Matthew Kisner

137 posts

My post about CPI from 4 days ago! It is important to be able to interpret the market in advance! 💯👇

English

@Agrippa_Inv @TheTechInvest @IRENBULLLL Really? Who doesn’t want a giant data center in the back yard? It adds a nice element of “character” to the neighborhood. Plus, everyone loves the dust and construction sounds throughout the day. Sounds amazing to me! 🤣🤣😜

English

@TheTechInvest @IRENBULLLL Who builds a 300 MW data center hundreds of feet away from a residential area? $NBIS is desperate to lock up power, while completely ignoring nearby residents lol.

Talk about a neocloud NOT doing it the right way…

English

🚨 BREAKING: JUDGE RULES OXMOOR VALLEY NEIGHBORS’ LAWSUIT AGAINST $NBIS DATA CENTER CAN PROCEED

1. "Ruling comes the same day the Greater Birmingham Humane Society filed a separate suit over the project."

2. "The two lawsuits come less than a year after $NBIS purchased the land."

3. "A preliminary injunction hearing — where neighbors will ask the judge to halt construction entirely — is now set for Tuesday, July 14 at noon and continues Thursday, July 16."

The Tech Investor@TheTechInvest

🚨BREAKING: $IREN HAS OFFICIALLY BROKEN GROUND ON SWEETWATER 2 Source: @FransBakker9812

English

@Agrippa_Inv @themartian890 What an idiot! You are thorough and explain things well with detail. There are plenty of orther people on X that just post a few sentences. May be better to follow those folks. Good luck!

English

@themartian890 Lmao are you for real? 🤣 Just unfollow mate, my acc ain’t for you

English

Reflecting on $IREN

Over the last couple of days I spoke with multiple people in close contact with $IREN's management team, including investors who attended the RAISE Summit this week.

Given the insights I've gathered, I think it's an appropriate time to reflect on $IREN and share my latest thoughts.

It's no secret that $IREN has been somewhat slow on the commercial side, at least relative to the likes of $NBIS and $CRWV. I for one thought we'd have seen a Sweetwater deal by now, let alone substantial parts of the remaining Childress capacity pre-contracted.

So what's stopping $IREN from signing these multi-hundred MW deals?

In short, nothing is really "stopping" them. It comes down more to a few factors shaping their decision to hold off where other cloud providers perhaps wouldn't.

Based on management's comments both on and off camera, I can confidently say demand truly isn't the issue. Cloud capacity in this market is sparse and supply can't keep up. In fact, I've heard $IREN could easily sell out 100% of its 2027 capacity today if it wanted to.

The catch is that selling capacity which won't come online for another 6, 9, or 12 months yields significantly less than capacity arriving sooner. Customers want capacity today, and they're willing to pay a substantial premium for it.

So while selling far into the future might prop up the stock, commercially it may not be the most prudent strategy in this environment. That dynamic can obviously shift over time, but given how far supply sits behind demand, it won't change overnight, and as it stands, holding off as long as possible yields better long-term returns.

Not only do returns shrink the further out you pre-contract, but the available buyer pool shrinks with it. Selling capacity well into the future means gatekeeping much of the smaller, higher-margin clientele while mostly attracting the lower-paying hyperscalers.

As we know, $IREN is increasingly moving up the stack, effectively cutting out the middle-man that hyperscalers represent, as evident in their recent Mirantis acquisition. On that note, $IREN apparently has multiple LOIs and customer commitments for high-margin managed cloud services set to take effect once the Mirantis deal closes over the coming weeks.

I've now also heard several times that $IREN takes customer selection and contract structure extremely seriously. Creditworthiness matters, but management also wants clients that can scale their compute demand substantially as $IREN ramps capacity. The only near-term downside is that this due diligence takes time, yet the longer-term advantages of the approach are obvious.

Beyond contract timing and customer selection, I believe some of it also comes down to operational reasons.

We know the 1.4 GW Sweetwater campus is earmarked for the upcoming VR200 (Rubin) capacity, whose supply won't ramp until late this year into early next. That partly explains why the site isn't up and running already, since all they could lease out right now would be current Blackwell generation.

