KCM

75 posts

KCM

@KCapMngmnt

I invest in and follow undervalued companies, special situations, or businesses that have durable competitive advantages.

Katılım Ocak 2022

111 Takip Edilen157 Takipçiler

BREAKING: Apollo Global Management is reportedly nearing a $10 billion acquisition of Atlantic Aviation, in partnership with GIC, acquiring the asset from KKR.

Atlantic Aviation was acquired by Macquarie in 2004 for ~$238M and sold to KKR in 2021 for ~$4.5B. And now nearing a ~$10B valuation, that’s a ~42x increase over two decades.

English

This is what happens when you combine monopolistic airport land grabs with price-inelastic private jet owners: You get $SKYH's unicorn lease structure: CPI + 4% Floor (Uncapped). Very interesting deep dive on why this is the best lease in real estate:

reddit.com/r/SkyHarbour/c…

English

Mortgage Scores revenue should effectively double from FY '25 to FY '27.

Additional levers to be pulled are share repurchases, software segment growth, price increases in auto and card, as well as increased mortgage volume.

After all customers have converted to the direct licensing model over the next year or 2, I would expect them to begin slowly/gradually increasing mortgage scores again.

English

@ReneSellmann As the new Scores pricing model adoption flows through to the income statement, you will see significant revenue growth for the next year or 2.

That's just for mortgages. They can also hike prices in auto and card segments while the spotlight fades from the mortgage price hikes

English

What kind of growth can you reasonably underwrite for $FICO?

To make sure I don't miss anything crucial, let me walk you through my initial thinking:

✅ 2-3% volume growth

✅ 2-3% per share growth driven by repurchases

✅ 2-4% from operating leverage (mainly on the software side)

✅ 5-10% pricing power (in both segments)

Underwriting the final driver (price hikes; especially in Scores) is the hardest part for me. In fact, I believe management would be wise not to do further price increases in the next few years before then adopting the “Netflix playbook” of consistent, but much smaller price hikes.

FICO's management is guiding for 18% revenue growth in FY26. Is this sustainable?

Given the regulatory headwinds, you absolutely have to think in scenarios here (you always should, fwiw) as the exit multiple could probably be anywhere from the high teens to 40x+.

What are your thoughts @GHadjia?

Rene Sellmann@ReneSellmann

Those familiar with $FICO, what revenue growth are you comfortable underwriting over the next 5 and the next 10 years? What are the key drivers of that growth? I'm predicting that the range of forecasted growth will be WIDE.

English

You're 100% right to be skeptical of a 2021 SPAC miss. Like many SPACs, they experienced early supply chain and scaling delays that pushed their initial timelines way to the right. However, those growing pains have largely been mitigated through intense vertical integration. They are continuously refining their process to speed up construction, reduce costs, and expedite the path to stabilization.

Just look at the economics of their most recent campuses—it’s a completely different story today:

The OPF Phase 2 Arbitrage: They reduced the construction timeline down to about a year and built three hangars for an estimated $40 million. They recently sold a 75% stake in just one of those unfinished hangars for $30.75 million in cash, implying a $41 million valuation for a single hangar.

ADS Phase 2: For example, look at ADS 2. They just started construction a month or two ago and expect it to be completed this December at a heavily compressed cost of ~$250/sqft.

SLC Phase 1: For Salt Lake City they have reduced the construction timeline down to 1 year and construction costs to $285/sqft. Just to put into perspective the pace of improvements that are happening, if you look at the Q3 10-Q, SLC was expected to cost $350/sqft. Through their vertical integration and cost reduction initiatives, by the time they filed their 10-K, that number dropped to $285/sqft.

They have definitely made mistakes in the past, but that is exactly what has allowed this opportunity to arise. The stock was forgotten and left for dead because of the SPAC label, but meanwhile, all of the underlying KPIs are rapidly improving. Vertical integration has minimized bottlenecks, they have secured leases at numerous tier-1 airports with a long pipeline ahead of them, and they just locked in $450 million in debt financing while simultaneously turning cash-flow positive to help fund future construction.

