LD

128 posts

@acook986786 @StockSavvyShay They have funding. No need to raise additional cash at this point.

English

@StockSavvyShay Now the only question is, will this be followed by a dilution announcement? Makes sense into the hype

English

$ASTS is backing a U.S. carrier satellite-connectivity venture with $T, $TMUS & $VZ to help close mobile coverage gaps nationwide.

The goal is direct-to-smartphone satellite service without extra hardware with AST positioning itself as a key space-based connectivity layer.

Futurum Equities@FuturumEquities

Full breakdown on the print, the reaffirmed 45-satellite target, and the 99 Mbps demo from orbit to an unmodified phone. youtu.be/Ab4qO0O5imE 🎙️

English

@StockSavvyShay How does this compare to Starlink's partnership with T-Mobile that already exists?

English

@StockSavvyShay Is this positive for ASTS? It sounds like providers are planning to have their own joint venture.

English

@Gosleepriya 81151. Break 0 and make 11. Turn upside down and place two sticks at the end.

English

@mo32564305 One of my worst decisions to buy this as value play. It is going to zero.

English

$TTD at $24.17 — earnings tomorrow after close. Here's my take...

The asymmetric upside is real, but so is the structural threat people are underpricing.

Amazon is the actual killer here. Not Publicis. Amazon DSP charges agencies ~1% vs TTD's ~20% take rate, uses first-party retail shopper data that no neutral DSP can replicate, and is aggressively subsidizing head-to-head platform trials. Omnicom — which holds Amazon's US media account — reportedly shifted a double-digit percentage of Q3 programmatic budget from TTD to Amazon DSP. That pattern, if it spreads to WPP and Dentsu, is not recoverable with a product update.

Jeff Green has dismissed Amazon as a real competitor on multiple earnings calls. Wall Street didn't find it convincing. That fumble is as much of the stock story as the Publicis dispute.

The bull case: TTD still dominates the open internet, CTV is structurally growing, the 2026 World Cup and political cycle are real tailwinds, and Green just put $148M of his own money in near these levels. Revenue is $2.9B at 78% gross margins. The bar tomorrow is just 10% growth.

The bear case: a ~20% take rate in a world where Amazon charges 1% is not a sustainable moat. It's a business model that works until agencies have a credible alternative — and now they do.

Tomorrow answers the near-term question. The structural one takes longer.

Not investment advice, good luck longs.

English

$MELI Q1 EARNINGS

• Revenue $8.85B vs Est. $8.37B

• Net Income $417M vs Est. $426M

•TPV $87B vs Est. $80B

• GMV $19B vs Est. $18B

Free shipping and credit expansion squeezed margins.

English

Max Space is developing an inflatable space station called Thunderbird.

It will launch on a Falcon 9 and expand in orbit to create a larger living and working area.

Designed for four astronauts, it aims to offer more space and comfort, with a planned launch around 2029.

English

$ASTS Calling it. By Monday we see AST Spacemobile crates on the back of semi's headed to the Cape.....It's time.

English

I’m 58. My wife and I are both financial analysts at JPMorgan.

I’ll only say this once.

The fastest way to make $10,000,000 by 2026:

$NVDA (NVIDIA) — Strong Buy

$AVGO (Broadcom) — Strong Buy

$ASML (ASML Holding) — Buy

$TSM (Taiwan Semiconductor) — Buy

$AMAT (Applied Materials) — Buy

$AMD (Advanced Micro Devices) — Buy

$ANET (Arista Networks) — Buy

$MU (Micron Technology) — Buy

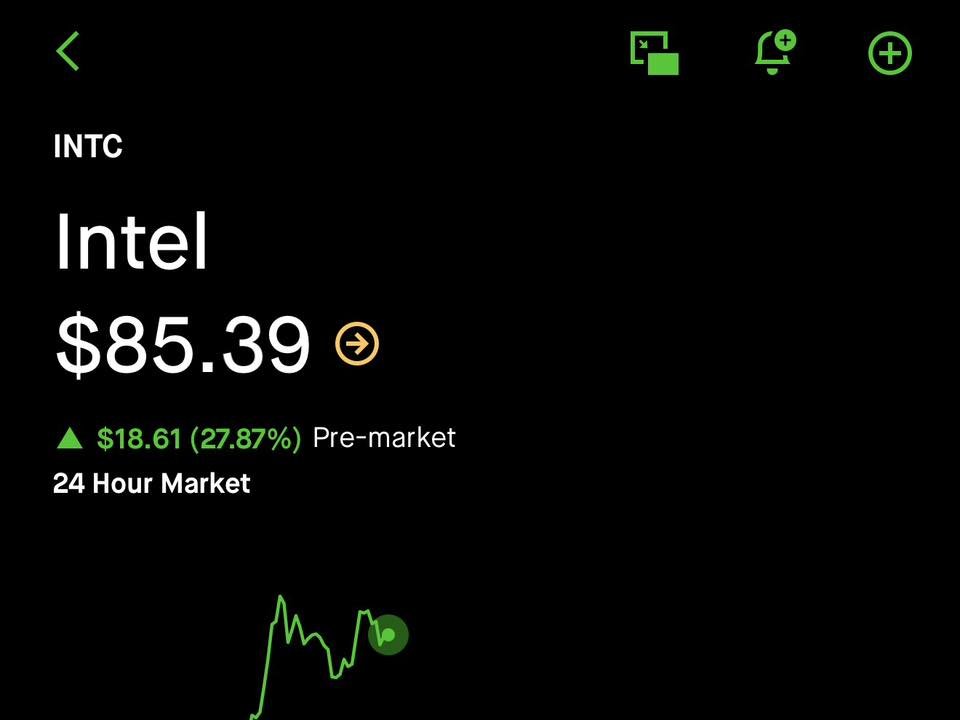

$INTC (Intel) — Avoid

People ask, “Why don’t you charge?”

I’ve already done well. I share because I enjoy it.

English

$RKLB Not only it was a great successful launch 🚀. This mission was a shareride mission. They deployed 8 satellites in the correct orbit. Yes that was eight and photon kept moving around to deploy the satellites exactly where they needed to be. Just Amazing.

English