The flip side is that $IREN could simply build "Horizon-style" capacity at Sweetwater, the same style they're currently developing at Childress, since those facilities are fully capable of housing next-gen Rubins, and have them ready by early next year, right as NVIDIA fully ramps Rubin production.

And while $IREN is already doing foundation work at Sweetwater, it could still easily take another 3-4 quarters before we see operational capacity there.

So what's the holdup?

I believe a major reason for the slow ramp at Sweetwater is that they want to implement lessons learned from their Horizon build-outs at Childress, making the Sweetwater process more efficient, less costly, and thus more economical.

Here I want to give a big shoutout to my friend @FransBakker9812, who found that $IREN has recently developed proprietary methods to make elements of the construction process significantly more streamlined, saving time and cost across all future liquid-cooled builds.

He shared more specifics on that with his "Research” and “Founding” subscription tiers, which I recommend checking out.

I firmly believe what some might see as a relatively slow ramp, given $IREN's starting position, is management's way of doing things right. Start with the first liquid-cooled buildouts in Horizons 1-4, implement lessons from one Horizon batch to the next, then apply the full set of process and workflow improvements at Sweetwater.

This closely mirrors what $IREN has always done since its mining era, when it started small and progressively scaled its construction operations in both size and speed. A true construction flywheel.

Interestingly, I've just heard that $IREN plans to develop Sweetwater 1, Sweetwater 2, and the 1.6 GW Oklahoma site in parallel over the coming years. That shows just how exponential their construction ramp really is.

In short, I believe holding out on the next wave of contracts comes down to a few factors:

1) Signing well ahead of commissioning means giving up pricing upside and attracting only a small subset of clients.

2) Customer selection and contract structure are a big part of $IREN's long-term strategy. It takes more time than simply selling to the highest bidder, but should build stronger customer relationships over the long run.

3) Scaling construction in a controlled manner, carrying critical lessons from current builds into the next. Slow start, exponential growth curve.

None of this means we won't see any deals this year, but it does add color on why commercial progress on closing deals has been slower than many of us expected.

As for deal activity and my current expectations there, it helps to step back and consider how $IREN's near-term capacity is structured.

We should expect the 50k B300 units $IREN procured back in March to be fully contracted and installed by year-end, roughly 33k at Mackenzie and another ~17k at Childress. Apparently first deliveries for Mackenzie have already arrived and are being installed.

Given this progress, I'd expect $IREN to announce having contracted substantial parts of these air-cooled Blackwells by August earnings at the latest. This is the low-hanging fruit.

And worth noting, since $IREN first gave ARR guidance for that capacity, GPU rates across the board have moved up substantially. If they sign anything close to what they landed with the 60 MW NVIDIA deal, their year-end guidance of $3.7B should climb to at least $3.9-$4.1B.

Beyond this, there's plenty of 2027 capacity that could get contracted later this year, including 190 MW of air-cooled capacity at Childress, 30 MW at Canal Flats, 150 MW of liquid-cooled Horizon 5-6, and 300 MW of liquid-cooled capacity at Sweetwater 1.

We don't have guidance on when this capacity comes online next year or what the ramp schedule looks like, but since liquid-cooled greenfield development takes longer than retrofitting existing air-cooled buildings (currently mining BTC), I'd expect the remaining 220 MW of air-cooled capacity to come online within the first couple of quarters of 2027.

For that reason, I think the odds those few hundred MW get pre-contracted later this year are relatively high.

The trickier part is the 150 MW of Horizons 5-6 and the 300 MW of liquid-cooled Sweetwater capacity. I think there's a decent shot at least one of the two gets pre-contracted in 2026, especially if it's for a hyperscaler or a frontier lab, which are far more inclined to sign a few quarters ahead.

Either way, it's just a matter of time until contracts start flowing. It's clear to me that $IREN is playing the long game and isn't compromising long-term upside for short-term euphoria in the share price. As a long-term investor, I fully support that.

I do wish, however, that $IREN were a bit more open about strategy and roadmap. It's obvious they're holding their cards close to the chest, but I find management has been overly vague on strategy.

It takes investors like me piecing the puzzle together to make sense of how $IREN plans to scale into the next hyperscaler. Ironically, management does share a fair bit of interesting and useful information if you get the chance to meet them in person, yet on earnings calls they come across as overly reserved.

