Sabitlenmiş Tweet

A traditional nuclear plant is not expensive because the fuel is rare or the technology is exotic (it is however for SMR's). It is expensive because almost all of the cost is paid upfront, long before a single kilowatt hour is sold. You spend billions first, then wait years before revenue starts. During that time, capital is not idle. It accrues interest. i'll walk you trough it:

The metric that matters is WACC, the weighted average cost of capital. In simple terms, WACC is the minimum return investors demand to lend money or provide equity. The higher the perceived risk, the higher the WACC. Nuclear projects typically face much higher WACC than wind or solar, not because they produce worse power, but because the timeline is longer and the downside is asymmetric.

A wind farm might be built in 2 years. A nuclear plant often takes 10 years or more. Every extra year adds interest on top of interest. A 1 year delay does not just shift cash flows forward. It permanently raises the total cost of the project. This is why schedule risk dominates everything else.

To see how sensitive this really is, reduce the problem to 1 euro.

Assume 1 euro is invested today, at time 0. No revenue comes in until year 10, when the plant finally starts producing power.

At a 6% cost of capital, that 1 euro grows to about 1.79 euros by year 10. That is the minimum amount that must be recovered just to break even.

At a 9% cost of capital, that same 1 euro grows to about 2.37 euros over the same 10 years.

Nothing changed technically. Same project. Same build. Same output. Yet the required recovery is roughly 32% higher at 9% than at 6%, purely because interest compounded for longer.

Now add a 2 year delay.

Cash flow starts in year 12 instead of year 10. At 6%, the original euro now grows to about 2.01 euros. At 9%, it grows to roughly 2.81 euros.

The gap is no longer 32%. It is now about 40% higher for the exact same euro invested upfront.

This difference does not come from inefficiency or mismanagement. It comes from time. When construction is long and revenue is delayed, small increases in WACC and small delays in schedule compound into large differences in total cost. That is why a project that works on paper at 6% can become unfinanceable at 9% even if nothing goes wrong operationally.

Private capital understands this well. That is why traditional project finance rarely works for nuclear. Banks do not like assets that take a decade to complete, cannot be easily abandoned halfway, and face political and regulatory risk throughout construction. Without guarantees, investors either demand very high returns or walk away entirely.

Governments have tried to bridge this gap using contracts and guarantees. One approach is a long term fixed price contract for electricity. This removes market risk but not construction risk. Another approach is loan guarantees, where the state absorbs part of the downside if things go wrong. A more aggressive model allows investors to earn regulated returns during construction, reducing the period where capital earns nothing.

All of these tools have the same goal. Lower the effective WACC by shifting risk away from private investors. When this works, projects move forward. When it does not, projects stall, overrun, or collapse under their own financing costs.

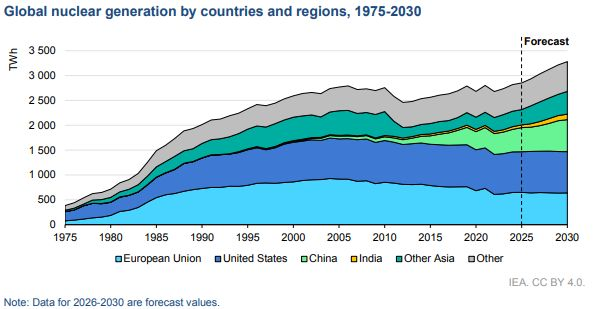

There is a second layer that is often overlooked. Fuel supply. New reactor designs increasingly depend on enriched uranium that is not widely available today. If investors are unsure whether fuel will be available at stable prices 10 years from now, they price that uncertainty into capital costs today. Fuel risk becomes financing risk.

This is why comparisons with wind and solar are misleading. Renewables start generating cash quickly. Nuclear does not. Even if nuclear produces reliable power for 60 years, the first 10 determine whether it ever reaches operation. Finance is front loaded. Risk is front loaded. Returns are delayed.

Recent policy changes help, but they do not change the core math. Tax credits reduce total cost, but they do not eliminate schedule risk. Loan guarantees help, but only if political support remains stable, thats why I look into the political changes more directly than the costs of Uranium for example.

English