Philipp2008

349 posts

Philipp2008

@Philip_pan2008

Semiconductor, the former Senior Marketing Director in WPG Holdings

Los Angeles, CA Katılım Aralık 2023

435 Takip Edilen162 Takipçiler

$PENG

Retesting the 8 year breakout looking for continuation.

Up.

bryan@BryzonX

$PENG breaking out of its 8 year base 👀 Don't underestimate a HTF breakout

English

@BryzonX Top professional analysis! Fortunately, I grasped it, but unfortunately, no heavy position!

English

$MXL swept ATH but closed back below

This leaves me to believe this move is just about wrapping up and we could be taking a much needed hiatus

MA's are just starting to curl up so it would be nice to allow them to play catch up

This has been one of the craziest moves i've ever seen and was lucky enough to catch it.

However, what i'm most excited about is their path to taking serious market share from $MRVL & $AVGO in the $8B 1.6T DSP TAM

They are using 2nm & 3nm nodes for manufacturing at TSM lol good luck getting capacity while $AMD & $NVDA are back in scale mode

Analysts say they are 9-12 months away from even starting production while $MXL is ready to start shipping with Samsungs foundry

Data centers are already out of power, if MXL's Rushmore can save your DC 30% in consumption you will never run out of customers in this environment

This move is well justified when you put into account that 60%+ of every sale going forward will go straight to profit now that they have serious operating leverage after spending all of 2025 investing in R&D

English

Thanks @DataCenterMilly

Wanted to repost your post with my answer since I have received A TON of DMs about ATOM this week. (woke up to 8 new ones asking basic questions)

Yes ATOM is speculative and pre-revenue. Plenty of pre-revenue companies have turned into profitable businesses before. I think even at $11 there is a ton of upside given they have 5+ "shots on goal" in the next few quarters where ANY SINGLE ONE can take this company to 30+ and 2 or more probably make it 50-100 per share.

Is there a chance they dont succeed? Yes- thats why I'm not all in. I think theres a greater than 80% chance of success and have been saying this since my initial posts in the 3s. Here is my original reply to his post for all:

claude doesnt understand the story. you didnt need AI to tell you its a pre revenue company. It absolutely is. Buying ATOM here is like buying a biotech with no approved drugs but great phase 3 clinical data in 5 applications and a huge tam thats being very underrated by the market. And no competing drugs waiting to steal that TAM from you.

Unusual Intelligence@DataCenterMilly

@joedab12 @bluezerone Love your work Joe. Claude had some choice words about cosmos:native

English

@joedab12

Hey Joe.

I appreciate your content.

Thank you.👍

English

@joedab12 No one asked the suits against MPWR from VICR in today’s call?

English

$VICR

So monolithic power talked up their vertical power delivery products a lot on the q4 call...

But on the q1 call they said ABSOLUTELY NOTHING about Vertical Power Delivery.

Very recently $VICR met with AI accelerator OEMS(plural- AMD+NVDA), and hyperscalers(plural as well, $GOOG $AMZN $MSFT $META all making their own ships) about VPD and demo'd their newest VPG gen 2 with 5th gen multiplication technology....