That said, the future looks bright, and I have no reason to get overly concerned about disappointing price action. With a bit of luck we're in for a string of positive catalysts, starting with the Horizon 1 handoff in a couple of weeks.

I also want to take a moment to thank @OMCapitalGroup, who did an excellent job gathering information and insights while attending RAISE this week.

If it weren't for his work, I wouldn't be nearly as informed, so big props to him for taking the time to travel all the way to Paris for $IREN due diligence and then going out of his way to keep me updated with everything he picked up, even putting some of my own questions to management directly.

He's relatively new to X, but he told me he's going to start posting shortly and jump into Frans' spaces more often. Do me a favor and give this fella a follow.

Have a good one, cheers! ✌️

Thumbnail Credit (enhanced version): @AndyDTrades

English

@XCapitalMgmt Great analysis and connecting all the dots @XCapitalMgmt!! What you have laid out seems very plausible - it would explain a lot of the behavior from IREN. It also could be what Mike A. mentioned in a space about an announcement later this year.

English

Matthew Kisner retweetledi

If you missed the $iren Board Response, please see 👇

iren.gcs-web.com/static-files/4…

English

@BecauseBitcoin I still drink 6 beers (Sapporo) a day and I am 46! And I am fit…lol

English

Why did $IREN drop the comp package NOW, and not alongside a deal?

I see a lot of people complaining about this.

It's normal.

Emotional investors.

We all suffer from emotions occasionally.

But the logic here is very, very simple.

Play it forward.

Imagine they announce a monster deal first, the stock runs to $100, everyone's euphoric.

THEN they announce this exact same package.

At $100, the headline numbers are twice as big.

The sell-off is massive.

The drama is deafening.

They go from loved to hated overnight, and the comp story poisons the deal story.

Now play it the way they actually did it.

Announce it now, with the stock on the floor.

Yes, people hate them for a week.

But nobody sells, because everyone knows the price is already depressed.

Discontent, sure.

Panic, no.

And then?

Then the deals come.

The euphoria returns clean, with nothing hanging over it.

That's why the "bad news" gets announced BEFORE the good news.

Not after.

It's not a conspiracy.

It's sequencing.

Pure logic.

Now, the part almost nobody says out loud: this "bad news" is actually good news for me.

I now KNOW that Dan and Will Roberts will take less than 1% a year from me. For five years. In writing.

We won't see Dan Roberts trying to pump the stock to get his bonus, he'll care about the business.

He obviously wants an 0.5% of a $100B company rather than 0.5% of a $5B company.

And not only that: the percentage SHRINKS every year, because the grant is a fixed share count while shares outstanding keep growing.

Year two it's smaller than year one.

Year three smaller still.

Compare that to peers like NUAI, where one year they carve out 10%, and next year, who knows, maybe more.

Honestly?

IREN's package is a relief.

Nothing scandalous about it.

Quite the opposite.

