Mr T

16 posts

@MrTprh Bearish. Bullish would be PL7737 having IND worthy data and actually submitting IND applications. Their most wanted asset got sacked for potentially something better one more year down the line. Stock will probably sink to 10$ in the next 6 months with no other news. $PTN

English

🚨 Weekly Watchlist: Phase 3 Readouts are coming before 2Q ends.

$ADCT, $PTN, and $DFTX are all approaching clinical data. 📈🧬

🔹 $ADCT: LOTUS-5 data

🔹 $PTN: ED Synergistic data

🔹 $DFTX: MDD Phase 3 data

Watch now: youtube.com/shorts/GWl7Egy… 📺

Weekly Watchlist:

biopharmcatalyst.com/news/2026/biop…

Track the countdown at BioPharmCatalyst.com 📈

#Biotech #Stocks #Trading #ADCT #PTN #DFTX #BioPharmCatalyst

YouTube

English

Call it nitpicking because in a way it is, but also because transparency from management and investor relations has been and remains trash...but you should at least have the correct symbol on your website $PTN

IND coming up which should coincide with the next round of dilution

English

The Weekly 🌱

New: $anl , $tern , $cmps

Increased: $abvx , $nktr

Unchanged: $nxtc , $ovid , $slno , $cntx , $pasg , $dawn , $lqda , $rytm

Decreased:

Closed: $crvs (s) , $apge (s) , $asnd , $ptn , $cogt

Feels like forever since the last weekly but nice to get back to work. The past week felt like a movie but important to not get distracted. Long weekend ahead with markets being closed on Monday so will use this time to get back up to speed and work on a few new ideas. $iron CRL ngl was a surprise but I’m glad I passed on it even though there were rumours that approval was a foregone conclusion. $goss and $ocul should be next week, I am going to wait for data to act. If you remember $aplt CRL there was ample chance to short it to 0 after, so if $goss is a fail, you’d probably still be able to short. I’m just not present enough on my desk to have conviction to press the short on these two binaries.

My last weekly commentary $gpcr view turned out to be right but again passed on the opportunity to actually short.

$abvx I’ve been adding, it’s been trading well and I just think since October there is just too much smoke to assume it’s a nothing burger. I covered my 100p sells for a huge profit and then sold another layer of 120 and 125s puts.

$anl is a $50 stock, its time will come. Still adamant I think it’ll be the best performing biotech co in 2026. Already up what 600% ytd.

I’m back in $tern , should’ve never left, BP gonna come for the CML asset only a matter of time.

$nktr I’m a buyer on any weakness. It’s significantly derisked. We got more comfortable on safety too. Hearing some big names in the offering, so that will provide stability and they’ll help mgmt navigate through the next phase. $nktr over the past few years have lacked that. Bvf / tcg didn’t really provide that support. Think the litigation overhang clears in 6 months and I wouldn’t be surprised if it gets scooped up before YE.

$nxtc $pasg $cntx all speculative plays even if 1 of them works , should cover the possible losses for the other two if they don’t comfortably. A good r/r small cap bucket.

$dawn and $Lqda my commercial names with good recent prints. $Lqda could be a $VRNA story esp if the legal overhang clears sometime soon.

Also idk why $iron is holding up here if should be lower imho should be sub 50. Anyone buying this here I would suggest to read the CRL notes again.

$slno I’ll give it another few weeks, but I’m losing patience. Same with $rytm

Anyways hope everyone has a top weekend, hopefully on Tuesday we get some M&A and all the anticipated Feb readouts. Also hope $ocul disappoints, they played too many games.

