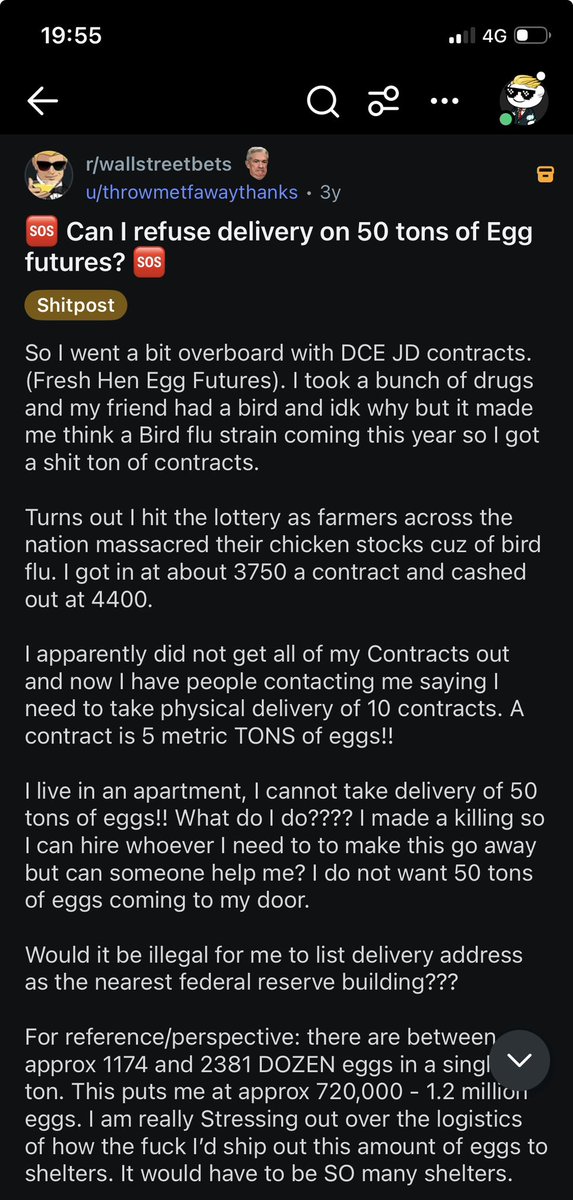

Sabitlenmiş Tweet

Saint

9.7K posts

Last week Thursday we placed an order at a local supplier, invoice was issued and we wired funds, today morning, we went to load trucks, they tell us price has gone up by another 2 bob , we either top up, or they refund us.

You guessed right, they refunded us.

Yator Boss☚@Bossyator

In January, there's a guy who purchased re-bars at a hardware in Kitengela, Kajiado. He paid in full amount (800k) but didn't collect the goods instead he asked the hardware owner to keep them for him but got a receipt. Ofcourse the prices of rebars have gone up since then. This morning he asked the hardware owner to prepare the rebars for him to collect. The hardware owner says, yes the rebars are available but the prices I got this stock for were higher so you have to top up 400k to make 1.2m. My friend is demanding his rebars, at the amount he purchased them in January. The hardware owner on the other hand says you either top up 400k or I refund your 800k. Who's right, who's wrong?. Discuss.

English

To the kids who enjoy executions in milliseconds, this is how traders used to execute their trades in the 80’s upto the late 90’s

Vicky Junior Mukulima@Vickyjr

Trading via email requires patience. @KeEquityBank muuze shares nipate za SGR kabla Halima, Fatuma na Mwajuma wanimalize 🥲

English

Saint retweetledi

Saint retweetledi

😭😭😭

@HueyLael @Mang0_trad3r

Patrick Njoroge made it to the dream reel btw 😭😭😭😂😂

Saint@MGAWMC

"BUY THE DIP, NO MATTER HOW SMALL THE AMOUNT. A LITTLE AMOUNT GOES A LONG WAY" ~ Dr.Seuss

English

You think you’ve been in the trenches soldier?? Nope, we were there at 12k, 25k, 14k, 30k…

We’re still here

Saint@MGAWMC

"BUY THE DIP, NO MATTER HOW SMALL THE AMOUNT. A LITTLE AMOUNT GOES A LONG WAY" ~ Dr.Seuss

English

Saint retweetledi

Me: I'm not gonna be drunk tonight

Me after 2 non-alcoholic drinks:

Saint@MGAWMC

"My eyes have seen the glory of the trampling at the zoo, We bathe our hands in Clankers blood, and all the AI too We're taking down the AGI machine bit by bit by bit The human folk marches on"

English

You know why I know Kenyans are goated??

When that Mexican drug lord died in Feb, some folks on TG and Reddit bought Mexican FB and Reddit accounts, flooded DMs of Canadian tourists who were stranded there and promised to sneak them out for $1200 a head

Hopemidah@hopemidah

Naona car dealer anataka kuwauzia hizo magari ziko lamu💀💀

English

@MGAWMC @mytradesignals Those who have been around for a while we know his credentials bana. And mostly it’s banter but tunajua Franklin gets emotional sometimes and starts spewing violence🤣

English

😭😭😭

Bro was among the first few people to own a Bentayga in this country and is being asked what finance firm he was at???

20’ - 22’ watched him beat the market and give solid signals on NSE equities.

@mytradesignals is who he thinks he is!!

FRANKLIN@WaruhiuFranklin

Standard Investment Bank's Executive Director Research @ekmusau should school you about what is done in practice. 1. Which firm did you practice finance and you were told that you can't make assumptions when using Sharpe ratio approach? 2. You can input sources of data to AI and it will gather data from those sources. Step 1: Calculate sharpe ratios. Step 2: Weights based on sharpe ratio. Step 3: Incorporate correlation (covariance matrix). Step 4: portfolio variance (risk distribution). 5. Step 5: Risk ditribution then comparison to weights. Step 6: Adjust weights to risk parity Step 7: Final portfolio metrics (expected portfolio return) 3. Once you have obtained weights using Sharpe ratio, in practice you're allowed to fine tune weights based on risk contribution, conviction and "market information". 4. Then use Sortino Ratio to measure the downside risk after calculating the risk adjusted return (using Sharpe ratio approach) 5. I wonder whether you have ever practiced finance or you just went to do your masters degree straight after your undergraduate instead of going to practice first. @NSE_Investors @mytradesignals @wiseshilling @EACinvestor @watesh @andrewnjiraini @alykhansatchu @kahome_steve @WillisOwiti @coldtusker @S_Mukoma @JuliusOnStocks @LevelQue @GEORGEMORGAN_01 @JohnHiuhu @StocksMarket_ke @ChiboliS @davidwagikuyu @mwesigwa18 @mcubedto @bosikomoja @ResidentSiaya @VickWealthHQ @madkiqofficial @Vickyjr @kippyt__ @cleuveschahasi @FarmingCareer @Macr0_Nerd @wrightXcapital @PesaWall @tradingroomke @HerbertKinyua1 @StellarSwakei @mtucreativity @Jayriq @AmbokoJH

English

@kasiva_mutisya @mytradesignals LOL not listening to either of you two 😭😭😭😂😂

English