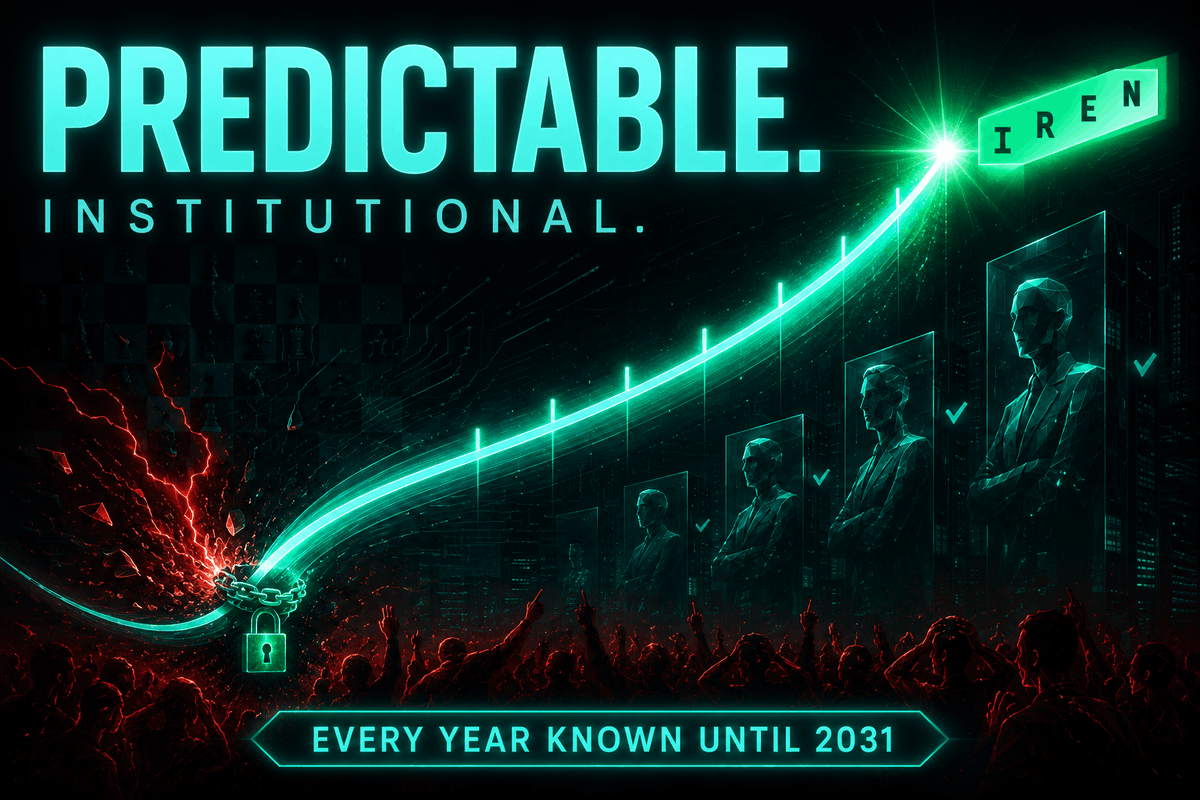

This is EXACTLY the corporate structure institutions love.

Any institution buying IREN today knows, to the decimal, what management takes every single year.

No surprises in 2027.

None in 2028.

None in 2029.

None in 2030.

Sealed until fiscal 2031.

Predictable.

Stable.

Modelable.

Retail sees a scary headline.

IInstitutions see a solved variable.

Guess which one moves the stock.

This is not financial advice. Do your own research.

I'm long $IREN.

ChinoAleman@chinoalemano

I see a lot of bad-faith actors around $IREN. And plenty of honest people simply misinformed BY those bad-faith actors. That's exactly why I'm running this Hunt Series, comparing IREN against names like $NUAI, $SLNH and $HUT, straight from the filings. IREN's comp package is among the best in the sector. The cleanest. The least predatory. Just some bad actors taking the headline out of proportion, taking 5 years of compensation to scare you. Now, some will say: "why not performance-based?" Fine. Let's play that movie forward. Dan and Will set a $70 stock price hurdle, and in exchange take 5% of the company. Then a $100 hurdle, another 5%. And so on, milestone after milestone, until they've carved out the whole thing. That's the HUT model. "But but but, make them set $300!" Sure. They'll set $1,000 just to please you. Come on. In the real world, boards set REACHABLE hurdles. That's the whole game. The exec hits the realistic target, collects 5% in one slice, and then? Then the stock price can go to hell for all they care. They already collected. Look at BITF. Awards that paid out with the stock at $6. Stock at $2 right after. They did everything (X post, etc etc) to get it to $6. Cash their bonus. And who cares about the stock price later. The bonus didn't fall with it. That's the dirty secret of "performance-based": it pays on the way up and doesn't claw back on the way down. Also, without performance, names like NUAI and SLNH hand out ~10% in a single year. Now compare IREN's structure. ~1% per year, for five years. FIXED share count, so it SHRINKS as a percentage every year the company grows. Locked for six years, they can't sell a single share on the way. Nothing more until fiscal 2031, in writing. They don't get paid for touching a price target once. They don't need to care to pump the stock. They get paid for still being there in 2033, with the entire ride, up or down, on their own backs. Is it the perfect package? No. The perfect package is 0%. Sure. Dreaming is free. In the real world, this is about as clean as this sector gets. The filings say so. The Hunt continues. This is not financial advice. Do your own research. I am long $IREN.

English

English

I respect @bitcoinbutcher1 a lot.

His decision comes as a surprise, but I understand his sentiments.