The 2021 SPAC deck was definitely a fairy tale on timing, but the unit economics they are executing on today are very real. I recommend looking at this company without any preconceived notions and we can revisit this discussion. I look forward to hearing your thoughts.

English

@alexbossert @KCapMngmnt You've been bullish on this since the spac. Being this fantastically wrong on the projections disqualifies management entirely. Other spacs were also wrong, yes, and they too have performed poorly.

Anyone buying this deserves to lose their money. Would rather short than long

English

Very interesting new deep-dive on $SKYH over on Reddit.

This post breaks down the hidden FAA arbitrage that legally requires airports to charge Sky Harbour below-market ground rent.

This is one of $SKYH's biggest structural moats, and very few in the market have picked up on it yet.

Link in comments below

English

The 68% pre-tax ROE was an illustration from their latest quarterly presentation. On top of their recent $200 million warehouse facility, they issued subordinated debt to fund the equity portion, meaning they barely have to put up any equity to fund these future projects. This results in a massive increase in their ROE. I highly recommend revisiting this company as the story has changed.

English

@irbezek @alexbossert @KCapMngmnt He is almost certainly affiliated with the company / sponsors in some way. He shills them hard despite obviously suspect forecasts and cartoon tier profitability projections (68% pre tax ROE unit economics)

English

KCM retweetledi

My research has confirmed a portion of the tenant roster for Sky Harbour $SKYH, and it is arguably the most exclusive real estate list in the country. Confirmed tenants utilizing $SKYH private jet hangars include:

Billionaires: Elon Musk, Jeff Bezos, Lane Bess

Cultural Icons: Derek Jeter, Luke Bryan, Rick Ross, DJ Khaled, and the Kardashians!

Corporate Giants: Chevron, Amgen

Rick Ross filmed his "Champagne Moments" and "Shaq & Kobe" music videos right inside his $SKYH hangar, AND this year's Fanatics Super Bowl ad featuring Kendall Jenner was filmed at the Kardashians' Sky Harbour hangar!

English

I'm playing around with screens, preparing a bit for 👇

Was screening for insider purchases at small- and micro-caps and stumbled upon GEE Group $JOB.

Never heard of it, but quite the sizable insider purchases very recently + very strong net cash balance sheet + profitable it seems.

Anyone familiar with this one?

ToffCap@ToffCap

We’re thinking about adding a few Bloomberg screens to the TMM. Think top insider purchases or stock screens based on certain criteria, etc. Would cost us very little effort, but might be interesting to share. Would this be useful? What would you like to see?

English

What else? I essentially look for 10% cash and buying back shares at cheap multiples or growth with high incremental margins at reasonable multiples.

I'll add more to the above thread that I like.

English

Japanese stocks are starting to look juicy. It's time to buy. Finally, something to deploy some cash into.

I like:

Asiro $7378 - Legal networking (Japan's LinkedIn for lawyers..rapid growth and rapidly increasing margins, huge incremental margins).

English

It looks like we now have a place/community to discuss all things Sky Harbour ! $SKYH

r/SkyHarbour

reddit.com/r/SkyHarbour/

English

KCM retweetledi

🧐Sky Harbour $SKYH – Initial Equity Research

✈️Aviation infrastructure company building the first nationwide network of private hangar campuses in the 🇺🇸

✅Early-stage company reaching breakeven while aggressively expanding its leasable hangar footprint

🎯In recent weeks, it has secured financing to build its next wave of campuses — without shareholder dilution — while the shares have traded near 18-month lows.

💎Today, we present our in-depth research, where we cover:

• A detailed breakdown of the business model and what makes it structurally different from anything publicly traded today

• The structural demand thesis: is the hangar shortage real, durable, and large enough to support the ambitions of this company?

