Marieke retweetledi

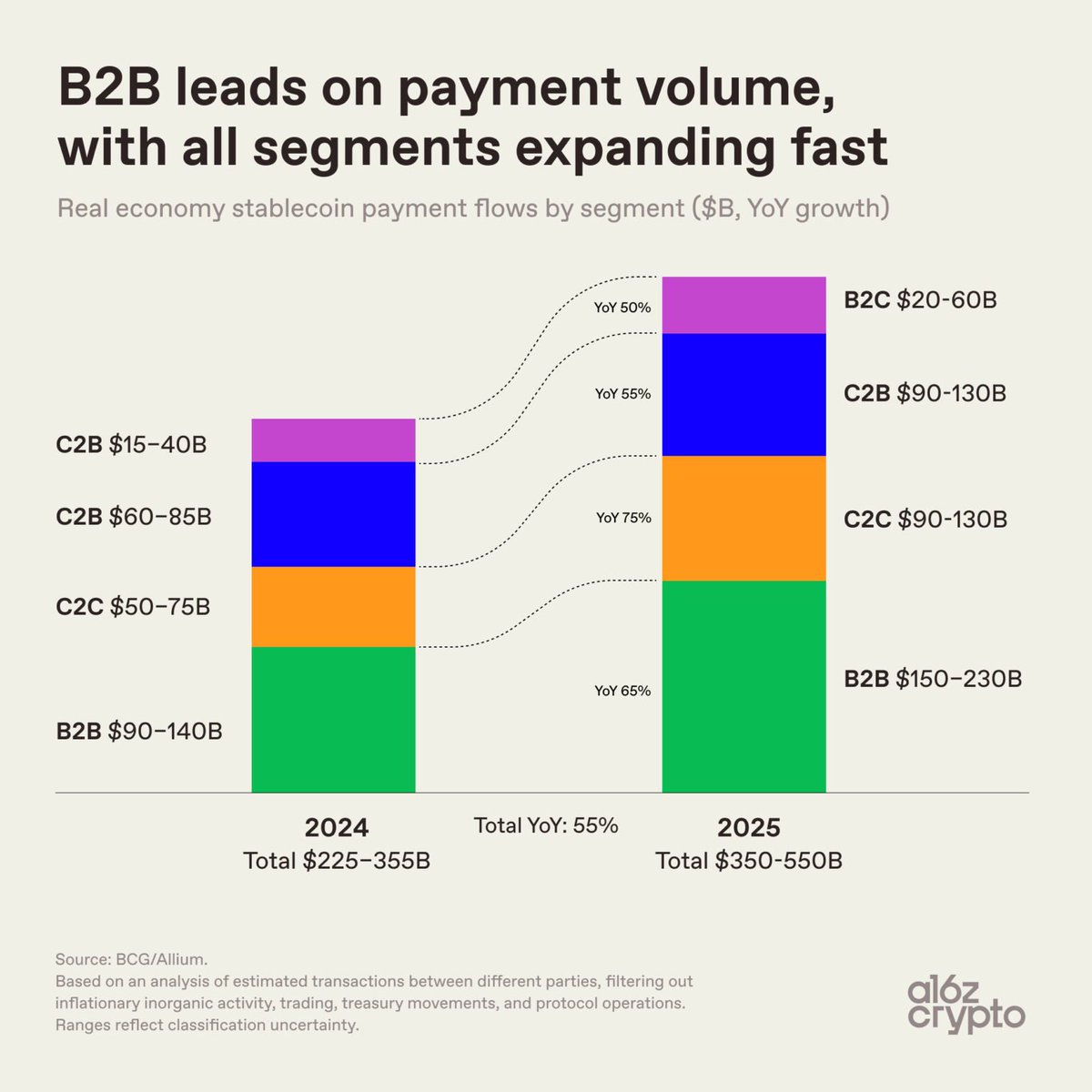

Stablecoin B2B payment volume just keeps compounding! 📈

🔹 2023: $3.5B

🔹 2024: $19B (5x)

🔹 2025: $66B (3.5x)

🔹 2026 forecast: $147B (2.2x) by @obchakevich_ and @artemis

That's a 42x increase in 3 years.

Why it's happening?? cross-border B2B via SWIFT costs 3-5% and takes 2-5 days. Stablecoins settle the same route in seconds for under $1.

For companies paying suppliers in Asia, Latin America, or the Middle East, this isn't an experiment anymore. It's an operational necessity.

Regulatory clarity (MiCA in Europe, GENIUS Act in the US), better infrastructure, and new B2B payment rails being built directly on stablecoins are all converging at the same time.

Bullish.

English