Pasta™

37 posts

Pasta™

@PastaMaxxer

something something soon on Hyperliquid

Katılım Mayıs 2009

64 Takip Edilen802 Takipçiler

I've just published ~2 million MT1 and MT2 peptide analogs as §102 prior art with full pharmacology and synthesis protocols.

This is clearcutting any future patents of this class of peptide. I chose MT1+2 as a demonstration because they are the least likely to be monetized, and the least useful.

The reason for this is credibility, so there is little doubt when I say that I have about 98% of the patentable peptide analogs, all as high fidelity as the ones I just published, all with grade A markush filtering.

In total it's about 140 million analogs across 87 classes. I've predicted about 600 of those to be S+ tier in terms of effectiveness, etc. Ozempic without the osteoporosis, things like this.

I am not planning to publish any more analogs as prior art, but I could clearcut the entire peptide IP field. I think that would be foolish, so this catalog is available to purchase through inquiry on the coracle research website. I will only give this information to one buyer, biggest number wins, good luck!

coracleresearch.com/research/07-me…

English

@bryan_johnson Bryan what about the led lights destroying your circadian rythme and nervous system? Replace with red lights

English

English

One wallet, all access.

Trust Wallet@TrustWallet

Hyperliquid is now live in Trust Wallet with 0% markup on fees for 3 months. 🚀 With @HyperliquidX and @tradexyz, expect broader market coverage; RWAs & Commodities. 200+ Perp markets & deep liquidity. Learn more: short.trustwallet.com/hl-in-trust

English

@PastaMaxxer @ponyo_fp Tell me about hyperliquid success..

English

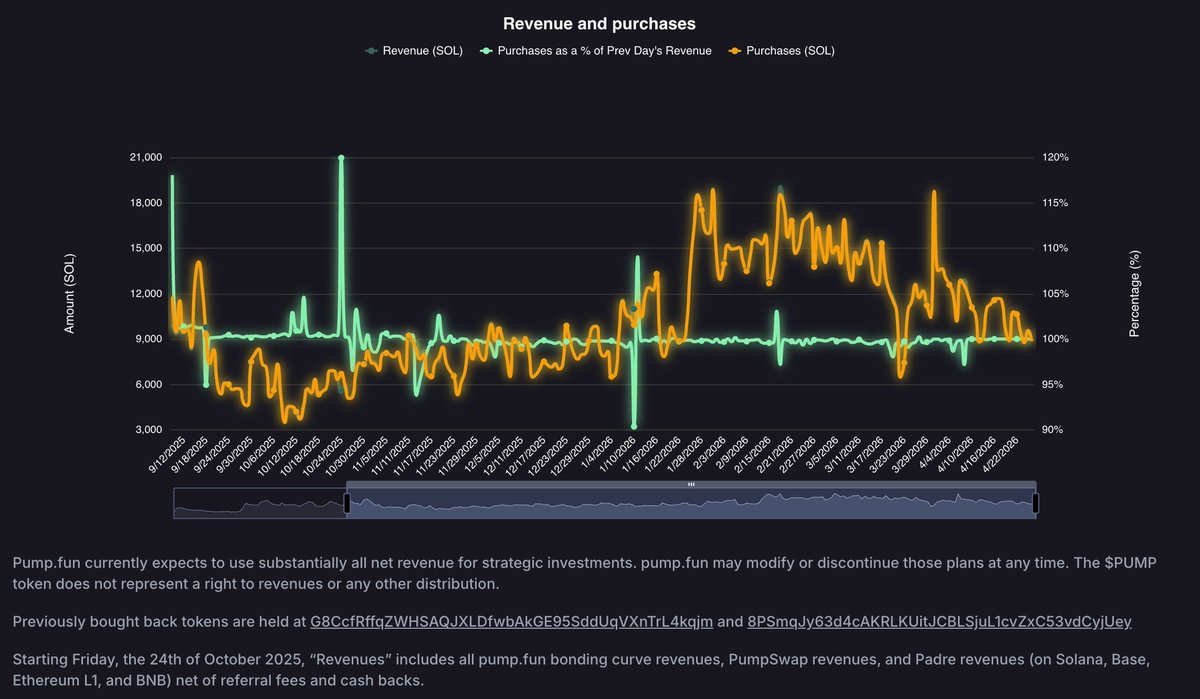

Pump.fun is going to burn their buyback tokens and gigasend it

pumpfun has spent $369M buying back 126.8B $PUMP, roughly 35.8% of free float. What’s the rational move with 127B tokens sitting in a treasury 74 days (Jul 12) before the team’s cliff unlock?

Let’s walk through the decision tree.

- Option 1) Sell 127B (roughly $224M) into $52M daily volume and you crater the token, suicidal for a team about to vest.

- Option 2) Recycle through staking, airdrops, or LP and you redistribute to holders who sell, a slower dump with extra steps while total supply stays unchanged.

- Option 3) Hold indefinitely and the pile grows by 520M tokens per day, compounding an uncertainty tax that the market prices as a permanent overhang.

- Option 4) Or burn the pile, reducing total supply from 1T to roughly 873B, the only outcome where every holder’s per-unit claim on future cash flows increases, including the team’s own unvested allocation.

Three of the four branches destroy value. The fourth is a one-time permanent removal that benefits everyone holding the token. The disclaimer on the buyback page says pump.fun “may modify or discontinue those plans at any time,” which means nothing contractually prevents a burn and nothing contractually guarantees one. But when three options lead to value destruction, the remaining option doesn’t need much advocacy.

July 12 turns the burn from nice-to-have into self-interest. That day, 82.5B tokens unlock as team (200B) and investor (130B) allocations begin a 36-month linear vfest. Post-cliff monthly emissions run roughly 11.9B, split between community (~5B) and team/investor (~6.875B). At current revenue of ~$920K/day and a $0.00177 token price, the buyback absorbs ~520M $PUMP per day, which is ~15.6B per month, running at roughly 1.3x buyback/emission coverage. Revenue has oscillated between $750K and $1.1M/day for six months now. At 1.3x, $336M a year in buybacks roughly matches post-July emissions.

Let’s run two scenarios. If the team burns before the unlock, circulating supply goes from 590B - 127B + 82.5B (cliff) = 545.5B, which is 7.6% below today’s float. If nothing burns and the cliff hits raw, circulating supply goes to 672.5B, a 14% dilution from where we sit. That’s a 22% swing in circulating supply, and needless to say the team's own 50B cliff tokens are worth more per unit in the first one.

Now strip the cliff out. 590B collapses to ~463B of free float, +27% per token at constant market cap. At $0.00177, $PUMP's market cap is $1.04B and FDV is $1.77B, down 80% from the all-time high. Against ~$336M annualized revenue, that's 3.1x on market cap.

Assign 30% probability to the burn and you're picking up ~8.1% in expected price impact from that scenario alone before any multiple rerating. The upside only requires the team to act in their own financial interest.

English

The fucked up thing about this is that despite knowing basically every PFP on this picture and remembering their X nickname

I've only met 2 people out of all of these pfps IRL lmao

Hyperretardio

Havoc.hl 𝕏@Havochl_

This is Hyperliquid Twitter. Did you spot your pfp?

English