OrangeGroveCapital

4.5K posts

OrangeGroveCapital

@OGCapital25

To God be the glory | Turned 80K to 1M in 4 years | Now hoping to build gen wealth | High-conviction, asymmetric picks only | I publish my process on Substack:

Katılım Temmuz 2025

294 Takip Edilen4.4K Takipçiler

Maybe consider that your days are short, perhaps a handful more decades at most, and all that you pursue is vanity and chasing after wind.

Consider that there is an eternal God who created all things and who sent his Son to die on the cross for your sins. Consider that if you confess your sins and repent to him, he will transform your desires and you will have eternal life.

Maybe take some time yourself off this platform to seek God, read the Bible, and to consider the truth of the universe.

Love you Erik.

English

@ShadyJosh5 must be good to know that Adjust EBITDA>0 in 2 quarters

English

The market seems to be using an Excel formula for $LMND

=IF(Adjusted EBIDTA<0,"SELL","BUY")

Time and math will take it's course here in my view

English

@PaperBagInvest I bought back in with the amount I trimmed @ $78.

English

These are the levels.

I didn't think anything crazily wrong with the report (but haven't had time to go through in detail).

If that's the case, I think $45 probably the lows (0.618 fib).

Need something catastrophically wrong - more bombing + fed hike + some reason opex is so high to visit 30.

English

Haven't had time to go through the report in detail, but I don't see any change in the thesis.

Fully back in $LMND after trimming at $78/79. Bought @ $49.

OrangeGroveCapital@OGCapital25

$LMND The $78 / $79 level is the 0.382 fib. Trimming some $LMND here hope to add lower.

English

@sheslee @TJTheWheelDeal That’s insane. Brave of you to admit.

Respect Lee!

English

@TJTheWheelDeal Been absolutely brutal.. I was sitting on a $80mm portfolio for about a hot second before watching it all fall to about $25-30mm again 🥲

English

I get a lot of shit for my drawdowns that I’m willing to take chasing the $100M dream.

If you’re so damn good, how’s your path to $100M coming along?!

Asking for a friend :))

English

Shared with Substack subscribers a full 10 days ago.

Stay safe out there friends.

Don’t fight the tape.

English

OrangeGroveCapital retweetledi

I’m more bubble boi than RJC, but with a nuance in that I am picking my pivot.