I hope to see you in one of the Sunday night spaces as a guest speaker mate, your wisdom as $CIFR holder is welcome regardless of your $IREN position.

As for me, I'm not f*cking leaving.

Multiple calls scheduled with IR in the coming week, and I will do my best to get @danroberts0101 on a space this month.

Have a great weekend fam 🫡

₿itcoin ₿utcher 🥩 🐑 🐷@bitcoinbutcher1

I sold my $iren this morning premarket and have reallocated to $nuai $wulf $cifr Right now I’m focused on my 4th of July holiday business and will follow up with a space or post to give more detail to those at are concerned with the reasons

English

Matthew Kisner retweetledi

The Most Important Thing in the Neo-Cloud Industry: Building a Self-Reinforcing Capital Flywheel

What is the best way to evaluate the long-term potential of the Neo- cloud industry?

I believe there is only one answer: identify which company can quickly build a self-reinforcing flywheel between capital investment and capital returns.

In this model, a company continuously invests in high-quality AI computing infrastructure while generating growing free cash flow. At the same time, its reliance on external financing gradually declines. It establishes a clear path of capital investment → cash generation → larger investment → greater cash generation, ultimately reaching a point where its own cash flow is sufficient to sustain the entire cycle.

Only company that achieve this have a real chance of winning in the future.

Stock prices can be highly misleading. What the market focuses on in the short term is not necessarily what will determine long-term success. Instead, we should evaluate how each participant performs in building this flywheel.

To build such a flywheel, six conditions must be met.

First, low-cost energy assets.

Whoever can secure abundant, stable, low-cost, and green energy over the long term will enjoy a generational advantage in cost structure.

Energy is the first principle of this industry. It is the foundation upon which the flywheel begins.

Second, stable cash flow from high-quality tenants.

This is the cash-generating engine of the flywheel.

Third, package stable cash flow together with computing assets into Asset-Backed Securities (ABS/ABF), allowing future cash flows to be monetized in advance through the capital markets.

This is the accelerator and financial leverage of the flywheel.

This is also the step that turns something ordinary into something extraordinary.

By packaging long-term customer contracts together with AI computing assets into financial products similar to REITs or Asset-Backed Securities (ABS/ABF), companies can monetize future cash flows today through the public capital markets, enabling capital recycling and recovery.

Fourth, expand capacity to improve energy utilization.

This is where scale economies come into play.

Larger scale further reduces marginal costs, improves Power Usage Effectiveness (PUE), and attracts more high-quality customers who value stability and cost efficiency.

The larger the platform becomes, the better it can optimize scheduling, spread costs, and improve utilization, creating a positive feedback loop that allows the flywheel to spin faster and faster.

Fifth, computing orchestration and full-stack service capabilities.

These maximize the efficiency of the flywheel.

Only when a company possesses integrated hardware-software scheduling systems, large-model fine-tuning capabilities, and highly efficient operations with minimal losses can energy truly be transformed into marketable AI computing products.

Sixth, alignment with policy incentives and industry standards.

This includes carbon footprint compliance, green finance, carbon credit mechanisms, and similar frameworks.

This ensures the flywheel can continue operating smoothly.

Green AI infrastructure gains access to lower-cost financing and stronger policy support, further improving capital efficiency and reducing expansion costs.

These six conditions are strict benchmarks.

Any company can be measured against them, and we can quickly see who is actually on the right path.

Take Oracle as an example.

Oracle has an outstanding legacy business, a stable customer base, and excellent cash flow. After recognizing the enormous opportunity in AI, it dramatically accelerated investment.

But has it successfully built this new industrial flywheel?

The answer is no.

Rather than comparing every point one by one, I'll simply mention the result.

All three major credit rating agencies currently place Oracle's credit rating close to the edge of non-investment grade. One more downgrade would move it into junk bond territory.

Google, Microsoft, Meta, and Amazon all possess exceptional cash flow businesses and strong balance sheets.

They are diversified giants.

However, their size also creates limitations.

They cannot devote all of their attention to developing the new cloud industry.

Although they continue investing heavily, they failed to secure first-mover advantages in premium energy resources, especially grid-connected gigawatt-scale sites.

The power projects they have announced are impressive, but most will not come online for another three to four years.