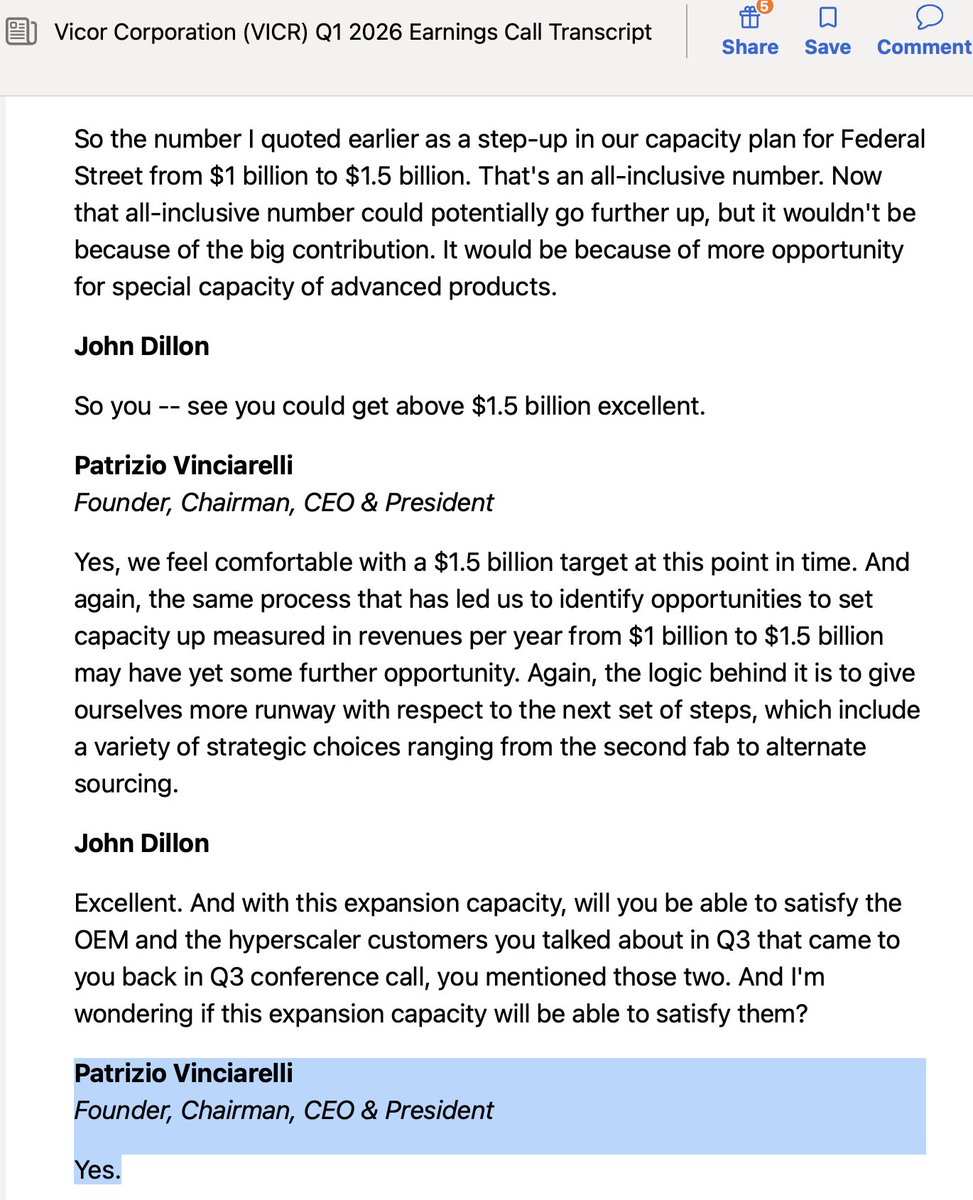

Shortly after those meetings they announced they are expanding from a previous $1b to $1.5b in annual capacity at their first fab in Andover MA. They also confirmed that expansion was because of the previously mentioned meetings with OEMs and Hyperscalers.

Previous to that they said there is 1 customer who can fill 2 fabs on their own(when 1 fab was 1b capacity) that they could not service due to lack of supply. They are working on a 3rd party license deal to service this customer (we all know its $NVDA - by far the largest).

Fab 1 is being filled by $GOOG and $AMD along with Cerebras who is set to IPO soon. It can't be more obvious.

English

@joedab12 Much appreciated for ur great post! Already added double last week! Enjoy reading ur professional posts everyday!

