Sabitlenmiş Tweet

Krevix

3.9K posts

Krevix

@KrevixD

Investment Analyst | σ γ | 📚Formación y tesis: @clubdelvalue

Madrid Katılım Ağustos 2022

711 Takip Edilen4.4K Takipçiler

Krevix retweetledi

Comentario del primer trimestre de Sigma Internacional & Gamma Global

Entramos en detalle en el comportamiento de la renta fija de Gamma Global comparada con la renta fija tradicional, la renta fija High Yield y la deuda privada

youtu.be/SUQ9LkUjh1E?si…

YouTube

Español

Krevix retweetledi

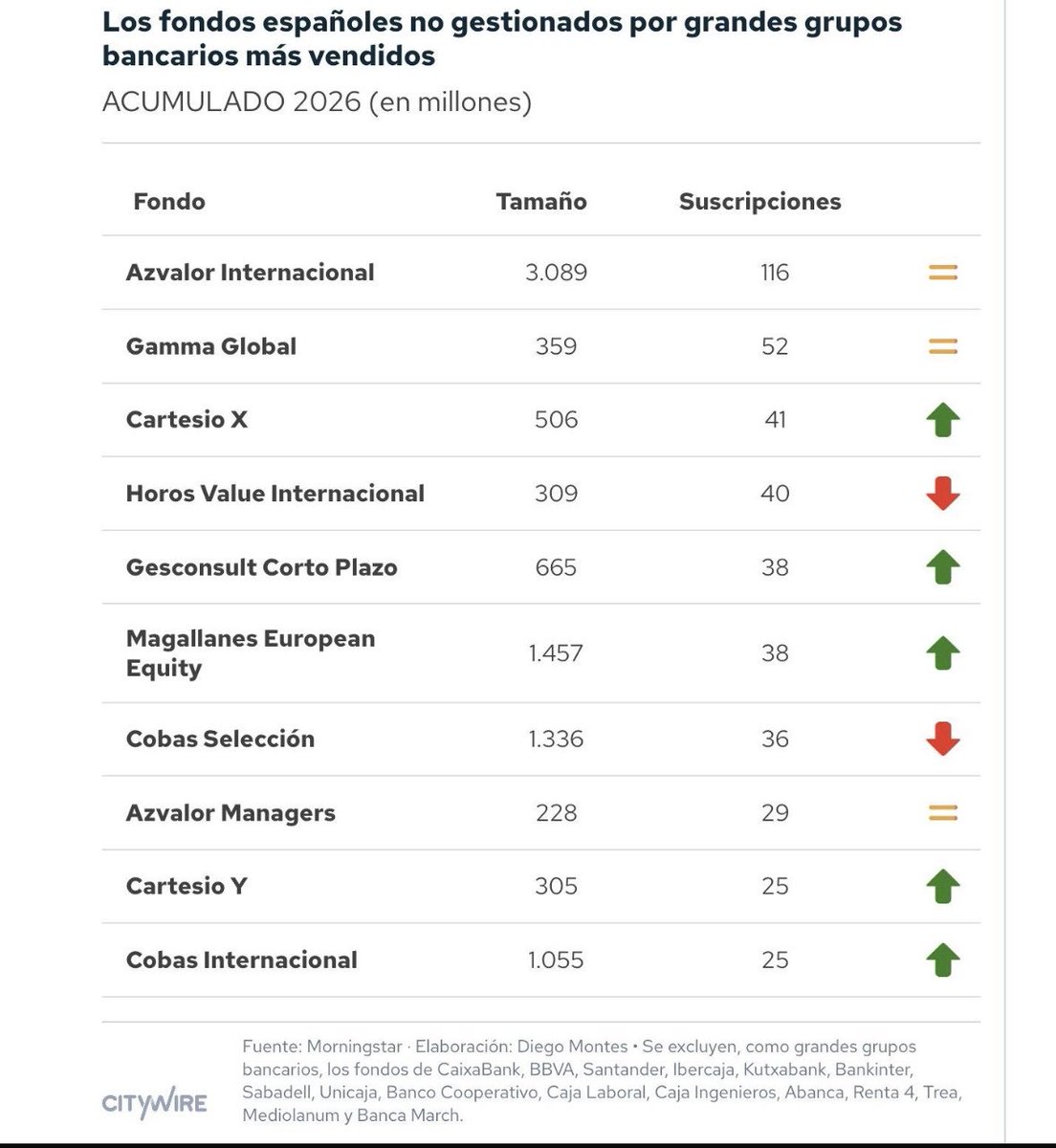

Según citywire, Gamma Global es el segundo fondo con mayores entradas en el año excluyendo a los fondos de los grandes grupos financieros.

