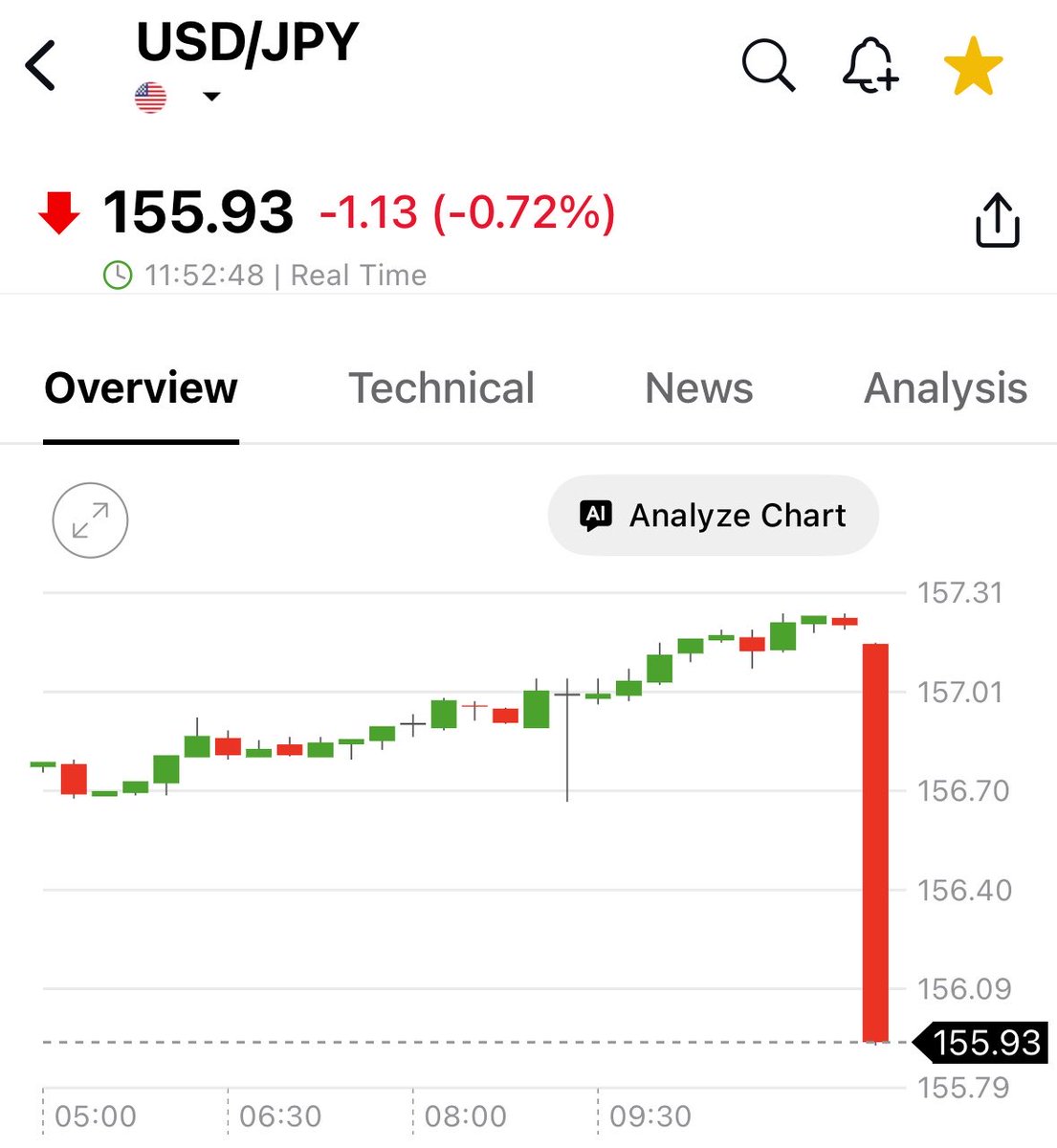

@anytimeFXmetal Could you please explain it why SPX would not go down if USDJPY above 159.2? I am not well versed with the macro and FX so trying to understand.Thanks.

English

BioAndTrade

2K posts

@Kapstahoon

Do your own DD. Not a financial advisor. Biotech , Tech, EV and growth, trading

According to my calculations, with an oil price stable above 90$ $OXY P/E drops to ~5.5 from the current ~40 at the current price. Won't be personally shocked to see $OXY pull off a 3x or even 4x in a few months if the current situation shifts from temporary to long-lasting