• An honest assessment of the moat: what genuinely protects this business, and where the defences are thinner than the narrative suggests

• A full map of the campus portfolio: what is operational, what is under construction, and what the pipeline actually implies for revenues through 2030

• The financing structure in detail: how the company is funding $350M+ in construction, what it costs, and what the real risks inside that capital stack are

• The unit economics of a stabilised campus, using figures disclosed directly by management - and what they imply for the return profile at scale

• A bottom-up valuation of the 2030 portfolio using a NOI and cap rate framework, with a full sensitivity analysis

• The key risks and things to monitor

•Our honest opinion about Sky Harbour

English

KCM retweetledi

Important data point from the most recent sell side report from BTIG on Sky Harbour $SKYH:

"Construction Has Ramped (and Costs are Down). SKYH's efforts to decrease development timelines and reduce construction budgets appear to be paying off. While a small sample size, management noted that the three sites under active construction are all on time and on budget, a stark contrast to the company's previous projects (DVT I, ADS I, and APA I). Management noted that recent guaranteed maximum price (GMP) contracts on active projects have averaged ~$253/SF (vs. ~$390/SF for the three most

recent completions), and there are still opportunities for further efficiencies in the future. Improving costs and development timelines will be critical for the company's plans to start 7-8 new development phases per year, which equates to ~$250M of annual capex spend."

English

@kylehtucker Hangars for business aircraft are another supply-constrained asset pool, which is why I’m invested in Sky Harbour $SKYH

English

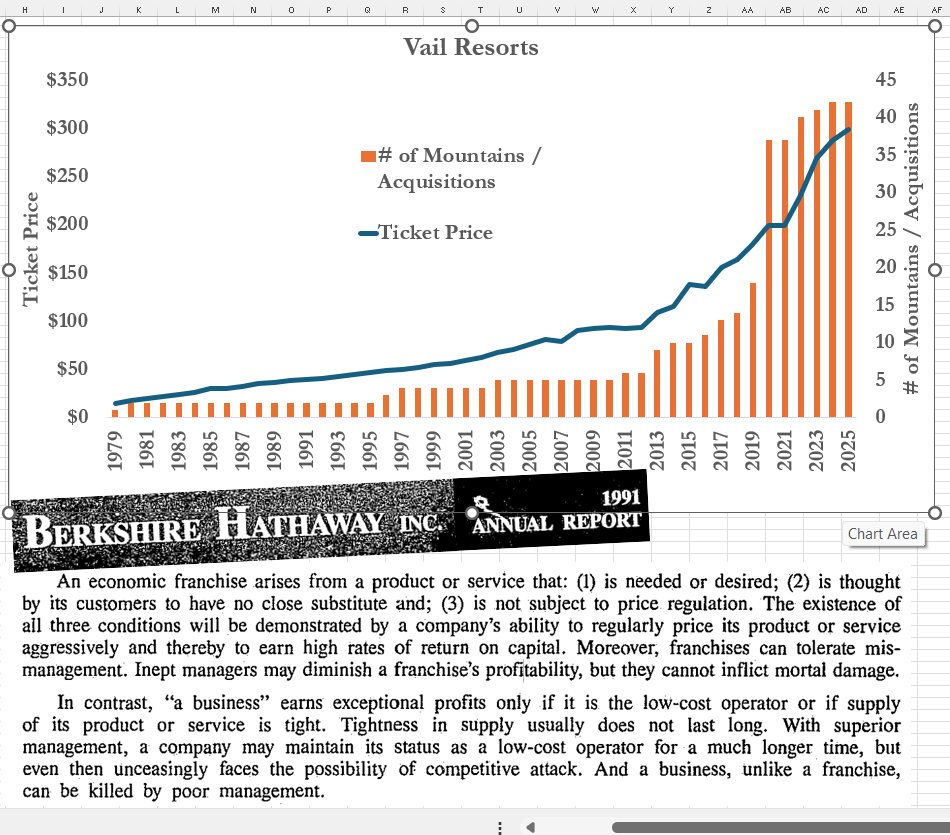

never understood how Vail (10x bagger ski mountain rollup) had like $1 billion of EBITDA (probably half that in fcf), but always been a big out-side fan

so when annie said ski passes are like $250/kid, my reaction was something like ‘𝘤𝘰𝘰𝘭, 𝘧𝘦𝘦𝘭𝘴 𝘭𝘪𝘵𝘵𝘭𝘦 𝘳𝘪𝘤𝘩 𝘣𝘶𝘵 𝘨𝘶𝘦𝘴𝘴 𝘳𝘦𝘢𝘴𝘰𝘯𝘢𝘣𝘭𝘦 𝘧𝘰𝘳 𝘭𝘪𝘬𝘦 𝘢 𝘸𝘦𝘦𝘬 𝘰𝘧 𝘴𝘬𝘪𝘪𝘯𝘨’

