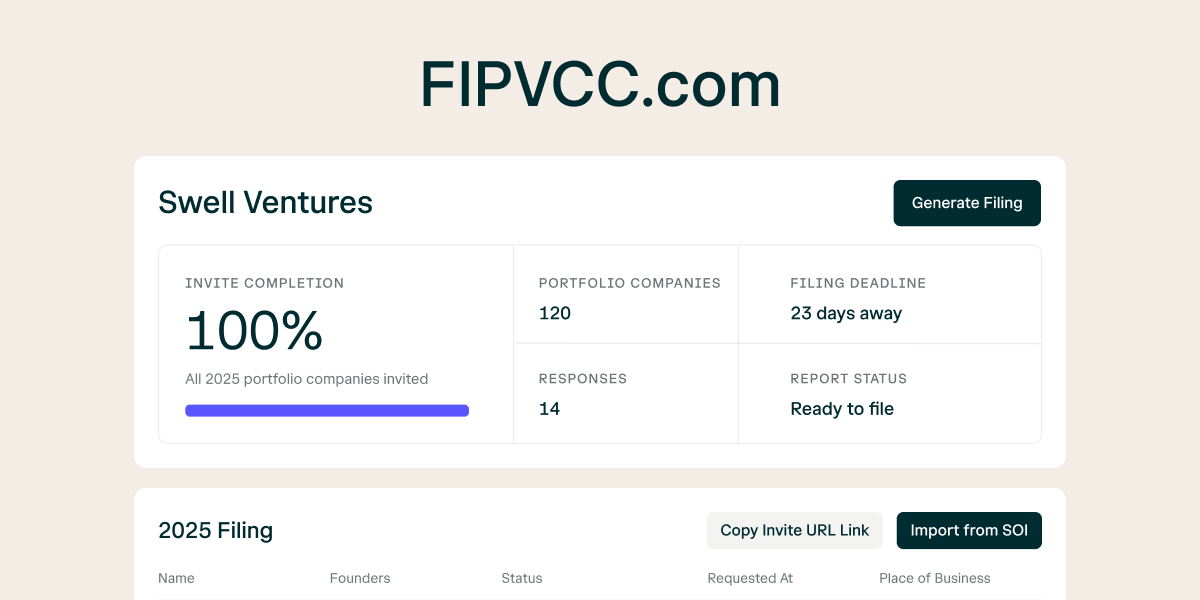

@JTLonsdale Check out FIPVCC (dot) com -- can collect the info completely privately (zero-knowledge compliance)

English

In CA this month, we’re literally required as a venture firm to ask each of our CEO’s in a survey if they are gay.

Meanwhile today in Texas the voting machine is like, Y or N, “Ban gender nonsense in K-12?” “Ban sharia law?” 🇺🇸

English

Joshua Webster retweetledi

Or how about we let free market capitalism work and let American companies innovate and win without burdensome red tape and regulations on top of government bureaucrat central planning on pricing and distribution? This is not some magic chip alchemy. It’s just the next generation of compute. The AI doomsday narrative is conflated and not based on technology reality. If bureaucrats were in charge during the PC revolution, American x86 and WinTel would not have been able to dominate for decades. Free markets work. Government involvement and intervention generally does not (hello Soviet Union).

If the government was smart, they would do a nuanced strategy of letting China remain on CUDA but one or two generations behind (keeps USA ahead) - instead of literally creating a chip competitor ecosystem with tens of billions of R&D oxygen from the biggest chip market in the world.

Basically, let Nvidia cook.

English

Joshua Webster retweetledi

When I was 7 years old I was asked by my father what went into the price of a sandwich. Considering it carefully, I answered.

The lettuce, the tomato, the bread and the meat.

I did not consider correctly. I was short quite a few costs as my father was eager to point out. I had forgot the labor of the worker, the rent of the land, the marketing costs of the chain. I wasn’t seeing the full picture.

Today we are all making a similar mistake with AI. We are not considering what cannot be considered. As foreign to the 7 year old as these excess charges were, so are the downstream affects of AI.

In 1850, if you had told a teamster that his horse and carriage would soon be obsolete, he would have envisioned a world of mass starvation for men of his skill. He could grasp the concept of a faster carriage, but he could not conceive of the interstate highway system, the suburban real estate market, or the roadside motel industry. These were not just new products; they were an entirely new social architecture.