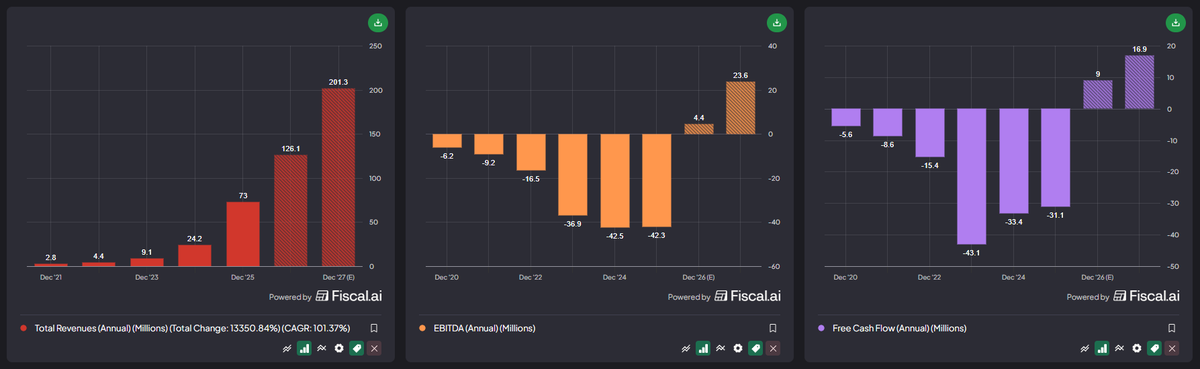

$AAOI reports earnings tomorrow and this is what I'm expecting. 2025 revenue was $456M. Management guided $1B+ for 2026 with $120M+ in non-GAAP operating profit. The business is set to more than double in a single year after running $190-250M annually from 2019 through 2024. > Q1 guide is $150-165M vs Street at $157M. CATV running hot, 800G firmware slip from Q4 pushed shipments into Q1, and they beat EPS by 91% last print. Setup favors a beat. > Q2 is what matters. Management has telegraphed it as the first profitable quarter and the start of the 800G/1.6T ramp. Above $185M with positive NG EPS and the move continues. > OFC capacity slide showed 650K combined 800G + 1.6T units/month by Q4 26, 30% above prior guidance. 930K/month by Q4 27. That's a ~$6B annualized run rate from two product lines against a $14B market cap. Full pre-earnings breakdown linked below. $AAOI $LITE $COHR $AEHR $VIAV

JustDarioCigarTime - Episode 75 ⚠️ WHILE THE OIL SHOCK WORSENS, THE FUTURE OF GOLD AND SILVER BECOMES BRIGHTER 🎙️ - Spirit Airlines - The Oil Supply Shock Impact On Companies Cash Flows - Japan FX intervention signals relentless money printing ahead youtu.be/gON5hirCbiQ?si…

