Supersleuth

4.3K posts

It’s funny that people think POTUS is the worst president ever, the man just took out the worst terrorist regime in modern history within 32 days.

Stock market volatility at extreme levels only last so long.

English

@Kaizen_Investor 🤔 not even after this bloodbath. Must be a sell then. I’ll defo trim. Thanks

English

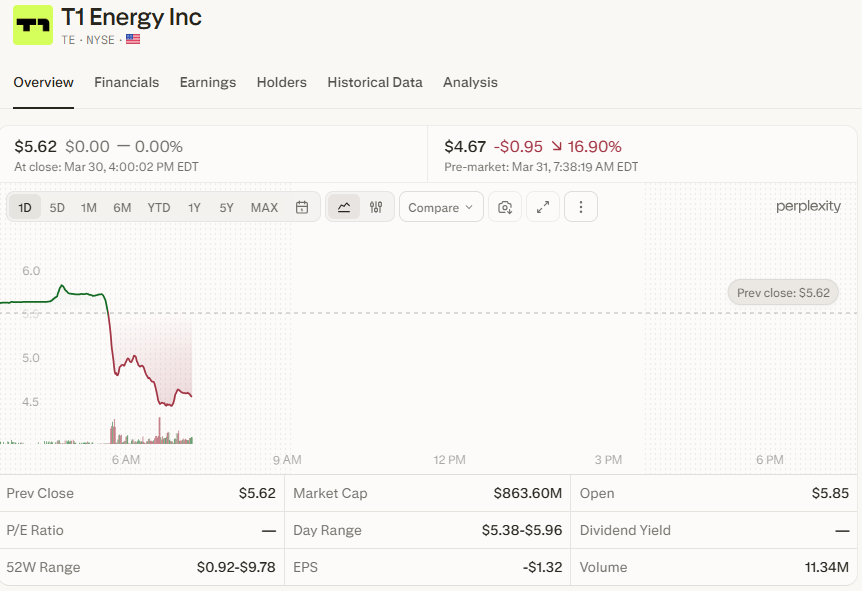

$TE down 17% today after earnings. The problem is that the thesis was mainly built on promises of the management.

The management assured a +$410M revenue quarter during the Q3 earnings call. They ended up missing this estimate by 13%.

Another problem is the profitability. Analysts were hoping to see T1 narrow its losses, but the company reported a staggering $380.8 million net loss for 2025, with full-year Adjusted EBITDA coming in at negative $65.0 million.

The timeline on G2 Austin was not delayed. But the main worry will be the funding of G2. Phase 1 of G2 Austin requires an estimated $400 million to $425 million in capital expenditures.

With G1 Dallas continuing to burn cash and the company sitting on a massive net loss, T1 might be forced to issue more equity, which would dilute current shareholders.

KaizenInvestor@Kaizen_Investor

Appreciate your take on $TE. I believe the total solar energy sector is still undervalued at the moment as the technology is improving at a rapid level. $TE is a company that could massively benefit from the improving technology. They are doing a lot of things right imo, however I did not buy any shares yet. During Q3 earnings call they promised a lot of things for Q4 (G1 Dallas ramp-up, record quarterly sales, construction start in Austin,…) and the stock started pumping. This is not a moment to buy imo, the stock has jumped 100% mostly on promises. I’ll keep following them closely and might start a position soon.

English

@flyfishing2020 @EndicottInvests I’m done 50% and I hold EOSE. Unlucky or I’m an idiot

English

@EndicottInvests I cut my losses this morning. Down 30% on my position.

English

$TE management said they would do do more revenue in Q4 than they did in the previous 3 quarters combined.

That number should have been $398 M+

It was $358 M

I may just cut my losses here

English

Didn’t look deeply but my quick $TE earnings take.

Biggest red flag isn’t the EPS.

It is that management called for +$410M in the last earnings call

“Larger than our first 3 quarters total”

They hit $358M. They missed their own revenue guidance from 3mo ago by 10-15%.

English

English

English

BREAKING: President Trump is interested in calling on Arab countries to "pay for the cost of the Iran War," per White House officials.

President Trump will soon have more to say on the topic, according to the White House.

English

@SixSigmaCapital @amitisinvesting @KobeissiLetter Why is there an escalation everytime we get close to resolution and who is responsible for the escalation?

English

@amitisinvesting @KobeissiLetter trying for an off ramp for a while now. But any time gets close there is an escalation.