English

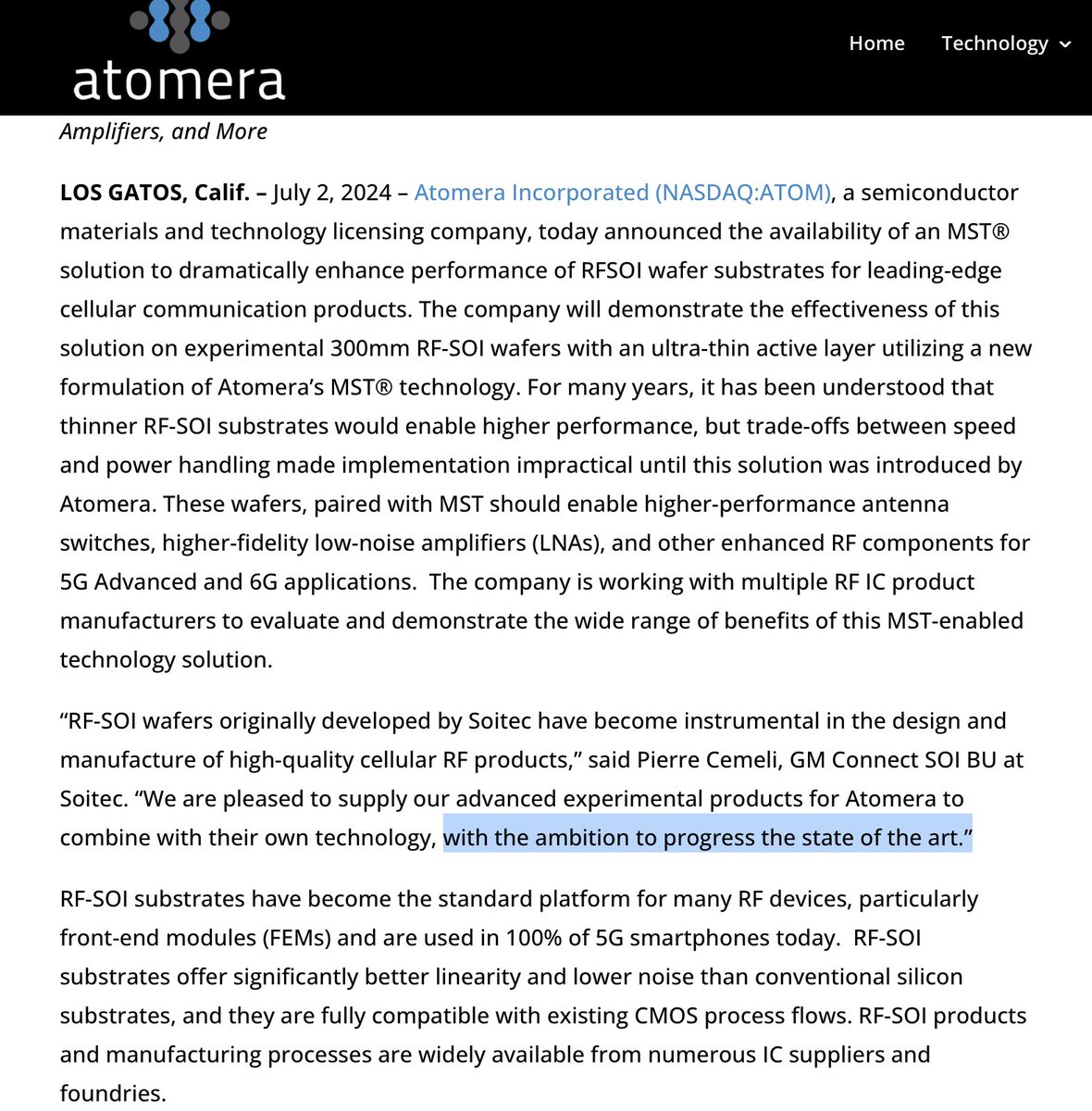

Atomera also announced a parntership with Soitec in July 2024 aimed at RFSOI products..where a soitec exec said they had "the ambition to progress the state of the art."

Recently Atomera used quite similar language when talking about GaN RF and GaN Power.

Is the evolution of RFSOI ---> GaN RF? Soitec is definitely working on GaN RF as well

Just sharing information. Not implying anything.

English

@aleabitoreddit @R_and_Invest Fking too good is bad! FQ3 ASP QoQ rallying +137%, but FQ4 (base on FQ4 guidance on midpoint) ASP QoQ only +17%! What’s wrong fking on earth!

English

$SNDK earnings are just way too good...

Q3 earnings:

Revenue: $5.95B vs. ~$4.7B (252% Y/Y growth, 26% beat)

EPS: $23.41 vs. ~$14.5 (62% beat)

Gross Margin: ~78.4% vs. 67.3% (+1,110 bps vs. Est.)

Q4 2024 projections:

Revenue: $7.75B-$8.25B vs. ~$6.5B (23% above estimates)

EPS: $30-33 vs. ~$23 (37.0% above estimates)

Memory companies (disclosure I do own Sandisk) are a bit easier to price in ahead of time vs. names like $RDDT (off of traffic data).

Just purely from third party stuff like NAND price hike reports... so all the repricing does happen ahead of time, not on actual earnings.

Regardless, this is formal confirmation that memory companies are going brrr...

Astronomical earnings from memory players and they'll likely keep marching upward over this year.