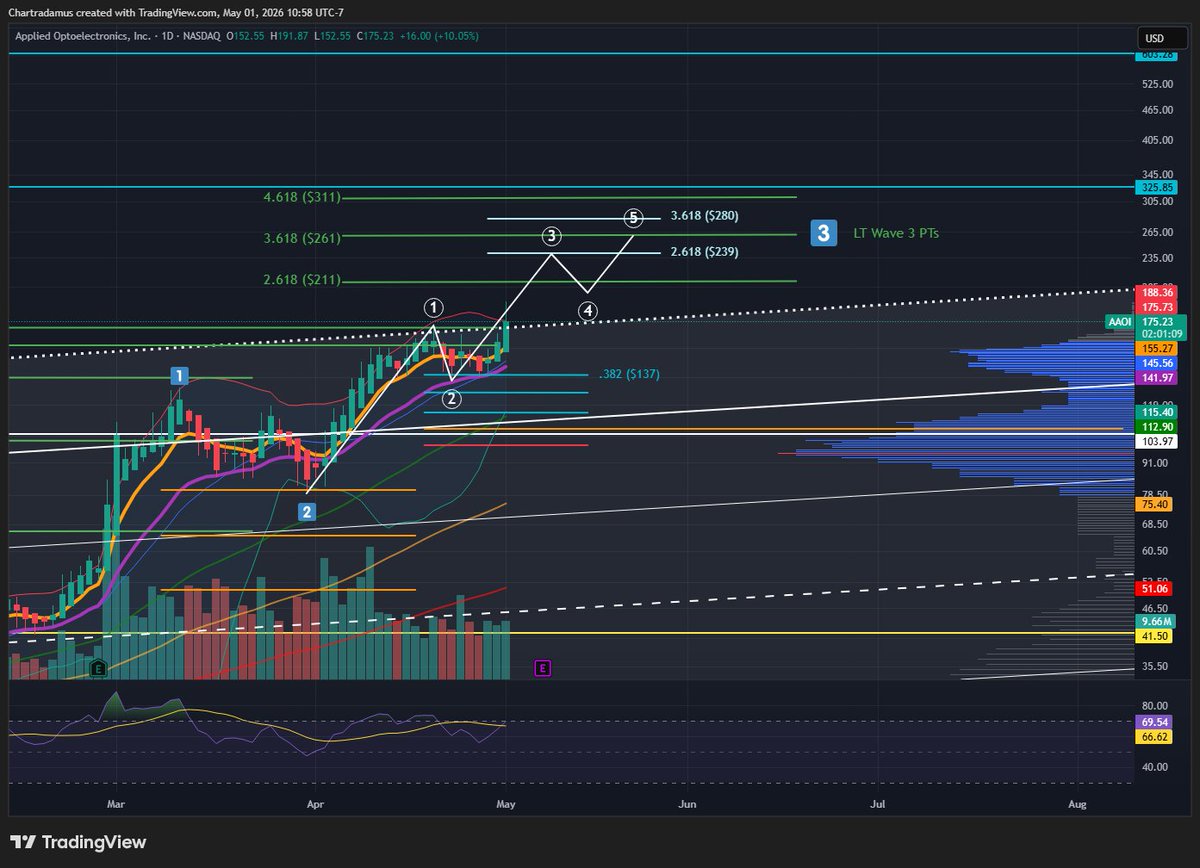

$AAOI Primary Wave 3 PT = $240 🟢 Base Case Very sly. As discussed prior, there was a chance for this leg lower to convert into a higher low via Primary Wave 2 of LT Wave 3. After tagging consolidative support alongside the .382 Fib ($137) of PW2, the minimal level of retracement for a higher low, the stock has soared higher today. In order to validate this bullish scenario, it must decisively break $170s and squeeze higher to the Primary Wave 3 PT of $240+ on route to completing LTW3. PW4 and PW5 cannot be determined until PW3 ends. Let us see whether it can validate this path forward.

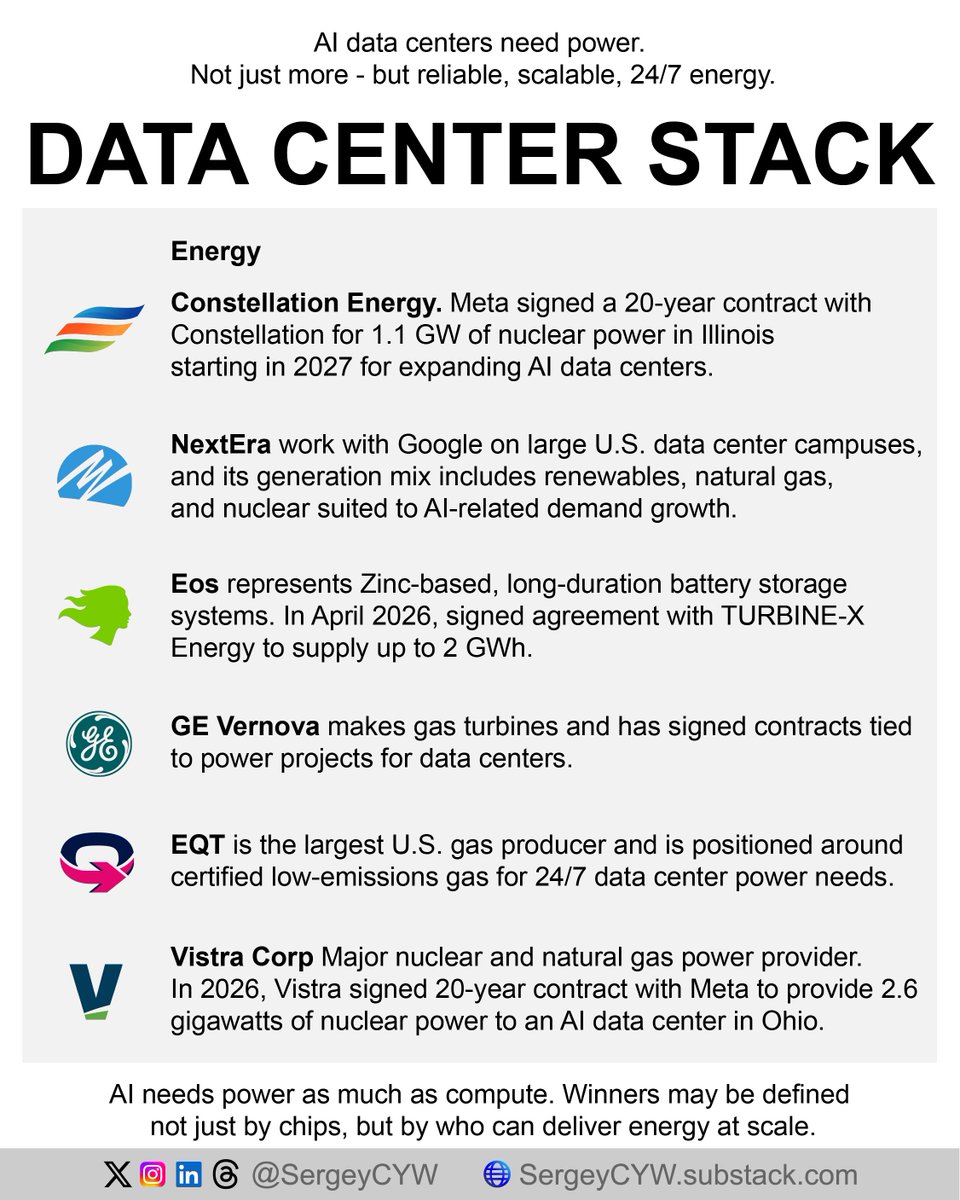

BREAKING: Half of planned US data center builds have been delayed or canceled