Seedy 🌱

English

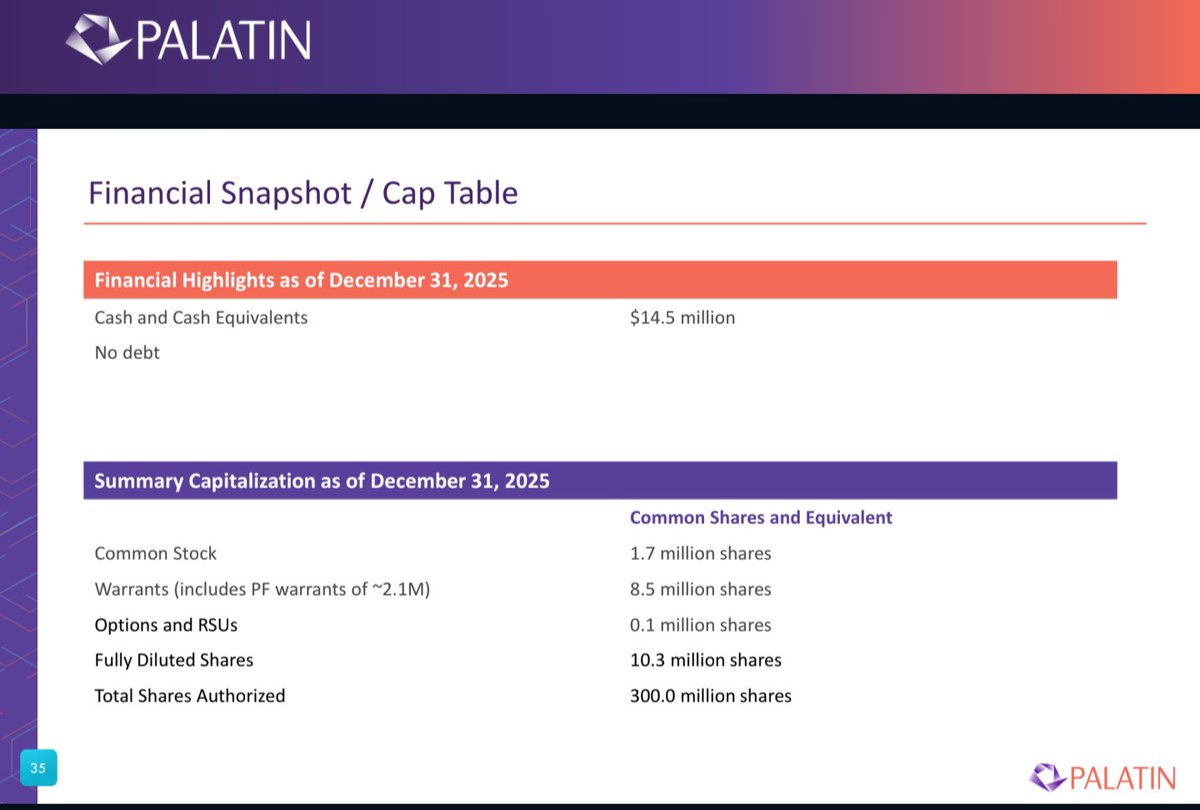

$ptn has a market cap of ~$150m fd compared to rhytms ~$7,4b. $ptn has a huge upside and they will definitely take a big size of that $5-7b market share with their new oral asset pl7737.

singhlosophy@singhlosophy

For context, $PTN at $100 is only a $200 million market cap. Hypothalamic Obesity is projected to be a $5-7 billion market space by 2033. $RYTM won't be taking 100% of that market share. Worth owning both for this target indication. x.com/singhlosophy/s…

English

So that entire $PTN move from 11/21 to 12/16 was an orchestrated pump and dump. Absolutely incredible how many scumbags there are on this app.

Using folks on here for exit liquidity is such a low life thing to do. "Due diligence" for a 3 week move is a cloak of lies.

I'm holding

English

@seedy19tron What’s your take on Palatins asset pl8177? P2 poc data in UC. Safe oral therapy, a non-immunosuppressive alternative, first-in-class mechanism of action. Will they outlicense it and to whom?

English

$lly need to catch up to $abbv and $jnj , a post ph3 asset would seem to be the most logical decision right?

Speaking of $abbv , I actually never addressed their comments, but to me , I haven’t been around long but when BP is indifferent usually means that the asset is poor or not worth of any commentary at all. $abbv shit talking suggests that they probably vetted the asset and recognized its threat to Rinvoq/Skyrizi. And since they couldn’t buy it themselves due to FTC concerns, they decided to try to kill it in the cradle with negative sentiment. Look if $abbv is worried enough to talk it down, the asset is real.

Anyways just to recap , hope you understand that the hard part is already done. $lly already at an executive level decided oral IBD is the way to go, thats already established. They’re “IN” , and to quote my friend “The friction to buy $abvx is significantly lower than the friction to pivot to a new therapeutic area entirely.” So the actual paying up and making a move seems like the less stressful bit. Which gets us to my discovery of the $lly plane.. to me their presence in the city where $abvx HQ is, a city they almost never otherwise visit , moves the probability from $abvx being a possible strategic fit to imminent deal. How imminent? Idk, probably the guys spamming the calls are better folk to tell ask.

Anyways, again so sorry for more $abvx spam but I just needed to remind everyone that Omvoh is a "me-too" biologic in a crowded room. $morf and $dice were failed bets on the future. $abvx is the pay up solution for $lly. It is the ONLY remaining independent + late stage + oral IBD asset of quality.

$pfe $sny $jnj others that could be in the reckoning. One day guess we’ll know for sure. For tonight , goodnight and let’s see what next week brings. 2/2

English

*Important Weekend Read*

Leaving you with one final piece on the rumours around $abvx and $lly . I’m terribly sorry I know a lot of folk are irked and the BioX experience has not been great due to all the $abvx commentary floating around. But it is important to me for all those interested to understand why $lly x $abvx seems like the perfect fit when greater context is provided.