Many rely on geothermal, nuclear, or other emerging energy sources whose technological maturity, cost control, and commercial viability are still being tested.

CoreWeave and Nebius both attempted to build neo- cloud businesses using an asset-light model, hoping to avoid heavy infrastructure investment.

Reality has largely disproven that approach.

Both companies now recognize the problem and are attempting to pivot.

Unfortunately, the optimal window for making that transition has already closed.

Economically attractive sites have largely been taken.

If they move into behind-the-meter power generation, they must still confront questions surrounding reliability, technological maturity, and cost control.

Measured against these six requirements, CoreWeave and Nebius remain far behind.

CoreWeave also carries a credit rating approaching dangerous territory.

The AI industry has barely begun, yet its financial position has already become highly leveraged.

That reflects very poor execution by management.

Nebius has delivered the strongest stock performance this year.

But what foundations has it actually built for long-term development?

Its front-end execution has indeed been excellent.

It has signed numerous customer contracts, filled most of its capacity, acquired several important software companies, and established the vision of building an AI Token Factory.

Its cash balance appears healthy.

Its AI business growth appears impressive.

However, it has largely treated the unavoidable issue of heavy infrastructure investment as a black box.

Its leasing strategy temporarily obscures the problem, but ultimately this challenge cannot be avoided.

Especially now that Nebius is increasingly emphasizing vertical integration, it will eventually have to undertake substantial capital expenditures.

When that happens, today's seemingly abundant cash balance could disappear very quickly.

Because of space and time constraints, I cannot compare every AI cloud company individually.

I have selected only several representative examples.

The barriers to entry in this industry have become extremely high, especially now that development has entered the era of gigawatt-scale AI factories.

Realistically, the number of companies capable of competing at that level can probably be counted on one hand.

Among companies that satisfy all six conditions—and continue strengthening them—$IREN stands out the most.

Rather than comparing every point again, I'll focus only on the third requirement:

Packaging stable cash flows together with computing assets into Asset-Backed Securities (ABS/ABF), allowing future cash flows to be monetized in advance through the capital markets.

This is the accelerator and financial leverage of the flywheel.

On June 1, 2026, IREN announced the successful completion of its ABF financing.

This $3.65 billion investment-grade GPU financing became a landmark event for the entire industry.

Not only did it provide the core funding supporting IREN's AI cloud agreement with Microsoft, but it also received an A rating from Fitch and an A(low) rating from DBRS, making it the highest-rated publicly disclosed GPU financing transaction to date.

It also became the first structure of its kind to enter the U.S. private placement market, marking the first time AI computing assets were accepted by capital markets as genuine investment-grade infrastructure.

The financing structure itself was even more sophisticated than many expected.

IREN combined $2.1 billion of U.S. private placement fixed-rate notes (SOFR + 2.13%) with $1.55 billion of delayed-draw term loans (SOFR + 2.25%), resulting in an overall blended borrowing cost of approximately 6.00%.

This financing covered roughly 96% of the $5.81 billion GPU capital expenditure required under the Microsoft contract.

Goldman Sachs and JPMorgan served as joint lead arrangers, further strengthening the transaction's credibility among institutional investors.

Even more importantly, once Microsoft's $1.94 billion customer prepayment under its five-year, $9.7 billion contract is included in the overall capital structure, IREN's effective financing cost falls further to approximately 3.31%.

In other words, IREN can fund nearly all of its GPU capital expenditures without issuing significant new equity, achieving an exceptional balance between infrastructure expansion and shareholder dilution.

Looking at the outcome, this financing represents much more than simply raising capital.

It serves as a model for optimizing capital structure.

It enables IREN to execute its Microsoft contract without sacrificing shareholder interests, while bringing GPU assets into mainstream institutional portfolios as investment-grade credit.

It marks the beginning of the financialization era for AI computing infrastructure.

Remarkably, when this major announcement was released, it generated almost no reaction in the capital markets.

Based on my understanding of what matters most in this industry, I believe this was the single most important piece of AI infrastructure news during the first half of the year.

It demonstrates that the long-standing gap between capital investment and capital returns is finally being bridged through high-credit financial structures.

Its significance is enormous.

For $IREN investors, three additional implications deserve attention.

