Matt @ Meritum

51 posts

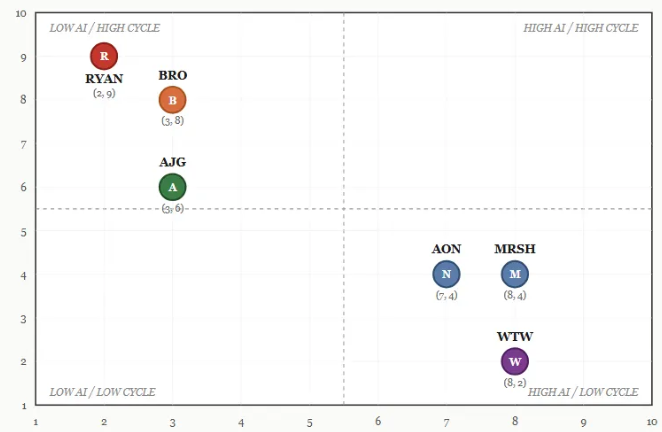

New post today in insurance brokers: "Which horse to pick" - combines our takes on Cycle + AI risk with an overlay of management quality, M&A capabilities and broader business quality (excuse the AI-assisted graph). $AJG $RYAN $BRO $AON $MRSH $WTW - link in bio & below.

English

@aerockrose Do binary search for 3 rounds, then always assume he would think adversarially and go to margins of probabiliyy space (i.e. no 57/58).

If you still havent hit by last free guess, stop playing. He never stipulated you have to finish the game.

English

Steve Ballmer reveals the interview test Microsoft used to separate problem-solvers from gamblers:

"I'm thinking of a number between 1 and 100. First guess, I give you $5. Then $4, $3, $2, $1. After that, you pay me."

"There are far more numbers on which you lose than win."

English

We published part 3 of our insurance broker writeup on the stack today. Cycle risk in focus, for both admitted + E&S. $AJG $BRO $RYAN $WTW $AON $MRSH

We go through recent pricing data on renewals, E&S market dynamics, casualty vs property and how the earnings outlook is hit.

English

Today we released our 2nd of four articles on insurance brokers ($AJG $BRO $WTW $AON $MRSH $RYAN) -- focused on AI-risk.

Steel-man is that brokers live on information asymmetry and LLMs collapse this - but we have 4-6 reasons to believe this won't be so.

English

@ToffCap $RELX --> Cheap and growth inflection ahead on relevance of data assets + increase in digital fraud.

$AJG --> Will grow EPS +50% next 3-4 years, and trades 15x NTM P/E.

$CDW --> Bombed out after todays okay earnings. Peak depression on mediocre results.

English

$CDW - open Q - "ugh, why do I own this shit? Christine is continually unable to manage costs" - down 20% - "fuck, can't sell it this cheaply"

Huge overreaction, but pretty natural since no natural ownership... no growth for compounderbros, not cheap enough for value-guys.

English

Meltdown in insurance brokers exemplified by $BRO NTM P/E relative to $SPY P/E over the last 20 years:

English

1Y ago to today on NTM P/E:

$BRO 26x --> 12,6x (5Y mean = 23x)

$AJG 28x --> 15x (5Y mean = 24x)

$WTW 18x --> 13x (5Y mean = 17x)

$AON 20x --> 16x (5Y mean = 20x)

$MRSH 23x --> 16x (5Y mean = 22x)

So $BRO went from "top tier" to $WTW-level + AJG rerated from premium->normal

English

Today we released part 1 of a primer on insurance distribution - including $AJG $AON $MRSH $BRO $RYAN $WTW.

Covers market layers (admitted / E&S), reasons for intermediation, recent sell-off, and a few more things. pt 2 = AI, pt 3 = soft market risk.

See link below.

English

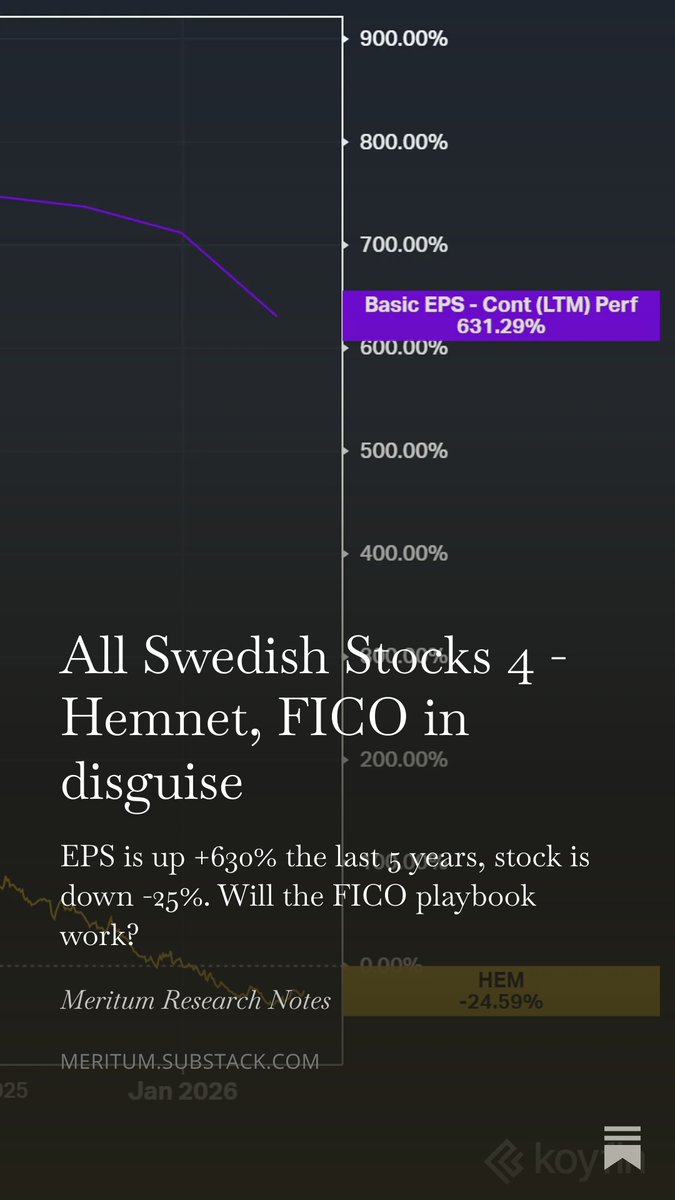

Read our latest piece on $HEM.st -- a Swedish $FICO in disguise.

Over last 5 years EPS is up +630% due to aggressive price increases, but the stock is down 25% over competition fears and crazy starting multiples. Management is executing very well on increasing their moat.

English

@fcfyplusg IMO risks on click-to-cancel and AI-automated savings are worth considering, especially given their debt-fuelled buyback model (meritum.substack.com/p/memo-planet-…)

English

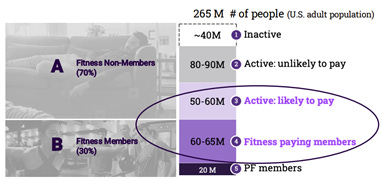

We cover Planet Fitness on our substack in todays memo ($PLNT).

Strong unit economics, but impending churn risk from easier cancellations & debt-funded buybacks makes the equity more fragile than one would expect from just looking at the core business model.

Read more below

English