English

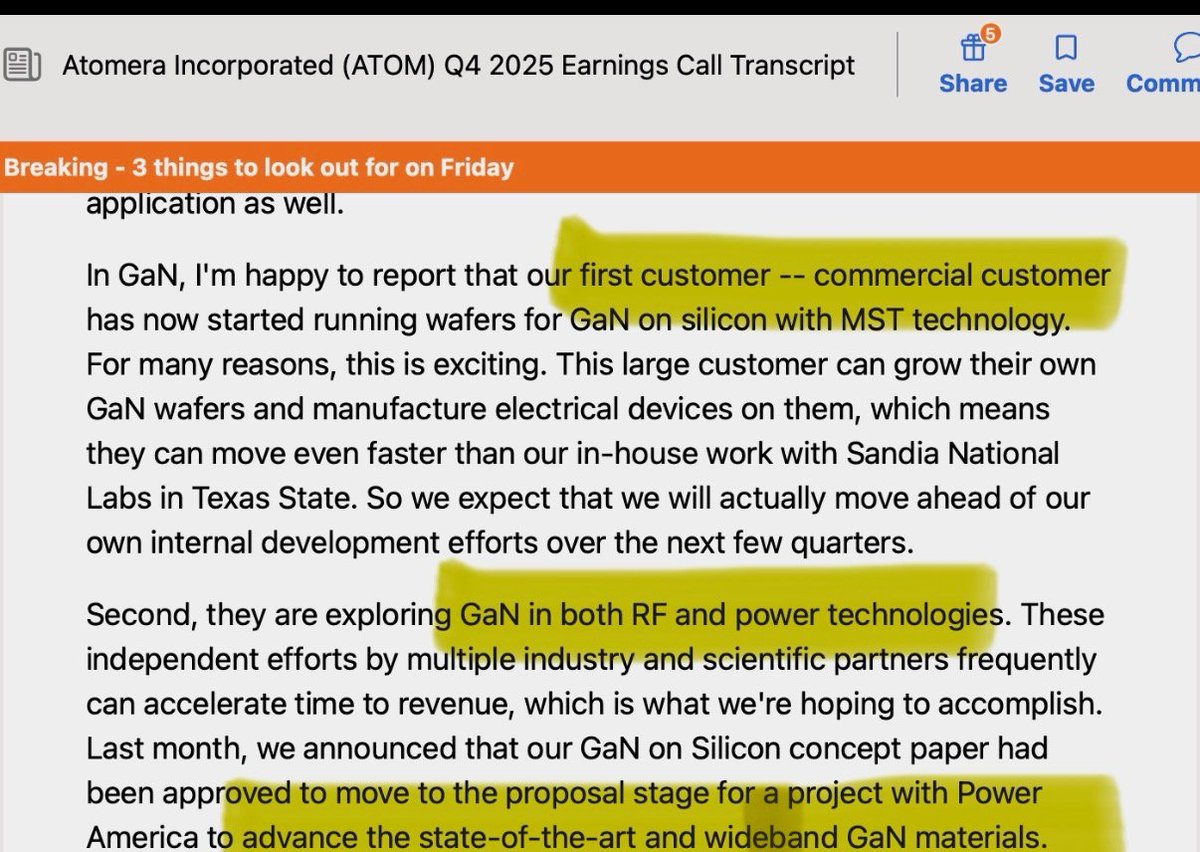

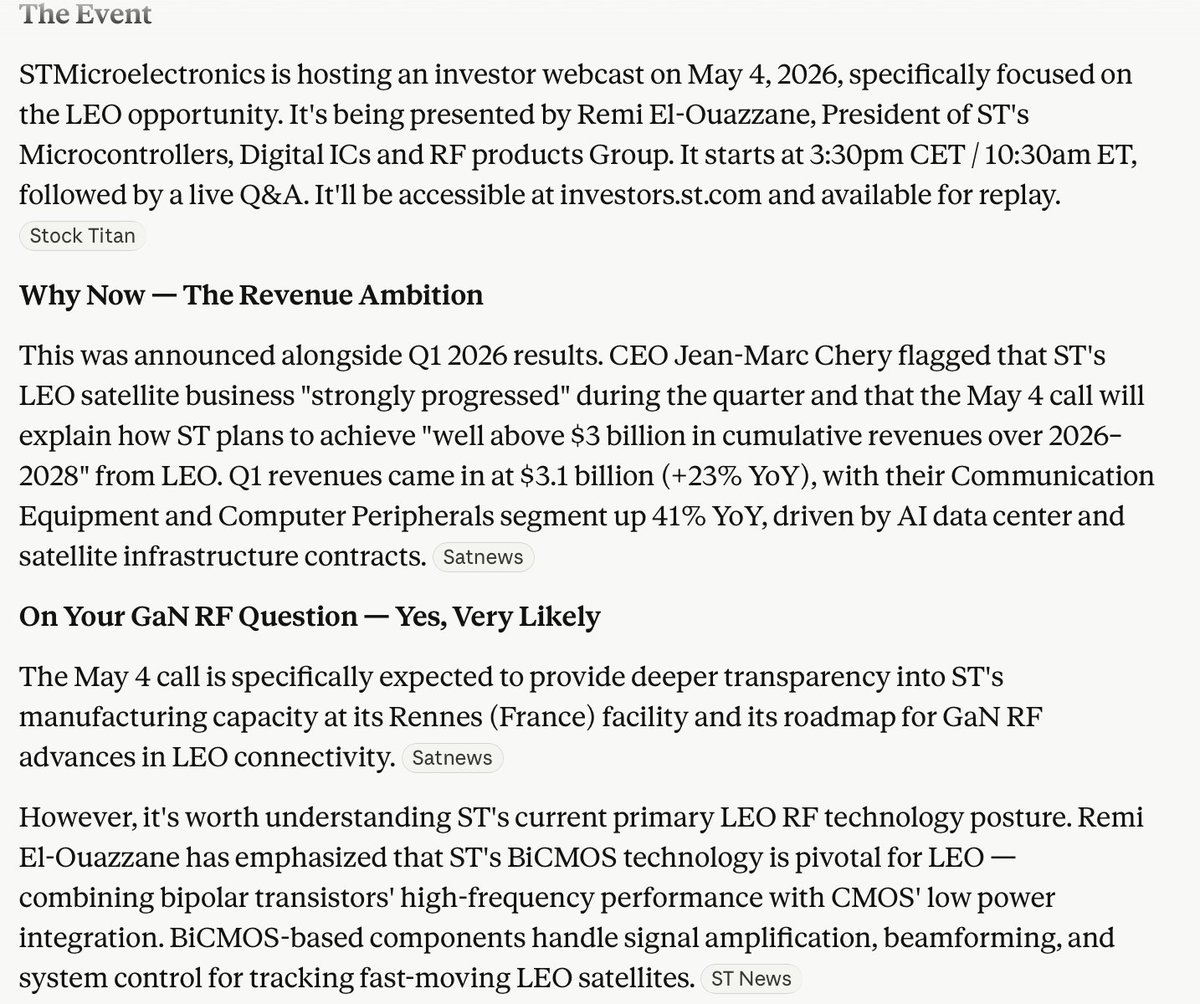

Here's an Atomera post I wasn't expecting to make until I saw some unusual call buying on $STM today... Apparently ST Micro has a Low Earth Orbit event monday I wasn't aware of until now.

ST Micro installed Atoms tech into one of their fabs in late 2023.

At this LEO event they will likely talk about the GaN RF roadmap.

Atomera has said they have a customer running wafers in GaN RF(and GaN power)- they also indirectly told us that customer is ST Micro. How do I know this? "First commercial customer."

STMicro was confirmed to still be running wafers after scrapping an initial bcd110 project due to delays in solving reliability issues(they were solved too late to design into the new 300mm process in Agrate)

Just last week $SNPS decided to put an Atom module for GaN RF and GaN Power into their chip simulation software

I'm not making predictions-just presenting facts.

I own a lot of shares and will continue to own a lot shares for a while.

English

Only $LITE has publicly shown (many times) their high power laser noise performance.

Not a single competitor has dared to publicly show their noise.

Go ask $COHR, $AAOI, Furukawa, or any of the "Chinese competition" what their RIN and linewidth are. They will not answer you.

English