Nothing would surprise me here even a ground invasion imminently

English

@thejefflutz You should be careful confirmation bias Jeff. It impacts your credibility

English

Be careful where you get news from. Always triangulate sources and confirmation of anything significant

Ryan Saavedra@RyanSaavedra

All of this is a lie, so naturally Megyn Kelly promotes it. The U.S./Israel did not bomb some drinking "water source". They bombed a heavy-water facility, which has NOTHING to do with drinking water. Heavy water is water in which the hydrogen atoms are mostly with deuterium, a heavier form of hydrogen. It is used in nuclear facilities. Mario Nawfal is a liar. He intentionally spreads disinformation.

English

Long-term investors shouldn’t be concerned at all.

The fundamentals of $ASTS, $NBIS, $ONDS, $RKLB, and $KRKNF haven’t changed.

These current dips, and any upcoming ones, are buying opportunities.

The only area to be cautious with is leverage, margin, and options, that’s where I would consider trimming or closing positions.

I also derisked and sold my $RKLB margins that I bought on Friday (still own my core position).

Stay safe out there, we’ll continue to ride the ups and downs.

-RM

English

Update:

$SPX continues to show a throw over on the monthly timeframe and head for a 4 year cycle low

Camel Finance YT ⚡️@camelfinance

Update: We have seen the beginning of the throwover

English

@Kaizen_Investor Interesting. Thanks for sharing. I did quite well with HIMS last year and reduced my position before the latest Novo Nordisk drama. I got lucky with that one but not with many of my other positions. Thanks again

English

I'm currently at 20% cash, my highest cash position ever. It's not because I sold, but mainly because I haven't added extra cash in a while.

Starting from next week, I will start to use this cash again. I'm still considering which positions I will strengthen.

I probably won't buy the $IREN dip.

$IREN is currently 6% of my portfolio and I'm down 20% on the position. I'm still bullish long-term but I don't feel that this is the moment to buy the dip.

I feel that the market is still de-risking. Pre-revenue stocks like $OKLO have dropped 71% from the highs.

In industries like datacenters or space, the safer stocks are currently outperforming the market. For space, the positive free cash flow of $PL is giving them the edge. In the datacenter environment, $NBIS is clearly outperforming.

IREN's business model makes that they are the high risk - high reward play in the datacenter industry. To put it simply, they buy the $NVDA GPUs and lend them. So, IREN is not only providing the power, they are providing the hardware as well. Other business models, only provide power.

This makes that $IREN needs more cash than other companies do in the space. The $6b ATM is a logical consequence.

I don't agree that the $6b ATM is just "noise". I also don't agree that this is the end. I know that they only issued the option to activate the $6b ATM, but I don't see why you would issue the option without confirming it.

They won't activate this yet though. They just bought the newest Nvidia GPUs without the ATM. These GPUs will be used to attract a new hyperscaler deal. This new deal will bring more cash but, it will be paid in multiple steps.

So, I believe the activation will only happen after $IREN announces a new deal and need more cash to buy more GPU's to attract another deal. The first new deal should push the stock higher and make the ATM less impactful than it would be today.

An ATM is never completely noise though. Noise does not impact the balance sheet, an ATM does. In a market where the key theme is de-risking, a company where the Sword of Damocles is hanging over their head, is probably not the best choice now.

Might add some more when the broader market shift changes, but happy with my position at the moment.

KaizenInvestor@Kaizen_Investor

The ATM trend continues: Following $IREN's massive $6B ATM offering filing, $AAOI has followed suit, filing for its own $250M ATM. Do you know what an ATM actually is, and why it should concern you as a shareholder? Let me explain An At-The-Market (ATM) offering is a mechanism a publicly traded company uses to raise cash by creating new shares of stock and selling them directly into the open market at the current trading price. Imagine a company that owns a glass safe. In the safe is exactly $10. The company has 10 shares at the moment, all trading at $1. If you own 1 share, you have the right to 10% of what is in the vault (so, $1). It is an open market, so everyone can see what is in the safe. The company now wants to do an ATM of $5, which means they will be looking for 5 new shareholders to put $1 extra in the safe. If 5 new shareholders put an extra $5 in the safe, the safe will be worth $15 and there are now 15 shares. Still all worth $1. You now own 6.67% of a $15 company instead of 10% of a $10 company. So, if the math balances perfectly, why does the stock price almost always drop? 1. True, for the first part of the explanation we can stay with our virtual safe company. Why would a person pay $1 to get a $1 share in return? There might be a risk that the safe gets stolen. He wants a return. So to convince new investors, you will probably have to sell the new shares at $0.95. This has an immediate negative impact on the existing shareholders. The more shareholders you need to find, the lower the convincing price will become. When the price drops, existing shareholders might want to sell as well. This can become a negative spiral. 2. Another immediate impact is that the EPS will drop. Let's say that after the money is 1 year in the safe, it will return $0.1. So in the beginning the $10 will return $1 each year. Every investor will get $0.1 and the EPS will be 0.1. Now there is $15 in the safe, but the last $5 will not return money for another year. The $1 realized profit will now have to be divided over 15 shares. The EPS will automatically drop to 0.067. 3. For the final negative part, we need to leave the safe example. In a real company, the value is different for every investor. The share price is a constant battle between supply and demand. With an ATM, the supply obviously increases while the demand might not. The demand could increase as well, as investors might think that the board might do great things with the new money. But when the ATM is big, the pressure of the constant new supply might be overwhelming. Conclusion So, the share price certainly does not have to come down with a small ATM. If investors trust the company to achieve high returns with the fresh money, the ATM might be a great decision. But the 3 consequences explained here will put constant pressure on that stock price. Convincing new shareholders, a lower EPS and a constant new supply of shares might be costly for existing shareholders.

