Andrew Perry retweetledi

Another excellent weekly contribution from @YraHarris at MacroPillars.

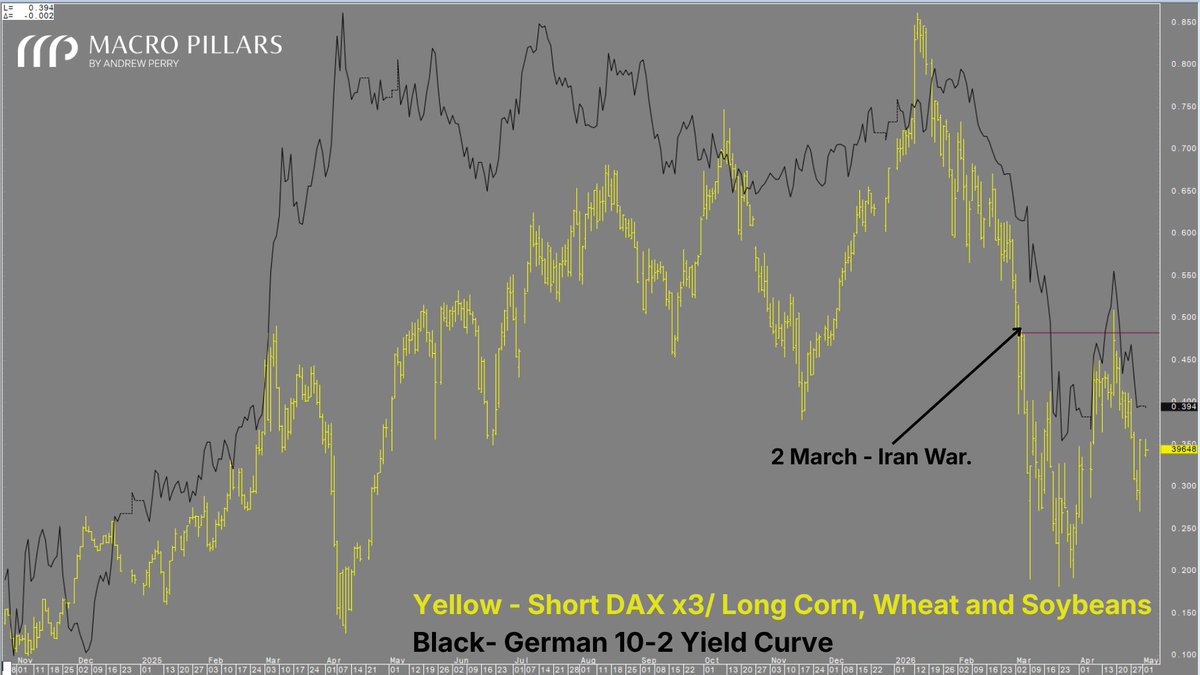

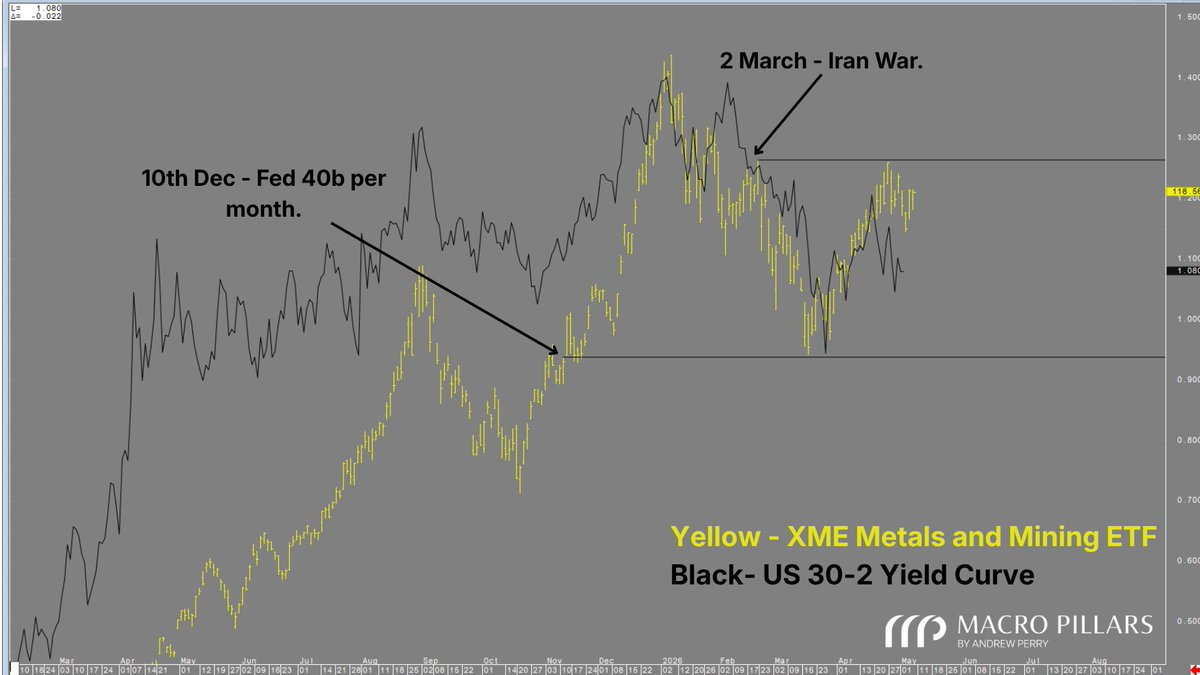

This week, Yra continues to follow the divergences building across grains and energy. He also touches on the rice supply shock, Bessent’s pressure on Trump, Warsh, the Fed, QT, the long end, Japan’s policy mistake, the yen, JGBs, and why the market may be far too complacent.

The section on Warsh, QT, and the long end is especially important:

“I understand the market moving them higher in anticipation, and with all the talk of higher inflation, but I just don’t see it happening, especially into the election. The market might push this, but it doesn't really have the power to do so in the short end. So if they take it out on the long end, it’s going to be a real problem for Scotty and some others, and I think that’s what scares them the most.

In terms of the front-end tightening in the US, with Warsh coming in and embarking on quantitative tightening, there is no way they will actually raise rates. They have to see how it plays out and what effect it has, because they will be curtailing bank reserves in a big way, and we know they already brought in the RMP from 40 to 10 billion. Warsh is smart and respects markets; Powell says he respects markets, but I don't think he does, because in 2018, he made a categorical mistake, as Druckenmiller dubbed it "the double shotgun" approach. If you're doing quantitative tightening, you hold rates; if not, cut rates, and see where it goes.”

Sign up for a 14-day free trial to receive the full article and all Macro Pillars research.

buy.stripe.com/8x27sNfwK17ld3…

English