You still can't scale manufacturing testing using VIAVI $VIAV solutions as evident today at their OCP demo.

Curious to see their commentary on hollow core fiber testing.

TheValueist@TheValueist

$VIAV post ripper. Sometimes it helps to simply get out there and touch the products. (Bloomberg) -- Viavi forecast net revenue for the fourth quarter; the guidance beat the average analyst estimate. FOURTH QUARTER FORECAST Sees net revenue $427 million to $437 million, estimate $402.3 million (Bloomberg Consensus) Sees adjusted EPS 29c to 31c, estimate 24c THIRD QUARTER RESULTS Net revenue $406.8 million, +43% y/y, estimate $393.3 millionNetwork Enablement revenue $321.5 million, +71% y/y, estimate $191.1 million (2 estimates) Optical Security and Performance products revenue $85.3 million, +11% y/y, estimate $83 million Adjusted gross margin 62.2% vs. 60% y/y, estimate 61.3% Adjusted EPS 27c vs. 15c y/y, estimate 23c Adjusted operating income $85.5 million, +79% y/y, estimate $77.4 million Adjusted net income $67.6 million vs. $33.9 million y/y, estimate $56.3 million COMMENTARY AND CONTEXT Sees aerospace and defense end markets as strong drivers for the foreseeable future For the fourth quarter of fiscal 2026 ending June 27, 2026, the Company expects net revenue to be between $427 million to $437 million and non-GAAP EPS to be between $0.29 to $0.31.