We are currently in the teamster’s shoes. We see AI automating the ingredients of our current economy—the writing, the coding, the data entry—and we fear the void. But history shows that humanity doesn't fall into the void; it builds a floor over it.

Karl Marx looked at the dark satanic mills of the 19th century and saw a terminal point. He argued that as the means of production became more efficient, capital would consolidate and labor would become a worthless commodity. He believed capitalism would eventually eat itself because it would run out of things for people to do.

Marx was wrong because he viewed human utility as a fixed pie. He didn't understand that technology doesn't just subtract labor; it changes the nature of what we consider valuable.

When the mechanical loom made fabric cheap, we didn't stop buying clothes. Instead, we invented the fashion industry. We created brand management, retail psychology, and textile engineering.

We moved from a world where everyone owned two outfits to a world where millions of people are employed in the cycle of seasonal trends.

In the age of the steam engine, "handmade" was a sign of poverty. Today, it is a luxury. We are already seeing a shift where the human touch—the artisanal, the face-to-face, and the physically present—is becoming the high-margin sector of the economy.

Every time we automate a simple task, we move the human to a more complex one. We didn't stop needing accountants when Excel was invented... we simply started asking accountants to perform much more sophisticated financial modeling.

The 7-year-old misses the rent and the marketing because they are abstractions. Similarly, we struggle to see the jobs of 2040 because they rely on problems we haven't even encountered yet. We might see the rise of Personal Data Stewards, who manage the interaction between our private lives and public AI models, or Reality Architects, who ensure that the virtual spaces we inhabit are psychologically grounded.

The world works itself out because humans are fundamentally restless. We do not tolerate a vacuum of purpose, we seek higher function always.

English

Joshua Webster retweetledi

A new California law (FIP VCC) is forcing VCs to ask portfolio company founders about their sexual orientation, disabilities, and more – all so it can be reported to the state.

We built a new system to help funds on AngelList comply without ever seeing individual founder responses.

To preserve founder privacy everywhere, we've decided to make the system available to any fund for free, regardless of who they work with for fund admin.

You can use it today: fipvcc.com

English

David Marcus, former president of PayPal has a great take on what happened- PayPal stopped being product led and was financially led (poorly!)