English

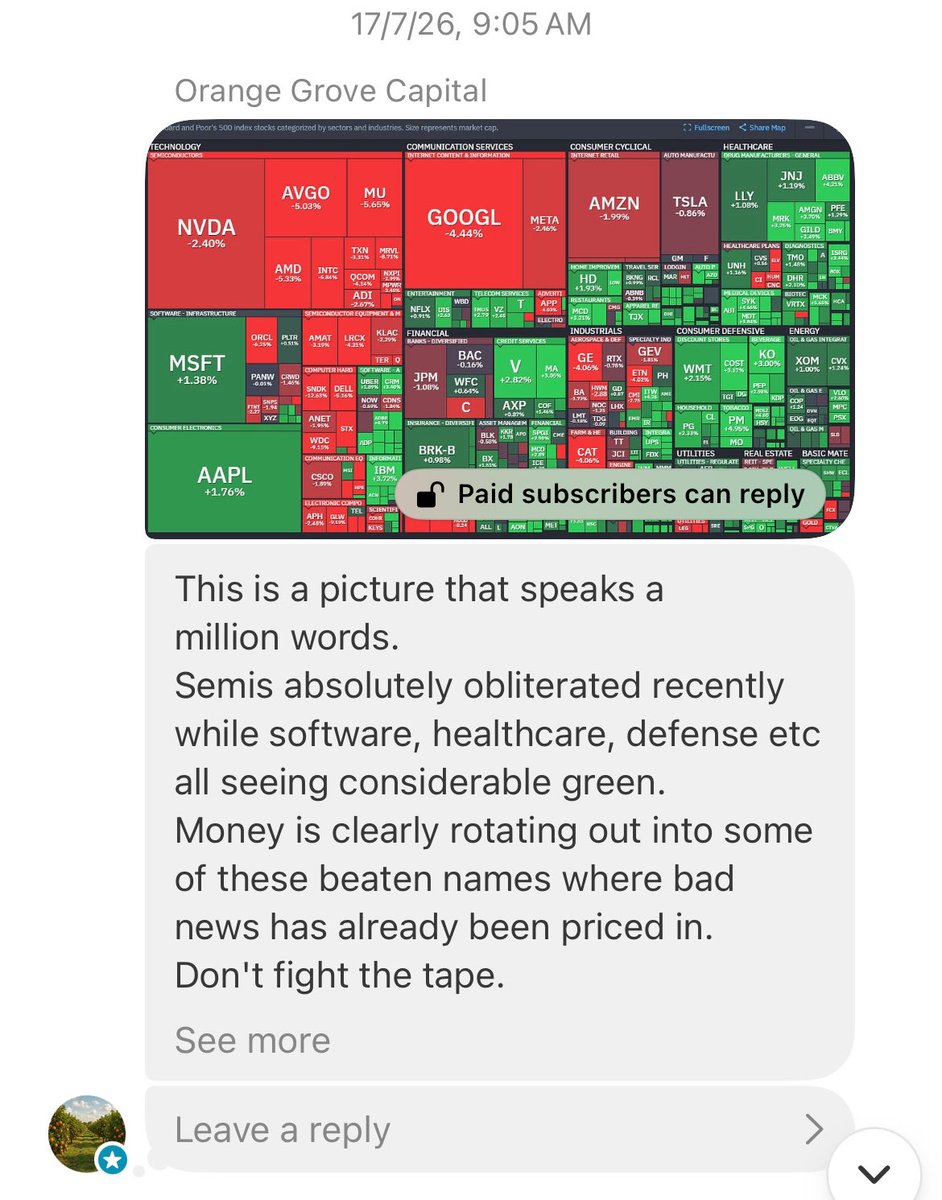

If only someone told you that capital was going to rotate from semis to quality 1 month ago …

OrangeGroveCapital@OGCapital25

English

OrangeGroveCapital retweetledi

I think it's quite important you read this.

I will bang on the drums until you realise that the memory run, while still has legs, is no longer the run to be in.

The article below discusses where you should look next.

OrangeGroveCapital@OGCapital25

Last Friday, on the back of a strong jobs report, the S&P fell by 2.7%, wiping out $1.8 trillion in market value and marking the index's worst single-day drop in eight months. To the extent that spooked any of you, I’ve spent the weekend preparing this article examining the state of the economy today and where I think we’re headed. It combines both technical and fundamental analysis to present what is I think a nuanced view of the economy today. I’ll spoil the conclusion for you: We’re not going to enter a bear market any time soon, but sector selection will be very, very important - I break it all down in the article. @ogcapital25/note/p-201548008?r=6j0pe2&utm_medium=ios&utm_source=notes-share-action" target="_blank" rel="nofollow noopener">substack.com/@ogcapital25/n…

English

Note to self:

- All in challenges

- 200% YTD screenshots

- Everyone and their moms making a Substack

Probably the top.

English

@Berlinergy @LIWEI_TWCapital It’s above my entry. But even if not $PENG is going to do just fine

English

@OGCapital25 @LIWEI_TWCapital Your entry recommendation now in the 50s - easy right ?

English

@FinnStockinger @TheBigBerbowski @JonkooTrades @ekroth @outliercapx @OInvests @LIWEI_TWCapital @rk8215 A real legend you are Finn! 🔥👊🏻

English

Great initiative by @TheBigBerbowski! 👏

I don't know everyone on this list, but the accounts I can wholeheartedly recommend are:

🔹 @JonkooTrades

🔹 @ekroth

🔹 @outliercapx

🔹 @OInvests

🔹 @LIWEI_TWCapital

🔹 @OGCapital25

I'd also add to the list:

🔹 @rk8215

🔹 @joedab12

🔹 @AnalysisOp

🔹 @chinoalemano

🔹 @superposition_V

I’m probably forgetting someone, but these are the first ones that came to mind!

Who else from the list should be on my radar?

Let me know below! 👇

TheBigBerbowski@TheBigBerbowski

Here are some fine accounts sub 10k followers which deserve more attention (in no particular order). Give them some love. @rmainvestmentsx @Double0Capital @yvesstocks @glocalinvestor @OInvests @Funmentalist @itsalasdairmann @JonkooTrades @napoleon21st @MirageWL8 @snmart @LandoInvests @PreIPOMedia @burak_finance @ekroth @LIWEI_TWCapital @jimmyinvest @AlphaOwlTrading @Raunav410657 @OGCapital25 @FrostByte123456 I have undoubtedly overlooked someone, so please accept my apologies in advance.

English