English

Psyllium husk is a safe plant fiber.

Studies show it lowers LDL cholesterol and improves blood sugar. It bulks up poop and feeds good gut bacteria as a prebiotic.

It slows (doesn't block) some nutrients so they absorb fully later and in human studies found almost no real drop in calcium or minerals at normal doses.

Take it 2 hrs from meds/meals + drink water and you’re fine.

A good amount of evidence to back up its efficacy.

English

Oh boy.. here we go (again)... a supplement that blocks nutrient absorption, requires excessive water to avoid intestinal obstruction, causes allergic reactions in some people, and acts as a laxative... and this is your daily health hack? Your gut doesn't need industrial seed husk to be "regular." It needs functioning digestive enzyme and bile flow, a healthy microbiome, and food that your digestive system actually recognizes. If you need a bulk-forming laxative to have a bowel movement, the question isn't "which fiber supplement?" It's "why has my gut stopped doing its job?" Fix the terrain and stop patching it with fcking overly-hyped plant husks.

Dan Go@CoachDanGo

I add this to my Greek Yogurt breakfast every day. It's called psyllium husk and it's one of the most underrated supplements on the planet. Psyllium husk is a type of fiber made from the husks of the plant called the Plantago ovata seeds. One of the benefits is improved digestive health. Psyllium is a prebiotic, which is needed for a healthy gut. It is also a bulk forming laxative, which means it soaks up in your gut. This can make bowel movements easier without making you fart. It's been shown to help people who suffer from irritable bowel syndrome. It's also been shown to lower cholesterol levels with very few side effects, which can also improve your heart health. Putting this in my shakes helps me stay regular, improves my gut health, and makes the shake fill me up more. Things to consider: When using psyllium husk make sure to add a lot of water as it is bulk forming, which can affect your intestines. Also, a small portion of people can have allergic reactions to psyllium. I would also take this separate from a greens powder as it has been shown to block the absorption of nutrients. I prefer to use psyllium husk flakes instead of the powder as I find the consistency much better. I take 5-7 grams once a day. Have you ever used psyllium husk or are considering adding it? Let me know in the comments.

English

I think the developments over the weekend are really bad. Two additional months in the war and the closure of the Strait of Hormuz could trigger a global economic crisis. I don’t think we’ll see the S&P 500 back in the 6000 range for months, maybe even years.

I still can’t believe Trump would allow thousands of U.S. soldiers to die in a war with Iran, but at this point it feels like he’s lost his mind. His recent speeches say it all, he seems capable of anything now.

If there isn’t a peace deal soon, I think we’re heading into a nasty bear market. The market feels like it’s at a top right now, not near a bottom.

The U.S. may have just crashed the global economy over a meaningless war.

English

@ideas_adrian @Pericleslealpha @EmmonsNick24458 @AwakenWithJP Medical technology is available to the everyday American!? Are you sure?? 🤣

English

@Pericleslealpha @EmmonsNick24458 @AwakenWithJP Jews also contributed to the U.S. economy and medical technology that is available to the everyday American.

What’s your point?

Your birthday is indeed a problem.

English

Supersleuth retweetledi

USA x Japanese Twitter all over the feed:

The fusion nobody expected.

English

NYC Friday Sunset.

This week’s blood sacrifice in the market stained the sky.

Portfolio Update tomorrow, spoiler alert.

It’s down.

English