You see $lly ‘s alleged pursuit of $abvx is not just about adding an asset it is about correcting a strategic deficit. We know $lly execs decided that they were going to get a footing in the oral IBD space, this was evident with the two high profile swings and misses with earlier stage assets $morf and $dice . What those flops have done is that they’ve pushed one of the most successful biotech companies of our time to pay up for certainty. $abvx ‘s Obe offers a derisked Ph III validated oral asset that plugs immediately into $lly existing commercial infrastructure solving the traction issues currently facing Omvoh. Whilst also providing the certainty they are looking for.

I was chatting to a friend over dinner who’s seen deals come together and he explained to me how BP acquisitions of $1B+ don't happen casually.

I agreed with his observation tbh, like these deals are the result of deep strategic convictions that come straight from the senior leadership.

When you look at the $morf (oral integrin) and $dice (oral IL17) acquisitions for $lly they serve as a definitive tell. Definitive tell for what, well you see these were not opportunistic buys they were targeted moves to secure a foothold in oral IBD.

To reiterate what I stated in the intro the fact that both deals failed to yield a viable commercial product does not negate the strategy, in fact it intensifies the urgency. $lly has already convinced itself that the future of IBD is oral. Walking away now would be an admission of strategic defeat not just clinical failure. Which for them considering how incredible their growth as a company has been does not seem like something they would do.

And to add to that, BP when they decide they want something, they don’t care if they have to overpay , take $gild $immu as an example. $gild decided that they had to become an ADC player and regardless of how it panned out, they paid up, $lly is now in a position where they feel like they’ve got to go for a late stage asset to become an oral IBD player. The decision has already been made imo they just need the right vehicle. Which has to be Obe.

You see $lly ‘s earlier purchases with the intention to enter the space were cheap relative to the potential payoff but they were high on technical risk. $morf failure (recent) was particularly stinging because it targeted the same mechanism (integrin) as $tak Entyvio but in oral form considered a holy grail for IBD.

Its simple when a pharma giant fails twice with early stage/risky tech the standard pivot is to stop gambling on biology and start buying data. $abvx is no longer a concept stock it took folk a long time to come around on the moa and with +ive Phase III induction data the biology risk is largely removed.

Then on the commercial side we know that $lly already has the sales force and commercial infrastructure built for Omvoh. Currently that infrastructure is underutilized because Omvoh is struggling to gain traction against established biologics. When you add Obe to the mix, that same sales bag instantly increases the ROI of their entire IBD commercial unit.

And I know everyone keeps saying novel moa over and over again but for the generalists let me elaborate so you understand what that actually means. See Obe has a novel mechanism of action (miR 124 upregulation) distinct from JAK inhibitors ( $abbv Rinvoq) and S1P modulators ( $pfe Velsipity, $bmy Zeposia). This allows $lly to market it without fighting the exact same safety/class battles as the competition. 1/2