x.com/davidmarcus/st…

David Marcus@davidmarcus

A few thoughts about PayPal, nearly 12 years after I left. I woke up this morning to dozens of messages from former PayPal colleagues. It pushed me to finally speak up. I never spoke publicly about the company after I left. Part of that was loyalty to John Donahoe, who gave me an unlikely opportunity, handing the reins of PayPal to a startup guy who, on paper, had no business running a then 15,000-person organization. But part of it was something else: I had left. I chose not to stay and fight for the changes I believed in. Speaking from the sidelines felt like armchair commentary. Easy opinions without the burden of execution. So I stayed quiet. But twelve years of silence is long enough. And today's news makes it clear the pattern I've watched unfold isn't self-correcting. I left PayPal in 2014 because I was deeply frustrated. We had executed a silent turnaround of a company that had lost its soul. We brought back engineering talent, shipped good products quickly, and acquired Braintree and Venmo. The company was on a tear. So much so that Carl Icahn felt compelled to accumulate a position in eBay and push for a PayPal spinoff. At the time, eBay decided to fight Icahn. It was a difficult period for me, caught between what I felt was right for PayPal and my loyalty to the eBay team. This is when Mark Zuckerberg approached me to join Facebook. The combination of his conviction that messaging would become foundational, the appeal of going back to building products at scale, and my growing exhaustion with the internal politics at PayPal and eBay eventually convinced me to leave and join one of the best teams in the world, one I had admired for a long time. In the summer of 2014, I met John in a café in Portola Valley and told him I had decided to leave. During that conversation, he told me that Icahn had effectively won the fight, that PayPal was going to become an independent company, and he tried to convince me to stay on as CEO, but I had already said yes to Mark, and my word is my bond. There was no turning back. After my departure, the board scrambled to find a replacement, and it took a few months for them to land on Dan Schulman. The leadership style shifted from product-led to financially-led. Over time, product conviction gave way to financial optimization. Much of the momentum we had created still persisted and carried the company forward, mainly driven by Bill Ready, who came over in the Braintree acquisition and rose to COO. Under his leadership, Venmo grew exponentially, and total payment volume (TPV) accelerated quickly. But the shift under Schulman became more pronounced after Bill's departure at the end of 2019. With him went the product conviction that had defined the post-spinoff momentum. Then, for a period, COVID-fueled online shopping hid a lot of the company's new weaknesses. During that period, the company made a fundamental miscalculation: it optimized for payment volume instead of margin and differentiation. It leaned into unbranded checkout, where PayPal had the least leverage, instead of branded checkout, where the margin, data, and customer relationship actually lived. Visa masterfully structured a deal that effectively ended PayPal's ability to steer customers toward bank-funded transactions, which had been a core driver of PayPal's economics. Not long after, PayPal lost a significant portion of eBay's volume. Over time, it saw its share of checkout among its most profitable customers steadily erode as Apple Pay and others continued to execute well. The same pattern repeated itself across lending, buy-now-pay-later (BNPL), and new rails. On lending, PayPal missed the opportunity to turn it into a platform weapon. Products like Working Capital were conservative, short-duration, and optimized for loss minimization. Lending never became programmable, never became identity-driven, and never became a reason for merchants or consumers to choose PayPal over something else. The missed opportunity in BNPL was even more striking. Klarna, Affirm, and Afterpay didn't just offer installment payments, they built consumer finance brands, persistent credit identities, and new shopping behaviors. PayPal saw the BNPL turn, entered the market, and had every advantage: distribution, trust, and merchant relationships. But BNPL was treated as a defensive checkout feature rather than an offensive category. There was no attempt to turn it into a core consumer relationship, no super-app behavior, and no meaningful differentiation for merchants. Others built platforms, PayPal added a feature. The failure to lean into building and owning new rails followed the same logic. After the spinoff, PayPal had a once-in-a-generation opportunity to build a global, at scale payment network. Instead, the company focused on building on top of existing networks and third-party rails. More recently, that mindset carried over to PYUSD. Technically, the product was sound. Strategically, it launched without a compelling transactional reason to exist. PYUSD had distribution, but no organic demand. It was not embedded deeply enough into flows to become a true settlement layer, a cross-border merchant rail, or a programmable money primitive. It sat adjacent to the product instead of inside the core of it. Acquisitions during this period followed a similar pattern. Honey was not a strategic acquisition for PayPal. It added activity, but not leverage. It lived outside the transaction, monetized affiliate economics rather than payment economics, and never meaningfully strengthened PayPal's control of the customer or the checkout moment. Xoom solved a real problem in remittances, but it never compounded PayPal's advantage. It scaled volume without changing the underlying rails, identity graph, or settlement model, and as importantly, it didn’t cater to a high-value, high-margin customer archetype. None of these were bad companies. They were just a wrong fit for PayPal and became unnecessary distractions. The board eventually recognized the problem. In 2023, they brought in Alex Chriss, an Intuit veteran with a strong product background, explicitly to restore product conviction. It was the right instinct. But Alex came from software, not payments. He understood SMB product development. He didn't have the muscle memory for transaction economics, network effects, or settlement infrastructure. In hindsight, he also made an error: clearing out much of the leadership team that understood payments deeply. Executives with years of institutional knowledge departed within his first year. This morning, Alex was removed as CEO. Branded checkout grew 1% last quarter. The board tapped another operator, Enrique Lores, the former HP CEO who's been on the PayPal board for five years. I don’t know Enrique. And he might be a great leader, but on paper at least, he’s a hardware executive. For a payments company. The common thread through all of this is incentive design. Once PayPal became independent, short/medium-term predictability beat long-term vision and ambition. Stock performance mattered more than platform risk and network opportunity. Financial optimization replaced product conviction. I'm not claiming I would have made every call differently. Running a public company at scale involves tradeoffs I didn't have to make after I left. But the pattern, choosing predictability over platform risk, again and again, was a choice, not an inevitability. Over time, the company that had every advantage and could’ve become the most consequential and relevant payments company of our time, lost its mojo, its product edge, and its ability to compete in a market that’s being rewired and reinvented in front of our eyes. That's the part that's hardest to watch for a company I care so deeply about.

English

PayPal is the biggest missed opportunity in all of tech- it should have been a trillion-dollar company.

They have a two-sided bank-connected consumer + merchant network at global scale!