First, the most important signal is the fundamental upgrade of the collateral structure.

This represents a true milestone.

The combination of GPUs + Microsoft's take-or-pay contract cash flows + data center ownership received an investment-grade A rating.

For the first time, financial markets are pricing AI computing assets with the credit quality normally reserved for infrastructure bonds rather than assigning them the risk premium typically associated with high-growth technology companies.

As capital costs decline and financing channels expand, the financialization of AI computing assets becomes genuinely repeatable.

For the first time, financial markets recognize AI infrastructure as an asset class that can be pledged, priced, and rated.

This externally validates the foundation of the flywheel.

Second, the rating agencies placed tremendous emphasis on ownership of the data centers themselves.

Daniel Roberts made this point very clearly.

The foundation of investment-grade financing is not the GPUs alone.

Rather, it is the combination of physical ownership of the data centers where those GPUs operate together with high-quality customer contracts.

Together, these two elements create the confidence necessary for institutional capital to participate while demanding much lower financing costs.

In other words, IREN's build-own-operate model is not merely an operational advantage—it is also the prerequisite for upgrading its financing structure.

Companies that rely primarily on leased facilities—whether CoreWeave, Nebius, or even Oracle—cannot easily replicate this credit structure.

Third, this transaction establishes an industry precedent.

It is not simply another debt financing.

It is the first transaction of its kind in the U.S. private placement market.

Fitch assigned an A rating.

DBRS assigned an A(low).

These ratings demonstrate that agencies recognize the structure as a relatively high-quality debt instrument, opening an entirely new financing channel for AI computing assets.

Because the collateral structure has now been accepted by the market, investment-grade financing has become reality, and the capital recycling mechanism has taken shape, the third stage of the flywheel has officially begun.

Why is this event so important?

Because it fundamentally changes how IREN finances growth.

The creation of the ABF represents a paradigm shift.

Previously, expansion depended largely on shareholder dilution, market sentiment, and external equity financing.

Now, the process begins with contracted rental cash flows, which become collateral for structured financing that funds new construction and attracts additional high-quality customers.

IREN has evolved from "asking the market to believe in the company" to "letting the assets speak for themselves."

The prerequisite for all of this is high-quality collateral.

If Horizon 1 can already support A-rated debt financing today, then what could become possible once the flagship DSX-powered AI Factory is completed?

Can everyone appreciate just how powerful the flywheel IREN has initiated could become?

The market has long criticized IREN for shareholder dilution.

But if this flywheel is successfully established, future dependence on ATM equity issuance could largely disappear.

If that happens, today's decisions will prove worthwhile.

Within today's aggressive and highly competitive AI industry, this type of conservative yet efficient financial leverage could prove genuinely transformative.

Now that the ABF financing structure has been established, several additional amplifiers can further accelerate the flywheel.

One of them is the monetization path enabled by Mirantis.

Its importance extends far beyond completing the software layer.

It transforms IREN's physical infrastructure from AI compute that can only be sold locally into a standardized, repeatable, exportable AI factory solution capable of commanding premium pricing.

Everything—from compute orchestration and container management to large-model runtime environments—can eventually be standardized and delivered as a complete solution.

This means IREN can continue expanding revenue through software and platform capabilities without proportionally increasing physical capital investment.

Once its flagship AI factory is operational, this advantage should become even more pronounced.

This changes growth from a linear model into a nonlinear one.

The flywheel evolves from expanding through additional assets to expanding through replication of an integrated system.

At this stage, the single most important milestone for IREN is Horizon's delivery schedule.

Only if new capacity comes online on time and successfully attracts even higher-quality customers can capacity expansion and customer upgrades connect seamlessly.

Whether the market speculates about Anthropic, sovereign AI, or enterprise sovereign AI, all of those developments rank behind Horizon in importance.

Now compare this with CoreWeave and Nebius.

When they sign a new deal, the value created is largely limited to the deal itself.

The benefits mainly include:

Receiving customer prepayments that ease funding pressure.

Gaining additional credibility that helps them raise financing from banks and financial institutions.

When IREN signed its Microsoft agreement, however, it achieved both of those benefits—and something far more important.

It transformed those assets into A-rated ABF securities, unlocking the value of its asset base and creating a high-quality capital recycling mechanism.