English

@joedab12 Great! added in 50% before close just for little casino lol

English

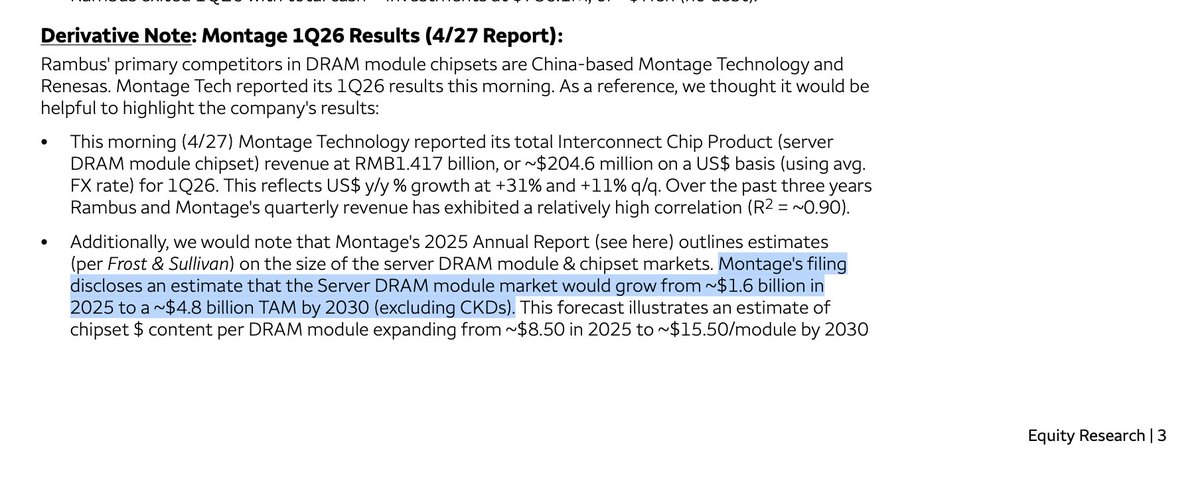

@joedab12 The interface and timing chip of Server DIMM, hot competition market, much lower margin rate than license biz, RMBS how to compete with china players lol

English

$RMBS found this little blurb from montage(rambus competitor) annual filing in a report from wells fargo...

Montage saying the TAM will triple by 2030

Meanwhile RMBS is STEALING market share from Montage and Renesas; remember, Rambus product biz is fairly new and really started ramping in 2017-Montage has a decade on RMBS-they started in 2008.

Rambus CEO needs to talk up the increasing tam way more. He's being extremely conservative.