They replaced the CEO today. I do not think a 35 year veteran of HP is the solution 🤮

English

Garry Tan: Can you not seize our assets to waste on useless stuff no one asked for?

Ro Khanna: I’m thinking… an industrial development bank? Ooh I know, how about social media with a portable social graph?

…

Ro Khanna@RoKhanna

I admire your work with YC and agree start ups are key. Would you support 1000 trade schools, an industrial development bank, AI literacy in K-12, tech job centers across California & America, $10 day childcare (for care jobs), high pay for home care workers with AI tools, Medicare for All so we don't have job lock and can have more founders, an open social web to allow portability of social media graph...there may be some overlap.

English

@alexisohanian @PhilipJohnston How do you manage cooling a datacenter/GPUs in space?

English

Joshua Webster retweetledi

Introducing: Secondary Vehicles

Now companies can run their own secondary SPVs for delivering liquidity to shareholders without the predatory SPV fee/carry structures.

English

Joshua Webster retweetledi

"I'm raising a round, can you introduce me to X investor"

— question i've had 1,000 times in the past 10 years. and another 1,000 times in the past 10 days 😆

Answer is often* "yes - but please send me something forwardable + easily parsable, give yourself best chance of passing the 2-second inbox scan test"

Back in 2015 i was the guy who wrote all the "featured startup" emails at AngelList .. email blasts sending out "active rounds" to thousands of online investors. I had the unique privilege of @nivi breathing down my neck, helping pedantically craft every word until we got the formula, format just right. That formula is the one i still use/recommend today. I've been meaning to share it in public, so i can sign-post back for founders requesting intros.

And, here we are.

So. If you want me to fwd something to someone for you, please send:

four bullet points. no more, no less.

Each bullet is one sentence, maybe two.. but it's not an excuse to write a paragraph.

1) what does your company do, what problem are you trying to solve?

2) what traction do you have, or how do you know it's working. why is this notable?

3) who is your team, why are they the right people for the job?

4) what's your fundraise status - past & future plans? "raising a seed round, targeting ~$X. ~$Y committed so far, led by ABC. Prev raised ~$Y from D, E, and F."

#4 can be a hard one, highly dependent on where you're at in your journey....maybe you're just testing the waters on the round, in which case say that - "planning to go out for a pre-seed next month." If you list investors as committed/previously invested, make sure they actually are (and ideally investing again) because someone will probably ask them.

Founders, does that help?

Other investors, what would you suggest/iterate on this format? What's your dream intro request to receive?

English

Joshua Webster retweetledi

Mo (founder of @frecfinance, backed by Greylock) used an RUV to raise $5.6M from his top customers.

RUVs have grown entirely through word of mouth. Founders, investors, and lawyers love them. We did very little marketing and no advertising; we just focused on building a great product.

Mo Al Adham@maladham

We just raised $5.6m from our top customers on Frec, and the round was oversubscribed in under 48 hours! Here’s how it all went down. Customers have been asking to invest in Frec since we launched, so we kept track of those who asked, provided valuable feedback, or referred customers. The list started growing quickly after launching long short. Although we had the bulk of our Series A still in the bank, we saw an opportunity to make our top customers owners in Frec. So I pitched the idea to the board. The pitch was simple. Customers who want to invest work at some of the most impressive companies in the world, like Nvidia, Meta, Apple, Netflix, Snowflake, Databricks, Stripe, Shopify, Uber, Robinhood, Plaid, Workday, Block, Two Sigma, JP Morgan, and more. Their colleagues are exactly the type of people who could benefit from Frec the most. Offering these customers ownership would create an incredible customer advisory board. The board agreed. And when I sent the invites to the customers, the reactions were heartwarming: “Heck yes, I’m 100% in. Thank you for thinking of me for this. I’d love to be part of it. You know I’m very bullish on Frec’s future.” “I am impressed with how smart it is to engage your best customers with ownership this way.” “I'm glad to be a customer and now glad to be an investor. Eager to see how things grow and develop.” …and many more 🙏 So we raised the money in a YC SAFE note for a fast and efficient close, and we used an AngelList Roll Up Vehicle (RUV) to keep our cap table clean. I’m excited to welcome our newest investors. We always value customers who engage with us and hope to include more of them as investors in future opportunities.

English