Mr. Tinker@xEBITDA

Trigger warning: Long post after digesting the ER.

I think the market is still misunderstanding what the $EOSE/Cerberus JV actually represents.

Most people are analyzing this like a normal strategic investment where Cerberus simply decided to back Eos. That’s not really the important part. The important part is that this may be one of the first serious attempts to solve the actual bottleneck in long-duration energy storage: project bankability.

The issue with LDES was never simply demand. Everyone already understands the need for dispatchable power, AI/datacenter load balancing, grid resiliency and renewable integration. The real problem was always financing, insurance, guarantees, underwriting and project structuring.

Utilities and hyperscalers do not want to coordinate a battery vendor, an insurer, a project finance group, EPC contractors, asset managers, software operators, and energy market specialists for every deployment. They want turnkey infrastructure with predictable economics and credible counterparties standing behind it.

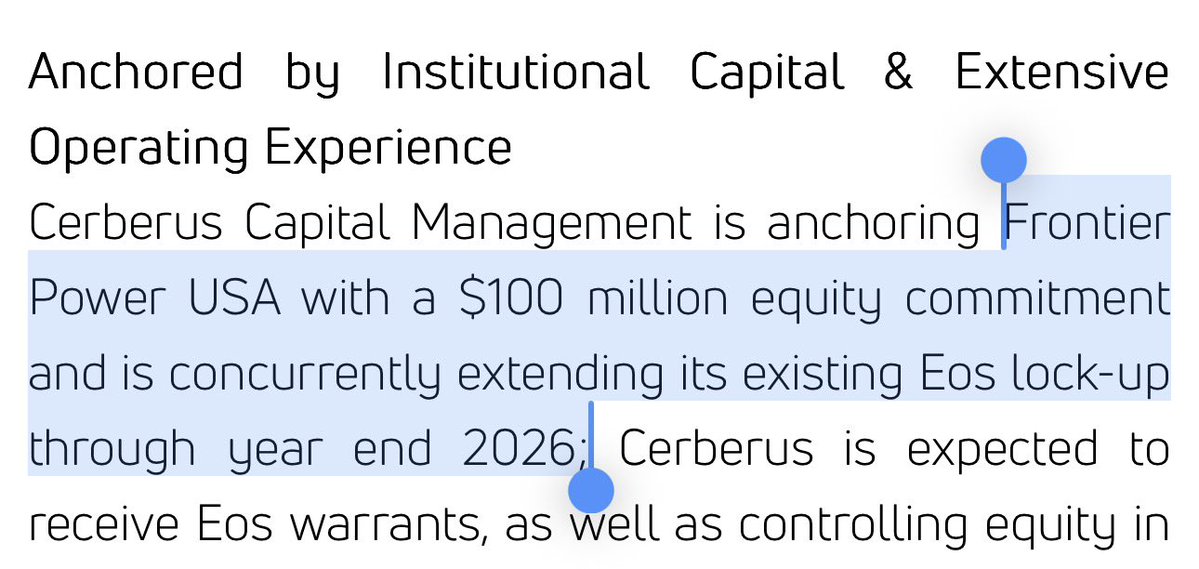

That is what Frontier Power USA appears designed to become. The JV effectively creates a vertically integrated deployment and financing platform around energy storage projects. Cerberus brings institutional capital, infrastructure expertise and project structuring capabilities. Ariel Green brings long-duration performance insurance and underwriting capacity. Eos supplies the initial underlying technology stack and manufacturing platform.

Together, that creates something much more important than simply “a battery company.” It creates a framework where a datacenter operator or utility can potentially make one phone call and receive: the batteries, financing, insurance, guarantees, project management, operational support, and assistance monetizing various energy market revenue streams. That dramatically lowers procurement friction.

The most important piece here may actually be the insurance and financing framework itself as both @AdamLevey7 and @JigarShahDC can probably attest to. Battery projects are difficult to finance because lenders fear technology underperformance and uncertain long-duration cash flows. Most lenders are not battery experts. They care about whether the project performs as promised and whether revenue streams are reliable enough to support institutional debt financing. By wrapping projects with standardized underwriting structures, long-duration insurance coverage and institutional financing frameworks, Frontier potentially lowers one of the biggest barriers preventing large-scale LDES deployment.

Infrastructure markets run on trust and underwriting confidence far more than chemistry debates. And this is where I think many investors are still missing the bigger picture. $EOSE does not necessarily need to “win the battery wars” in a winner-take-all outcome to become extremely successful. The LDES market itself may become enormous because the underlying demand drivers are structural:

- AI power demand,

- renewable intermittency,

- transmission constraints,

- resiliency requirements,

- electrification,

- and grid modernization.

It is naive to think $EOSE or any other company will be "the one". Multiple technologies will likely coexist.

What matters is whether $EOSE secures a durable position inside the financing and deployment ecosystem as the industry scales. The Cerberus JV potentially helps accomplish exactly that.

Before this deal, $EOSE was mostly viewed as:

“a speculative battery manufacturer.” After this deal, $EOSE starts looking more like “a foundational participant inside an emerging infrastructure financing platform.”

That distinction matters enormously. Battery hardware alone eventually commoditizes. Margins compress over time. But financing ecosystems, underwriting frameworks, institutional relationships, recurring project cash flows and deployment platforms create real moats.And ironically, one of the most interesting aspects of this structure is that Frontier itself may eventually become bigger than just $EOSE technology. As a reference, look at GE Finance, Siemens Finance, or any of the Automotive Fincos. These are enormous businesses by themselves.

Today, the platform is clearly centered around $EOSE. Frontier secured a 2 GWh reservation agreement tied to $EOSE manufacturing. Cerberus committed $100M of equity capital into Frontier. $EOSE plans to contribute approximately $150M via the rights offering. The Ariel Green insurance structure is specifically designed around $EOSE technology today.

But over time, if Frontier successfully institutionalizes the financing side of storage deployment, the platform itself could theoretically finance and deploy multiple technologies across the broader industry.

That possibility actually reinforces the thesis. Because it suggests the real moat may not ultimately be: “our battery chemistry is slightly better.”

The real moat may be: “we can actually get projects financed, insured, approved and deployed at scale.”

Disclaimer: Long $EOSE