English

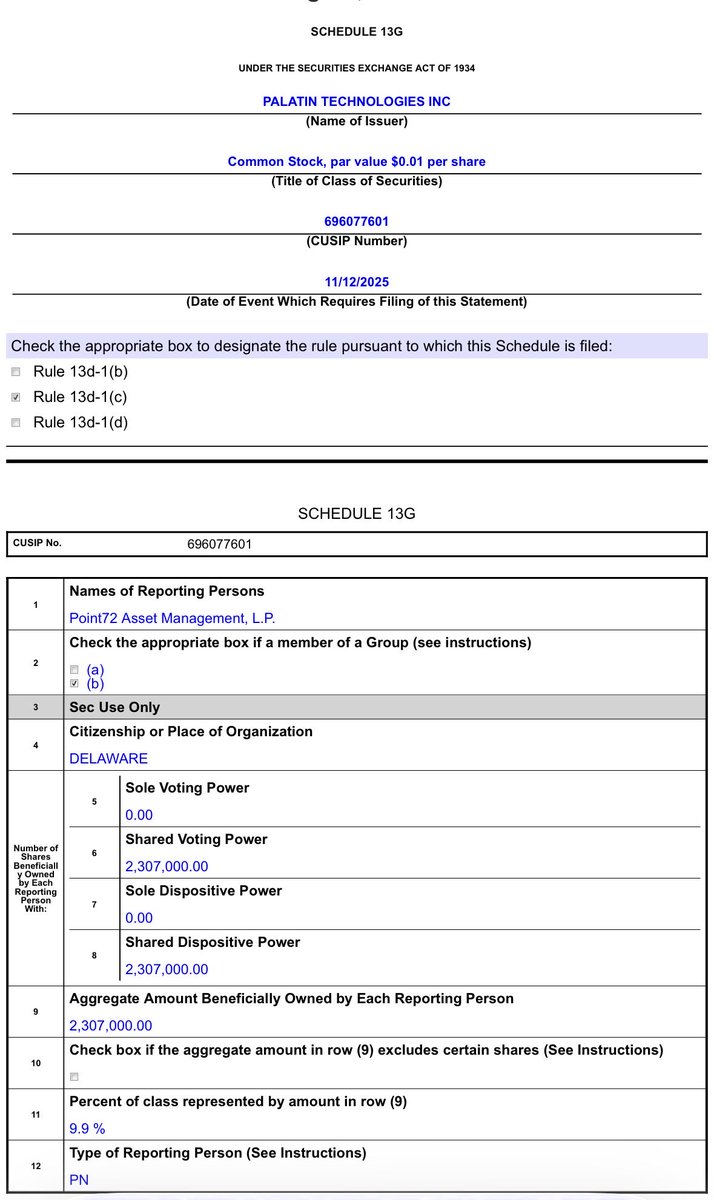

$PTN 13G Janus Henderson 9.99% stake

This story is really starting to come together nicely.

Literally only a $45 million market cap.

English

@seedy19tron $ptn may be one of the most asymmetric risk/reward opportunities in the entire small-cap biotech space right now.

English

The Weekly

New: $nvo

Increased: $abvx , $slno , $ovid , $cmps , $cogt , $nxtc , $ptn , $nktr

Unchanged: $rytm , $agio , $capr (s) , $celc

Decreased: $dawn , $crbp , $tern

Closed: $pali , $inbx (s) , $avtx

Bittersweet week, low on motivation writing this but hoping this will help someone out there make a more informed decision.

ATHs and 52w high galore over the past week across many names. The mood is within healthcare equities is euphoric. I covered my $inbx short, I think the way the market is going I should not be battling the trend at least not for now. $inbx still doesn’t pass the smell test but I was wrong with the timing and judgement of the setup, and perhaps too stubborn. Did I give up too soon? Perhaps, but I’ll be rooting for it to return to fair value in the 20s/30s

$slno making a comeback, which is refreshing to see, hopefully it settles in the mid to high 50s , and the next few weeks script data continue to trend upwards.

$nvo dip buy working , now I know big pharma trade slightly differently to smids (very different type of investor bases involved and obv huge pipelines + much more) that seem to be my forte, but despite $nvo struggles it felt like I was buying close to the lows. I added further into the strength today. I tell myself that I want to top tick tickers moving up in strength , but in reality what I’m doing is moving to greener pastures with a strong breeze behind my back i.e momentum and in this environment it’s a highly profitable strategy. This applied to most my long positions this week. $cmps on the other hand has been a bit of a laggard , but so was $ovid for weeks and now it’s finally getting the love it deserves. Not long till $cmps starts to get its fair share of love.

The timing and the way you all received the $nktr AA deep dive could not have been any better. Citi upgrade today too is a huge deal. I have to credit you all for pushing me to get the AA deep dive out and out at a good time where the stock was hovering at ideal r/r levels.

$capr still no data. My problem with $capr other than their drug being a dud is the CEO. I think in any walk of life , the person that acts nice to your face and simultaneously is plotting to scam you behind your back, is the worst type of person. That’s the $capr ceo. Act all sweet and innocent, but shaft investors at every calling. I ‘hope’ to see them fail.

Trimmed $dawn , I bought the dip post $mrsn but not sure what the next leg up would be apart from just moving with the market. Same with $crbp. $tern I trimmed purely because even if they have the data to suggest they can own the whole CML space, just on a risk basis, felt it was closer to fair value for now.

Speaking of dip buys, $agio turnaround has been wonderful to sit through. I did although sell 30c for Dec. Don’t think prior to the PDUFA it should be in the mid 30s, possibly after. Not far though.

I closed $pali because seems like for now it’s purely a $abvx proxy trade. So since I’m so heavily concentrated in $abvx , felt okay putting $pali aside for now. I also did add to other trades like $nxtc / $ptn . Both could be multibaggers imho.

I will return to $avtx and $zura in the new year, for now I felt like it was prudent the close the rest of the position that I had been trimming anyways in $avtx

Lastly, $abvx , ATHs traded as high as $132 PM today. I have started taking some covered calls as of today. Will continue to chip away , for December in case there is no deal or announcement. The premium on them is pretty jacked.

Anyway, may your Thanksgiving be full of loud laughter and lasting memories. I would also like to use this opportunity to pass my gratitude to the whole community and everyone that reads/follows The Weekly. I garner a ton of motivation knowing I am able to help the community with these.

Happy Thanksgiving 🌱

English

$PTNT Degraded to #OTC not dead.

If anything, it has held extremely well on OTC, I am still green. Means big backers are not leaving? It is not like that company does not have valuable assets

#OTC #stocks #biotech #StocksInFocus #StocksToBuy #StocksToTrade #TradingOpportunity

English