English

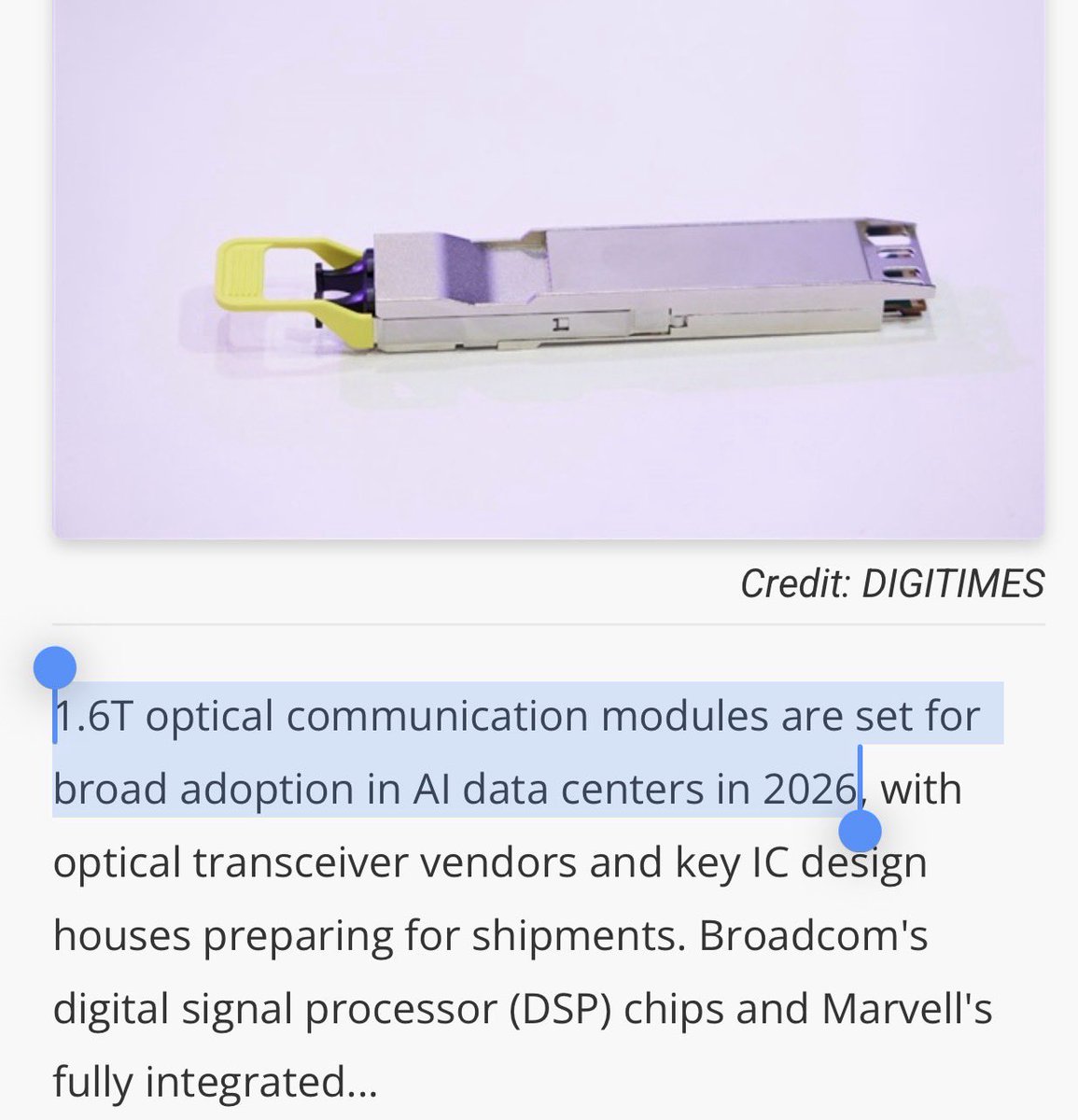

@aleabitoreddit 1.6T optical modules adoption absolutely bullish $MXL, who are ramping up 1.6T DSP +TIA in 2H26

English

“1.6T optical modules are near mass adoption this year”

So nothing new but this just confirms timelines for volume production/mass adoption H2 2026.

$AVGO and $MRVL are cited as main beneficiaries in the report but names like $AAOI are probably the most profound beneficiaries (largest 1.6T capacity US projected) for the pure play exposure.

$JBL also set to go brrrr but my guess is H1 2027 with wave2 architectures since their LRO architectures remove the DSP (with $INTC SiPH acquisition IP).

Jabil would be a good contrarian long in the broader 1.6T supercycle coming up if this gets broader adoption from $META validation but benefits anyway.

And especially $SIVE that powers Jabil 1.6T LRO, that when they scale, it scales laser demand too.

I think everyone focuses on the upstream supply chains nowadays but going long on Broadcom and Marvell doesn’t hurt too.

English

@joedab12 Whenever u sold out, the price keeps rallying till to $100 for sure lol

English

@insane_analyst The stock price of CRDO will be fucked today lol

English

Micro-LED is a hoax and will never work. Electrical crosstalk alone kills this retarded idea. Jitter induced by the LEDs kills it even more.

English

Jukan's Truth Time:

Many people have been asking:

"Samsung has its own DRAM division — so why isn't it aggressively pursuing mobile device market share expansion during a memory shortage like this?"

Today, I'll give you the answer.

First, let me clear up a common misconception.

Samsung's MX (Galaxy division) and Samsung's DS division (semiconductor division) only share the Samsung name — they do not share a single, unified interest. Each puts its own profits first.

This became clear in what happened before Samsung MX launched the Galaxy S25.

At the time, Samsung MX concluded that the LPDDR5X built on Samsung's 1b node lagged behind the offerings from SK Hynix and Micron in both performance and thermals. Yet Samsung DS was trying to sell this underperforming LPDDR5X to Samsung MX at a higher price than SK Hynix's and Micron's LPDDR5X.

This led to an unprecedented outcome: Micron — not Samsung — became the first vendor for the mobile DRAM in Samsung's flagship S-series smartphones. (TM Roh, head of Samsung MX, later denied this. But for at least the initial-to-mid production volumes, Micron has been confirmed as the first vendor.)

Now, however, the situation is reversed. As the term "Memorypocalypse" floating around the market suggests, memory is currently in extreme short supply.

So — after going through what happened in 2025, would Samsung DS really turn around and supply LPDDR5X to MX at a discount?

Another interesting point: one of the reasons MX cannot source DRAM cheaply from DS is that DS has to be mindful of its external customers.

Specifically, if Samsung supplies DRAM to its internal divisions at a discount, its external customers — who are already paying steep prices for DRAM — would be deeply unhappy. Trust between Samsung and its customers would break down, and customers would hold a grudge against Samsung.

Samsung DS reportedly has no appetite for taking on that kind of risk.

As a result, Samsung MX, having already incurred massive costs in Q1 due to difficulty securing memory and a sharp rise in its procurement prices, is expected to spend even more in Q2 to meet its volume requirements as the world's largest mobile device manufacturer.

This aligns with reports that TM Roh, head of Samsung MX, has briefed management that MX could swing to a loss this year.

In conclusion, the reason Samsung MX cannot aggressively pursue a market share expansion strategy during this memory shortage is not simply that "Samsung has a DRAM division but can't make use of it."

The core reasons are threefold:

First, MX and DS sit under the same Samsung roof, but their interests diverge. Second, DS has no choice but to prioritize its own profitability and its external customer relationships over internal supply. Third, in the current memory shortage environment, MX — like any external customer — is structurally forced to bear elevated memory costs.