Lo mejor? Seguimos manteniendo una cartera de renta fija en linea con los últimos 5 años en cuanto a duración, calidad y rentabilidad esperada.

Por último, quiero señalar que ayer sale en algunas plataformas que Sigma Internacional cayó un 3%. Esto es incorrecto, ya que subimos un 0.45%. Hubo un error en la comunicación y plataformas como Bloomberg si que lo corrigieron, pero algunas otras como Morningstar no llegaron a tiempo y se ajustará hoy.

Muchas gracias por la confianza!

Español

@MM_SdT @MrtnzAlvrz La exposición de Hamco a memorias en Corea es 0. A pesar de ser un +50% del índice las dos empresas (Samsung y Sk Hynix)

Español

@MrtnzAlvrz Cuánto te está apoquinando HAMCO por hacer toda esta publi de Corea? Confiesa

Español

@UserM1HA @MrtnzAlvrz President Trump says “I think the war is very complete, pretty much.”

English

@MrtnzAlvrz Pero ¿que noticia ha habido para que el mercado no impute una subida ? Quizás las reservas están mayoritariamente llenas y por eso no hay mucha gente comprando o se han metido reservas estratégicas? Solo escuche de Japón la verdad

Español

Krevix retweetledi

There are decades where nothing happens; and there are weeks where decades happen

Thomas van Linge@ThomasVLinge

Cuba 🇨🇺 BREAKING: nighttime protests have erupted in the capital Havana. After more then 60 hours without any electricity people have had enough. Protests against thr communist regime are now being reported in several neighborhoods across the capital.

English

Krevix retweetledi

BREAKING: Qatar's energy minister warns oil prices could rise to $150 within two weeks

English

Krevix retweetledi

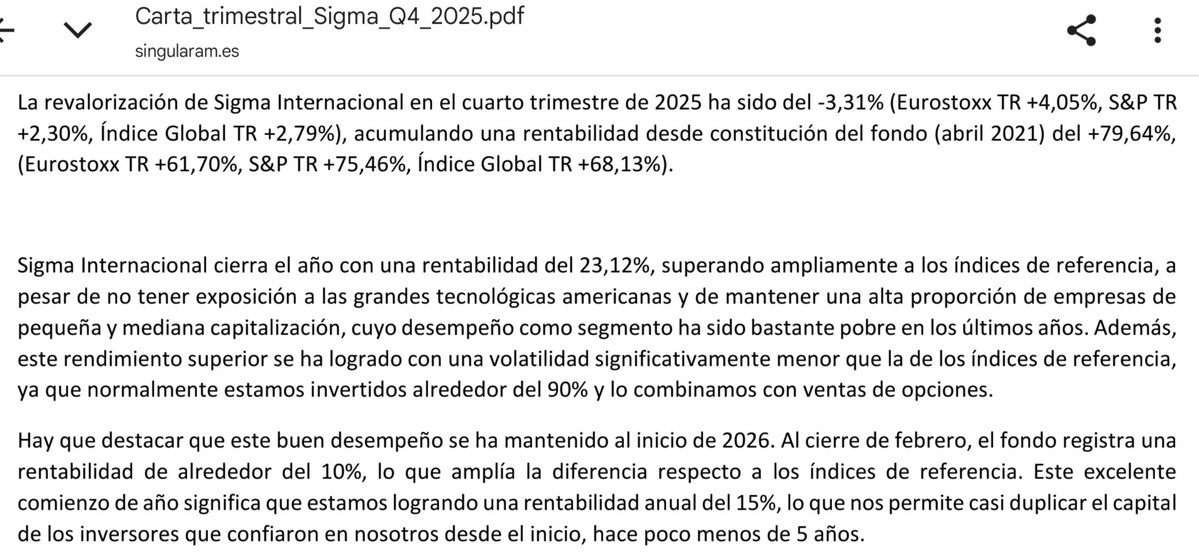

📈 Tras 5 años de trackrecord y superando en ese periodo a S&P 500 y MSCI World, podemos decir que Sigma Internacional (@gabcasla) ha dejado de ser una promesa para ser una realidad.

Su desempeño invirtiendo fuera de lo mainstream ha obtenido un 15% anualizado. Enhorabuena!!!