I missed the ‘per day’ piece!! 🥴

(this sounds like we live under a rock (we actually live 𝘰𝘯 𝘢 𝘳𝘰𝘤𝘬) but I’m not used to buying ski passes)

anyway I pulled this chart together quickly on pricing vs acquisitions

gotta love supply constrained asset pools. We’ve looked at small potatoes things (e.g. marinas and billboards, other things w nimby / moratoriums etc.) but typically struggle w pricing / unlevered yields

But I always think of the Balmer interview when he was asked why he paid a then record breaking $2bn for the clippers and he said ‘𝘸𝘦𝘭𝘭 𝘪𝘵’𝘴 𝘬𝘪𝘯𝘥 𝘰𝘧 𝘭𝘪𝘬𝘦 𝘵𝘩𝘪𝘴. 𝘛𝘩𝘦𝘳𝘦’𝘴 𝘰𝘯𝘭𝘺 𝘴𝘰 𝘮𝘶𝘤𝘩 𝘣𝘦𝘢𝘤𝘩 𝘧𝘳𝘰𝘯𝘵 𝘱𝘳𝘰𝘱𝘦𝘳𝘵𝘺 𝘩𝘦𝘳𝘦. 𝘈𝘯𝘥 𝘐 𝘸𝘢𝘯𝘵𝘦𝘥 𝘮𝘦 𝘴𝘰𝘮𝘦’ (as usual wildly paraphrasing)

--

pls subscribe to my newsletter in comments / in my profile. and pls send us any $2m+ EBIT deals!

English

KCM retweetledi

The next 2 years will be eventful for Sky Harbour $SKYH. Here’s the current development pipeline for new hangar campuses/phases expected to open:

2026 Openings

• OPF (Miami) Phase II → Q2 2026 (3 hangars, ~112k sq ft)

• BDL (Hartford) Phase I → Q4 2026 (3 hangars, ~107k sq ft)

2027 Openings

• ADS (Dallas) Phase II → Q1 2027 (4 hangars, ~108k sq ft)

• SLC (Salt Lake City) Phase I → Q1 2027 (4 hangars, ~172k sq ft)

• DVT (Phoenix) Phase II → Q2 2027 (6 hangars, ~133k sq ft)

• ORL (Orlando) Phase I → Q2 2027 (3 hangars, ~134k sq ft)

• IAD (Dulles) Phase I → Q3 2027 (4 hangars, ~172k sq ft)

• POU (Hudson Valley) Phase I → Q3 2027 (2 hangars, ~86k sq ft)

• PWK (Chicago) Phase I → Q3 2027 (4 hangars, ~172k sq ft)

• HIO (Portland) Phase I → Q4 2027 (3 hangars, ~107k sq ft)

Total expected new capacity (2026–2027):

10 phases • 36+ hangars • ~1.3 million rentable sq ft

All figures from Sky Harbour’s Q3 2025 10-Q.

English

KCM retweetledi

Sky Harbour $SKYH just locked down $450M in capital ($150M in Series 2026 Bonds and the $300M JPM facility) at a weighted all-in rate of 5.15%. Once deployed at a ~13%+ yield, that generates $59M in annual NOI. At a conservative 6% cap, that’s $975M in value. Subtract the debt, and you’ve got $525M in value creation—roughly $6+ per share. The market’s reaction? Dead silence. It’s wild.

English

$STRR issues statement on $JOB. $JOB wants to be a buyer, but it should be a seller.

globenewswire.com/news-release/2…

English