@MisterMCAP “Opportunity Pipeline” it’s not a given. Still impressive though

English

GlA

75 posts

Have you ever seen a company grow this fast and trade this cheap? Micron is projecting +219% YoY growth next quarter. Forward Multiple: 4.6x $MU

I’m the ghost trader of @aleabitoreddit. First she picked up my $SOI Soitec idea, now $SIVE too. Great that my followers could enter much cheaper, but she hasn’t reacted to a single one of my posts. Pretty pathetic. x.com/felixschreibe1…

$MU I worked 21 years as an HBM, DRAM & NAND engineer. AMA is open. Ask me anything. I'll drop rare insights where I can.

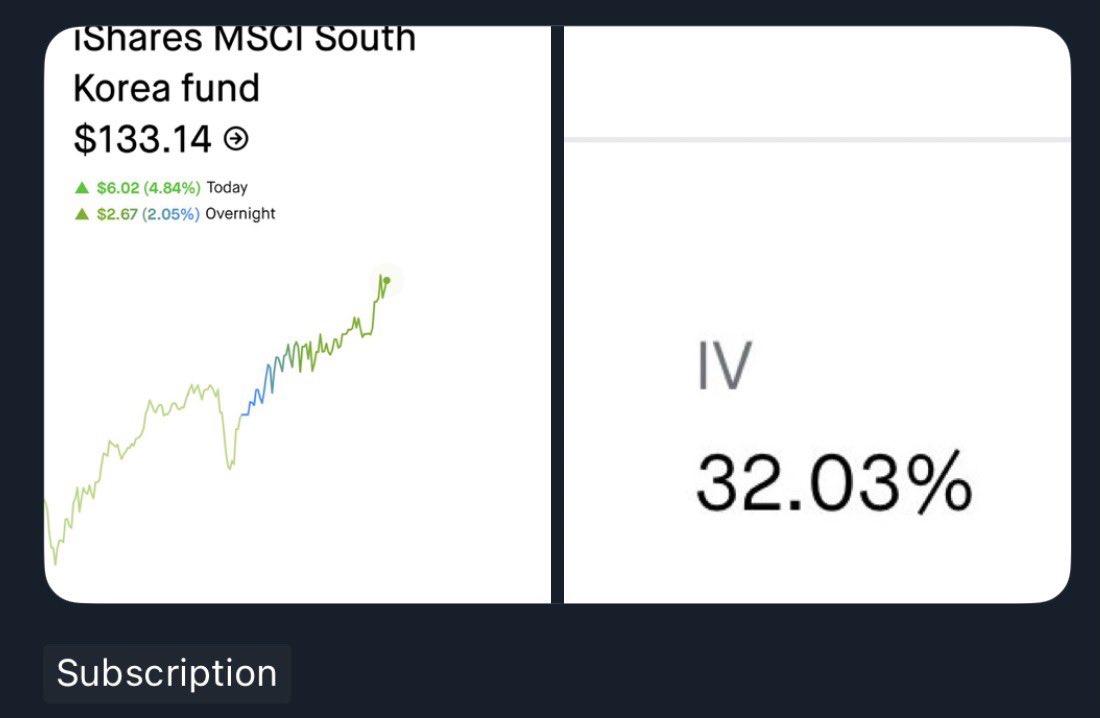

Trade idea that I published to my shower thoughts channel: Korean Index volatility arbitrage and taking advantage of Black-Scholes models. $EWY long options seem mispriced. This is Blackrock's Korea Index, which is majority memory (Samsung Electronics, Sk Hynix). The stock swings 2-5+% a day, and is up 136.25% 1Y, despite priced like a normal index IV. Samsung is volatile. SK Hynix is volatile (eg. 65% - 80% est). But the combination of the two through the index is priced way less than both low beta $GOOGL (37.33%) and $AMZN (39.12%) at ~32% IV. I've been watching $EWY for a bit and it does look volatile. As for pricing my guess is MMs priced in IV based on historical averages (5-10 years), where the Korean index was completely flat. And were expecting calls 2 years out to revert to the mean. But this volatility should be the new norm as markets price in the new memory supercycle (eg. $TSM went from 30% IV to 46.2% IV). Long calls should benefit from both Samsung + Sk Hynix carrying the index. And the main benefit is vega expansion that you won't get from $KORU. You also can't get this option MM pinning like individual US stocks since this is Korea's national index and long term. TLDR: Individual components SK Hynix + Samsung are highly volatile. They're basically half of the index, but options in index are priced with low volatility, perhaps due to historical 5-10 year data. Long calls benefit from vega expansion that weren't priced in correctly as MM forward vol estimates are anchored too heavily on historical realized vol, which was low for $EWY over the past 5-10 years

Was the first to talk about $AXTI in relation to photonics BOM/supply chains: $IQE is very interesting too as one of the only Western suppliers. Basically if you look at photonics flow on $GOOGL TPU/hyperscaler ASICs kinda looks like this (very likely, but undisclosed): Optical Transceivers (highest BOM): Lumentum/Cloud Light: ~ Vital / $AXTI-> $AXTI/Sumitomo/JX -> $IQE (Epi-Wafers) -> $LITE / Cloud Light -> $FN (Contract Manufacturing) -> $GOOGL TPU Merhcant optical supply chain: ~ Vital / $AXTI -> $AXTI / Sumitomo / JX -> → $LITE / $AVGO / $COHR (EML) + $MRVL / $MTSI / Semtech -> Innolight/Eoptolink -> $GOOGL So if you want moonshot-type photonics BOM / price-hikes stocks deeper upstream in the photonics BOM: $AXTI, $IQE and your way to go. $AXTI had terrible fundamentals before but the recent Northland fundraising round cemented its run. $IQE has terrible fundamentals now (Net debt £23.5 million) but is probably one of the most critical parts of the supply chain. If they manage to sell their Taiwan operations, wouldn't be surprised if it went up quite a bit just from their inp business. There's £18m convertible notes (which is basically nothing), then there's 120 to 154m new shares (~12% to 15%), which is also kinda nothing relative to current size. On the other hand, others $LITE and Innolight are probably more established. TLDR: $IQE -> seems critical to Western supply chains, $130MC. Net debt, if they sell Taiwan business -> strong re-rating or they might just dilute you anyway. But if the Taiwan business fails to be sold, probably expect to be diluted to oblivion like Wolfspeed. So huge, huge, risk ad do you own research into risks. But $AXTI and $IQE might are personally interesting to me (I do own $IQE).