Gabriel Castro, CFA@gabcasla

Carta del cuarto trimestre de Sigma Internacional. Repasamos la filosofía del fondo y el método que nos ha llevado a duplicar el capital en menos de 5 años singularam.es/wp-content/upl…

Español

Krevix retweetledi

BREAKING:

Trump stated that the U.S. is cutting off trade with Spain over the decision by Sánchez’s far-left government to ban the use of Spanish military bases for strikes on Iran.

"So we're going to cut off all trade with Spain. We don't want anything to do with Spain."

🇪🇸🇺🇸

English

Krevix retweetledi

$KOS Kosmos reported excellent results yesterday. Although the stock didn't continue climbing, I believe this is mainly due to investors taking profits rather than concerns about earnings—unless I underestimate the market's intelligence. Since KOS has already gained 2.7 times its value in just about two months, it’s normal for some investors to want to lock in gains. However, I maintain that the company's fundamentals are significantly stronger than its current trading price suggests.

Initially, focus on algorithms; earnings might appear as a miss and there's small cash burn, but a deeper look reveals a beat. One cargo from Jubilee was shifted into early 2026, resulting in production of about 67,9 Kboepd, while sales were only 62,9 Kboepd. This is expected to normalize in Q1 and is just a timing issue. When modeling production instead of sales, earnings and cash flow look strong. However, our main focus should be the 2026 guidance, as the company is making a complete turnaround thanks to GTA and Jubilee.

In production, the company forecasted a strong Q1 at 73 Kboepd, at mid-range estimate. Recent updates show that the fields that caused issues last year are now performing very well (Jubilee and GTA), surpassing consensus expectations. GoA is alright, but significant activity is expected this year on Tiberius and the strategic alliance with Shell, likely leading to a notable increase in production over the coming years. While Q4 and the outlook for Equatorial Guinea are somewhat underwhelming, that situation has changed since the assets were sold to Panoro. Be aware that the company will continue consolidating Q1 and Q2 results, but in reality, Panoro will be the one that collects profits/losses since January 1st.

One key point to highlight is that Senegal is set to begin constructing its domestic gas pipeline network next quarter. This is crucial for two reasons. First, it boosts production with minimal capex and no opex, significantly lowering the breakeven and making the asset highly free cash flow positive even at tough Brent prices. Second, it initiates a scheduled repayment timeline for Senegal and Mauritania. KOS provided a $400 million loan to develop the GTA, a figure that is not reflected in most models. Management plans to monetize part of this when the schedule becomes clearer, possibly at a small discount, thereby generating additional cash to further reduce debt.

The auditor loudly affirmed my previous statements. 1P reserves cover 10 years of production, while 2P reserves last 20 years. Excluding EG, reserve replacement exceeds 100%, and concerns about the status of Jubilee/TEN reserves should be disregarded.

Furthermore, as I have been asserting, the banks (RBL) provided the company with a covenant waiver to account for lower oil prices and the initial costs of the GTA under the company's net debt/EBITDA covenant. All rating agencies and analysts were very concerned about this, but I remained quite confident based on the relationship's historical performance. Indeed, Kosmos is preparing to initiate discussions to extend the Reserve Based Lending (RBL), meaning the bank loan.

The most crucial aspect is opex and cash flow breakeven. Opex per barrel has been decreasing over recent quarters, from $36.5 in Q2 to $26.8 in Q3 and $26 in Q4. As expected, we will see a substantial reduction in the next quarter and into next year. The company forecasts $19 per barrel for Q1 and $21 for the full year, but these figures include TEN and EG assets, which have the highest operating costs. Since they are acquiring the TEN FPSO and divesting EG, the opex per barrel will drop further, enhancing the company's resilience to lower oil prices. Capex and G&A expenses are projected to be low, encouraging analysts to significantly upgrade free cash flow estimates, given lower breakeven and higher oil prices. Additionally, the company is capitalizing on the current environment by hedging some production at favorable prices. I’m still surprised that I have a notably different FCF figure compared to most of them. They were assuming a $65 breakeven and $60 Brent prices, which led to a substantial FCF burn. It’s never too late to adapt, guys!

Overall, the results are positive and continue the strong momentum the business has shown this year. Given the current oil outlook, operational performance, and a fixed balance sheet, I still believe the stock is significantly undervalued at its current price. But please do your own due diligence!

PS. I saw yesterday that someone sent me a DM some time ago asking if I attended the Jubilee expert call that JPM organized. I don’t know how I deleted all the DMs… It’s crazy how many bots we have on X nowadays… it’s a shame. Well, I couldn’t read the message, so please reach out again here or on LinkedIn. Anyway, I want to share my thoughts. I was expecting more from this call, but it was enough for the JPM analyst to realize that all their estimates were wrong, as their main base case assumes that banks will panic and force Kosmos to raise capital or liquidate. These experts guys proved that the banks are overcollateralized (as the management confirmed yesterday) because the value of Jubilee alone is much higher than the amount they lent, even in mediocre scenarios.