That's all for today's Jukan's Truth Time. Thank you.

English

@aleabitoreddit I also owned $Sive, but really no need repeat the OLD information every day! I buying in the company just based on the two basic logics: 1) Sive’s DFB already GR-468 qualification, quality proved; 2) studying the background of the cofounder and CTO Andrew McKee, a genius!

English

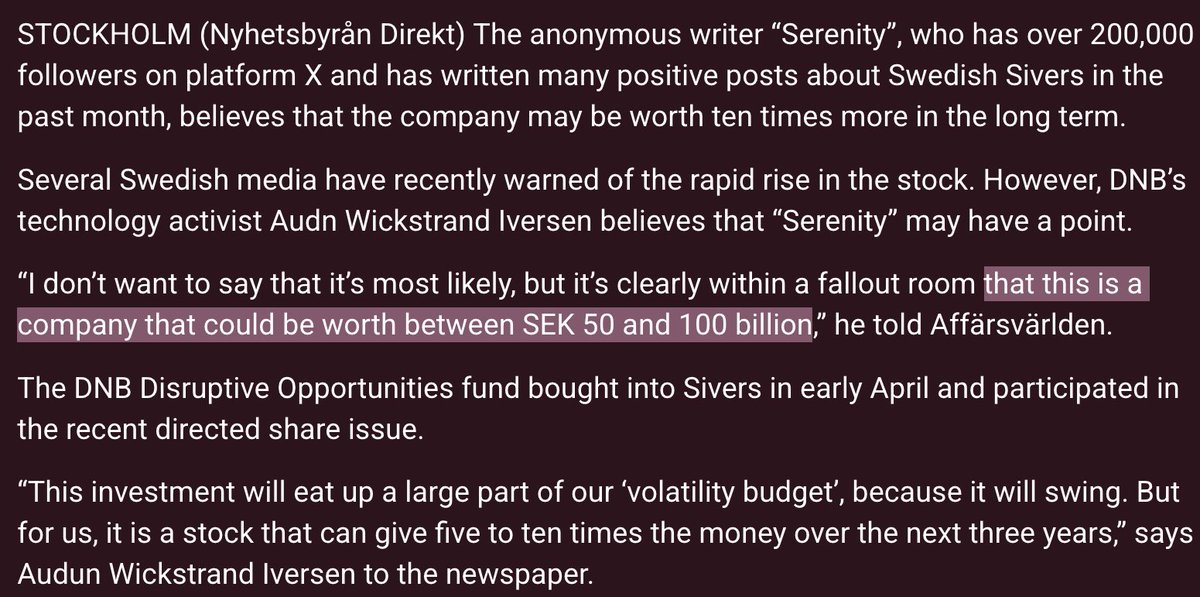

Agreed, and glad DNB, one of Europe's leading banks, went out to defend $SIVE valuations alongside me.

I still think $SIVE can reach $10B MC in 1 year time as their laser growth scales proportionally to:

- $AAPL Watches

- $JBL 1.6T Volume

- $MRVL CPO Volume

- Ayar Volume

- $POET Volume

Depending on how their qualification plays out into volume ramp.

As Sivers supply lasers to all the next generation of 1.6T/CPO players in the space (into ~ $AMD, $NVDA, $AMZN, $MSFT type supply chains).

These are EXISTING players at a ~990M MC. Not even including TAM expansion or more partnerships coming up.

Especially now with NASDAQ listing, US institutions are forward looking and price in ~12M ahead of time, compared local European valuations that mainly look at previous 12 months.

Banks usually provide very conservative targets (eg. 3 years for a 10x), but I do see potential for this company to be the next $LITE very soon.

Europe should embrace positive-sum growth of their own companies that supply to hyperscalers.

As their frontier companies provide back to locals through taxes, economic growth, and job growth.

Ⅎ F@FlachtFunds

@aleabitoreddit $SIVE market cap is a complete joke next to all the other CPO names. Sub 1 billion MC with a US listing on the way.

English

@joedab12 Goog for sure, they used VPD from V5 and going through V8; AMD MI350 not using VPD, maybe MI500?

English

@Philip_pan2008 it definitely will help bring new eyes. but i think more and more people will figure what i've been saying about fab1 being full with google+amd in the next 2 weeks.

English

$VICR

Excited to see how many new people realize $GOOG and $AMD are ramping Vicor VPD this week. Its so blatantly obvious and the share price continues to trend up-but the masses haven't figured it out. Its as if they're waiting for BofA or Goldman to come out and say it.

Are you guys really not smart enough to figure this out on your own?

Please read all of this closely and dont wait for the analysts to tell you Vicor landed Google and AMD before buying-its really not that complicated.

English