With 5.8 GW of secured power capacity, imagine how much capital this structure can ultimately unlock.

This is precisely why IREN has not rushed to sign additional deals before completing these foundational milestones.

The company first needs to provide the market with confidence that new computing capacity will be delivered on schedule.

Horizon must demonstrate that capability.

Once 5.8 GW of secured power translates into reliable AI factory delivery, every future customer contract can potentially become another ABF transaction.

Combined with the growing cash flows from newly deployed capacity, IREN could ultimately solve the industry's greatest challenge:

Building a heavy-asset business capable of funding its own future growth through internally generated cash flow.

Everything required to achieve this actually began back in 2018.

Secure energy assets through land acquisition, power agreements, and long-term contracts.

Sign the Microsoft agreement and develop Horizon.

Build the NVIDIA partnership and the DSX flagship AI Factory.

Deploy Sweetwater.

Complete ABF securitization with an A rating, packaging AI computing assets and contracted cash flows into investment-grade debt.

Every step serves the same ultimate objective:

Transform IREN from a company that depends on continuous external financing into one whose own assets generate the capital needed for future growth.

Whoever achieves this first will possess the industry's hardest competitive advantage to replicate.

Technology can be copied.

Power shortages may eventually ease.

Even data centers themselves can be replicated.

But once a capital structure develops this kind of path dependency, it becomes extraordinarily difficult to duplicate.

Finally, I would like to thank @FransBakker9812 for emphasizing the importance of the ABF structure and for highlighting the significance of Horizon's delivery timeline.

He identified what truly matters.

English

@FransBakker9812 @JoshTradeOption The fire pit is a nice touch, too!

English

TODAY I SOLD MY $IREN

Updated Portfolio:

$HIMS 500 shares

$ZETA 500 shares

$SOFI 500 shares *added 100 more

$ROOT 11 shares

A big reason for this is I expect a bit of a market rotation. I’m also just frustrated that $IREN is not the best in their sector and I already made a lot on what was supposed to just be a short term trade for me last summer when I bought at $18. I’m sitting on the rest of the capital waiting for the next move, but I did add 100 more shares of $SOFI

English

@bitcoinbutcher1 @DavidSacks @danroberts0101 The US government is not going to sign with IREN to provide any type of classified computing since they are an international company. Its a non-starter!! Australia is part of the Five Eyes - this has a less than .05% chance of happening IMO.

English

Always a must read when I’m not thinking big enough

@DavidSacks @danroberts0101 have been in too close proximity for $iren to not get a chance pitch with government

phads@PhadsEth

English

@FransBakker9812 @PhadsEth @mikealfred Good write up but I believe this is still not thinking big enough. The thought process is still around a “customer”. A customer will be the byproduct of the strategic moves they make. Just my two cents.

English

@marksotoges @dom_lucre No that is real. It’s in the Brazilian news.

English

🔥🚨LATEST: Footage has released of the moment the 21-year-old woman was accidentally killed when Entre Cordas workers forgot to attach her safety rope and and threw her off the the “Skeleton Bridge” in Limeira, a city in Brazil’s São Paulo state.

English

@Bare_Birk You guys think Jensen talks DSX at GTC on Mon - mentions SW, shows drone footage, etc...?

English

Matthew Kisner retweetledi

IREN has entered into a $1.6bn purchase agreement with Dell for air-cooled Blackwell systems to support its previously announced 5-year, $3.4bn managed services AI cloud contract.

The systems are expected to be deployed across existing data centers at Childress, Texas, with commissioning targeted for early 2027.

Upon commissioning, the AI cloud contract is expected to increase IREN's annualized run-rate revenue (ARR) from $3.7bn to $4.4bn.

@danroberts0101, Co-Founder and Co-CEO of IREN commented:

“Securing capacity and accelerating commissioning are our top priorities in a market where time-to-compute is everything. Hyperscalers, enterprises and developers choose IREN as a partner because we own and control the full stack - the physical infrastructure, the compute, and the operational capability to deploy at scale.

Our relationship with Dell ensures access to hardware at the scale and speed the market demands. Every deployment we complete makes the next one faster, and that compounding execution advantage is what we are building.”

Learn more: iren.gcs-web.com/static-files/6…

English