English

Krevix retweetledi

Krevix retweetledi

Heading to the kitchen to make a coffee so I can monitor the situation

English

Krevix retweetledi

El que le parecio barato el apartamento en Abu Dhabi mirando esto.

WarMonitor🇺🇦🇬🇧@WarMonitor3

Video of aftermath of Iranian missile attacks on Abu Dhabi.

Español

Krevix retweetledi

suicide bombing in an age where drones exist, pure love for the game, you have to respect this dedication

Eyal Yakoby@EYakoby

BREAKING: Afghanistan announces they will use suicide bomber battalions.

English

Krevix retweetledi

$KOS Big news!

Panoro Energy is purchasing the Kosmos Equatorial Guinea asset (40.375% stake in Block G) for $180 million, with potential earnouts of $39.5 million tied to Brent prices and production levels over the next three years.

I believe this is a significant win for both companies. Please note that I am involved in the bond amendments, tap issue (bond) and the equity raise.

On one side, Panoro Energy is acquiring a great asset at an excellent price. Panoro is boosting its pro forma production by 85% and its 2P reserves by 110%. Be aware that Panoro does not incur additional overhead costs, as it already owns 14.25% of the asset. To accomplish this, the company is raising $150 million via a tap issue and a minor capital raise, resulting in only about 10% dilution at current prices (no discount required!), which shows strong support from major shareholders.

On the other side, Kosmos is raising liquidity from a non-core asset that has little effect on production or free cash flow going forward. Simultaneously, it is countering the bearish argument that the company cannot manage the maturities coming in the next 24 months and that it is highly dependent on oil prices, which would inevitably require a significant capital raise. They proved to be wrong! Rating agencies and research analysts should promptly update their ratings based on this deal and the most recent production update.

I estimate that this asset is worth approximately $300 million with some optionality, while Panoro is purchasing it for $180 million plus potential earnouts. Keep in mind that these earnouts depend on Brent prices and production levels exceeding my valuation estimates, so if Panoro pays an additional $39.5 million, the asset's fair value will increase substantially. This transaction is a significant win for Panoro, as the difference between the fair value and the purchase price is considerable, given the market cap ($270 million) and the Enterprise Value ($377 million). It also lowers the cash breakeven and notably enhances the company's capacity to pay dividends and buybacks in the future. However, for Kosmos, this is less impactful on valuation, since their market cap exceeds $1 billion and their EV is around $4 billion. For Kosmos, raising liquidity is more beneficial, as it demonstrates to the market that the company is significantly more resilient than the current price indicates. Additionally, Kosmos could repurchase some debt at a significant discount, creating far more value than what was left in this deal.

I think Kosmos still has some ways to raise liquidity this year, such as monetizing the $400m receivable from Senegal/Mauritania and receiving McDermott litigation proceeds. However, although I believe these are very likely given the proceeds from this deal, the current Brent price, and production levels, I think the company doesn’t need them to fix the balance sheet and trade at much higher levels.

I think both companies will trade up, including Kosmos bonds.

As I mentioned, we hold Panoro bonds and equity, as well as Kosmos bonds and equity; please do your own due diligence.

English

Krevix retweetledi

Krevix retweetledi

Seré breve. Se han abierto dos situaciones especiales (odd lots) que permiten obtener muy buenos retornos en el plazo de un par de semanas con muy poco riesgo.

¿Es este nuestro estilo?

Honestamente, no. Nuestro enfoque es el análisis de tesis serias y el valor a largo plazo. Este tipo de oportunidades son fáciles de encontrar si sabes dónde mirar, y no basamos nuestra estrategia en ellas, ni nos gusta comerciar con ellas.

Sin embargo, hay un dato objetivo que no podemos ignorar: desde que abrimos el Club, la rentabilidad acumulada de estas operaciones ha superado con creces el coste de la suscripción.

Como diría aquel gestor value: “Te llevas la financiera gratis”.

Español

Krevix retweetledi

“why didn’t you buy bitcoin in 2012”

me in 2012:

English

Krevix retweetledi

Losing half your portfolio in 6 months from SaaS re-rating from 12x sales down to 5x and you stumble on some old BRK letters where you are introduced to this funky new idea called book value

English