@NoLimitGains Fuck that fool and fuck you for posting this and making me see his face

English

CJ

3.4K posts

@MMLABZ

#WEB3 #Crypto #Stocks #Investor #Youtuber.

🇺🇸 This absolute monster named Tesfaye Cooper, the same thug who tortured a disabled teenager on Facebook Live, is back on the streets. The twist?? He just got arrested again... okay, who am I kidding? Of course he was. He chased down a cyclist who simply waved at him, beat him, spat on him, screamed “Gangster Disciples,” and stole his bike. Released after only 7 years for the first savage attack. In a saner penal system, this predator would never see daylight again. Disgusting. Lock him up for good. Source: @CollinRugg

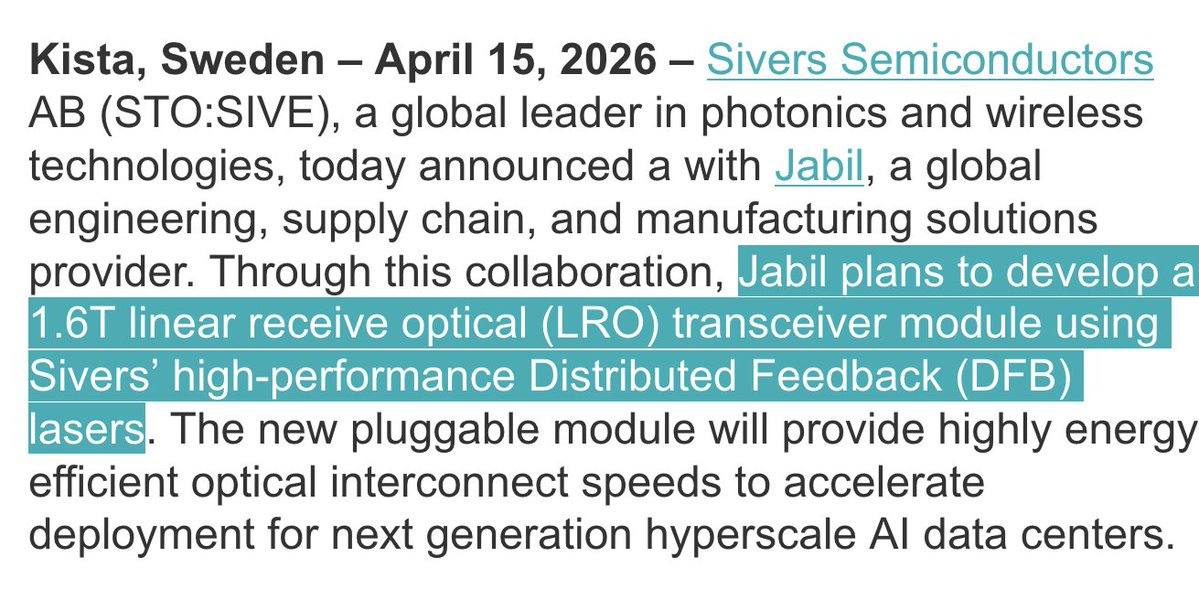

$SIVE is the next $LITE at $560m MC. Institutions just got full confirmation today: Sivers is now the light source in hyperscaler supply chains and the direct supplier of $JBL optical transceivers. It’s only a matter of time.