OnlyCFO

5.4K posts

OnlyCFO

@OnlyCFO

Finance stuff for tech companies. Sign up 👉 https://t.co/Yu5VD1YWTV

Cloud Katılım Eylül 2019

572 Takip Edilen32.2K Takipçiler

Wednesday! 👀

The most ambitious launch in @deel's history. It's reshaped the company from the ground up and is the biggest internal breakthrough we've had.

I can't wait for you to see it.

English

@EranBenHorin Debt will suffocate innovation

Which will lead to a lot of churn in 2026 (people go to the AI winners)

And then quick death spiral because of debt

English

OnlyCFO retweetledi

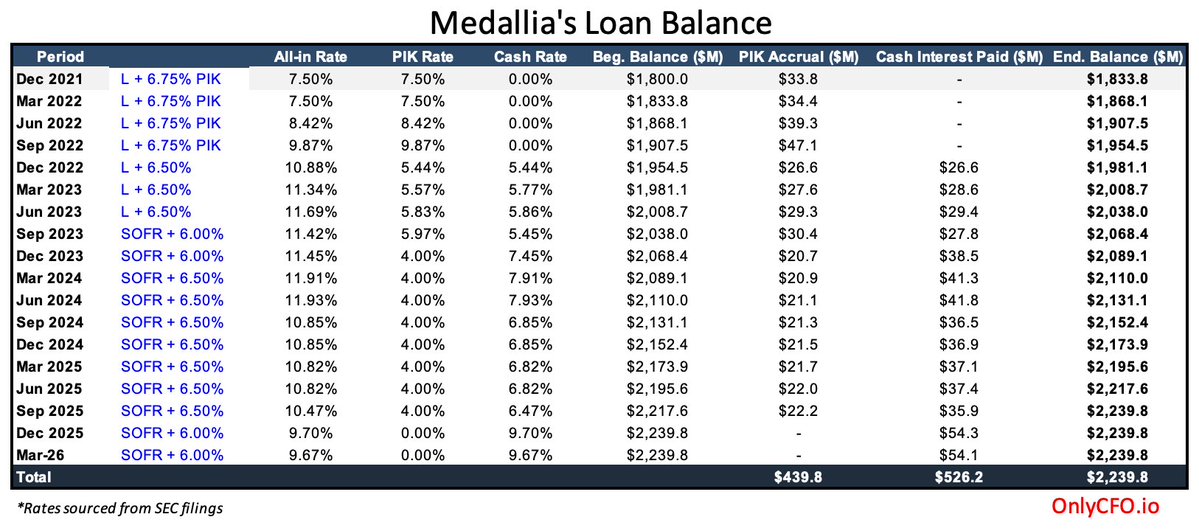

Thoma Bravo took $5B to $0 in just 5 years.

That’s the power of debt…doubled-edged sword

The PE playbook worked for a long time, but Medallia is the first of many more to come. And it’s bad news for all of us.

onlycfo.io/p/thoma-bravos…

English

@PrivCreditGuy Hard to get principal back if FCF is 50% short of the interest payments and terminal value is spiraling to zero tho…

English

@OnlyCFO I was being sarcastic on the zero; They can definitely keep harvesting cash flows and paying down debt but EBITDA is $200MM vs $2.8Bn of loans

English

The thumbnail below is some of my best work…

onlycfo.io/p/thoma-bravos…

English

@PrivCreditGuy I imagine they will get something right?

Will drain it for FCF at least even if they can’t sell it for parts later

English

@OnlyCFO Likely going to zero for the lenders too

PrivateCreditGuy@PrivCreditGuy

Why is Medallia marked at 60 cents on the dollar by $BCRED and $BXSL, yet Antares is marking at 84? $2.8Bn of debt, EBITDA is $200MM, implying leverage of ~14x for a plummeting software business yet Antares still marking their loan 30% above other investors? Just one example of how some of these (most) private credit fund NAVs are not reflective of true value

English

@ChairliftCap They should but I think most are thinking about it but using other metrics for it

English

@ChairliftCap Plenty of not very smart CFOs

But in fairness, very very few talk about ROIC in software

English

I once had a meeting with an, at the time, mid cap software CFO. I mentioned ROIC once in the meeting and he looked at me all confused and said 'what's that?'

English

Startups are hard

Personally:

- My cofounder walked out the door

- I spent all the money

- I had to sign at $750k note

- Our product failed at our top customer

- My VPS told my board I was incompetent

- My family didn't understand

- I went through recessions

Could have quit

English

@jasonlk For sure. Gross margin compression is just a side note that I think a lot of folks are thinking about on top of the bigger death spiral of churn and drop in win rates.

there are many 2nd/3rd order impacts that will cause the death spiral to be faster then most are modeling

English

I hear you. I mean most of the crappy pre-AI software we use probably has effectively 95%+ gross margins. We get zero help or support, and it costs nothing to host it (e.g. Marketo). So Marketo should keep us at any costs.

Captain Obvious but the general death spiral at the top line on renewals (net positive churn at renewal) to me is a much bigger deal than some gross margin compression

We will leave Marketo for an agentic solution at 1/10th the price. And it will be so, so much better

English

@OnlyCFO For sure, times are even more desperate than they look. Financials are backwards looking

But does dropping prices on a >renewal< really lower gross margins all that much?

English

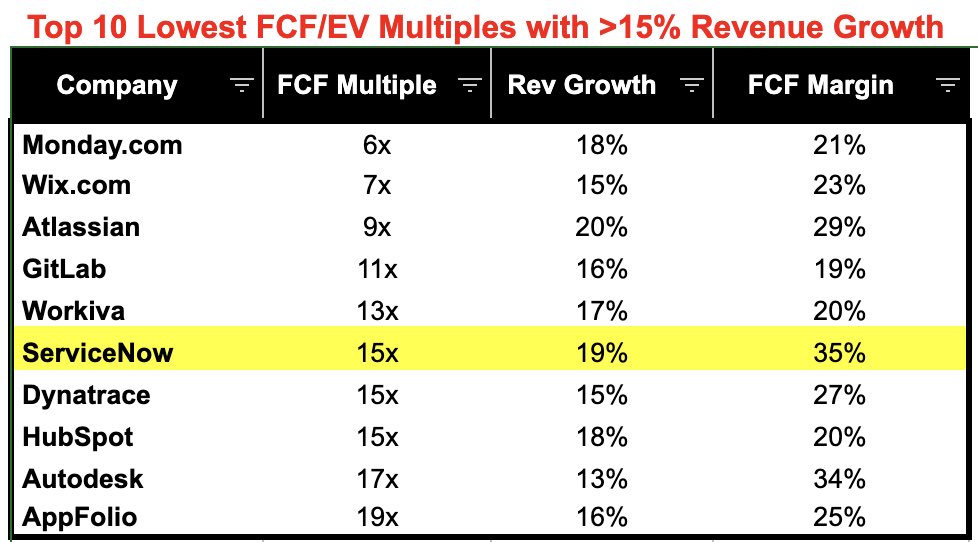

FCF multiples are the new revenue multiples

OnlyCFO@OnlyCFO

ServiceNow at its lowest FCF multiple ever.

English