Sabitlenmiş Tweet

PORTFOLIO UPDATE MARCH 17TH 2026

Buys: $NOW $MELI $TTD $ADYEN

Sells: $NOW $NU

It’s been an incredibly fascinating first quarter to start the new year (not technically finished I know) with the SaaSpocolipse continuing as well as a stellar earnings season in my opinion, which I really enjoyed following. These two events as well as many other nuances have led to multiple intriguing opportunities for the long term investor, so much so I’ve felt almost spoilt for choice, it’s not an exaggeration to say I feel like I’m suffering with mild decision overload right now which is funny because I’m sure my buying decisions really don’t require as much thought as I’ve been allocating recently. I’m sure that’s something we’re all guilty of at times.

Since the last update was published I started a position in ServiceNow which I then sold within probably 6 weeks, which I’ll explain why. I also sold my entire NU bank position.

Regarding buys, I increased my allocation to The Trade Desk and MercadoLibre significantly, doubling my position in both. I also increased my Adyen holding by 20%.

Of course we also made deposits into the account each month.

Buying and selling $NOW

This is actually a really simple one. I saw (and still do see) ServiceNow as a great opportunity long term at the current price point. I wrote a promising deep dive on the company and then actually decided to start a position just before earnings. I entered the stock at $129 and then sold at $120 about two weeks ago. So it’s a small loss, it’s much of a muchness to be honest. It doesn’t even need covering but I’ll always promise and provide transparency here. The only reason I sold the position was because I see multiple other interesting buying opportunities emerging within my portfolio with companies I hold a stronger conviction and understanding towards. Naturally because both conviction and deep understanding take time to develop and strengthen, I felt more comfortable and importantly, more excited to allocate that capital towards other positions. I was struggling to justify a new position when I saw so many opportunities within my current holdings. It’s funny because the problem is I haven’t fully yet decided where that capital is going to be deployed, so today it sits at a 4% cash position whilst I ponder over the coming days.

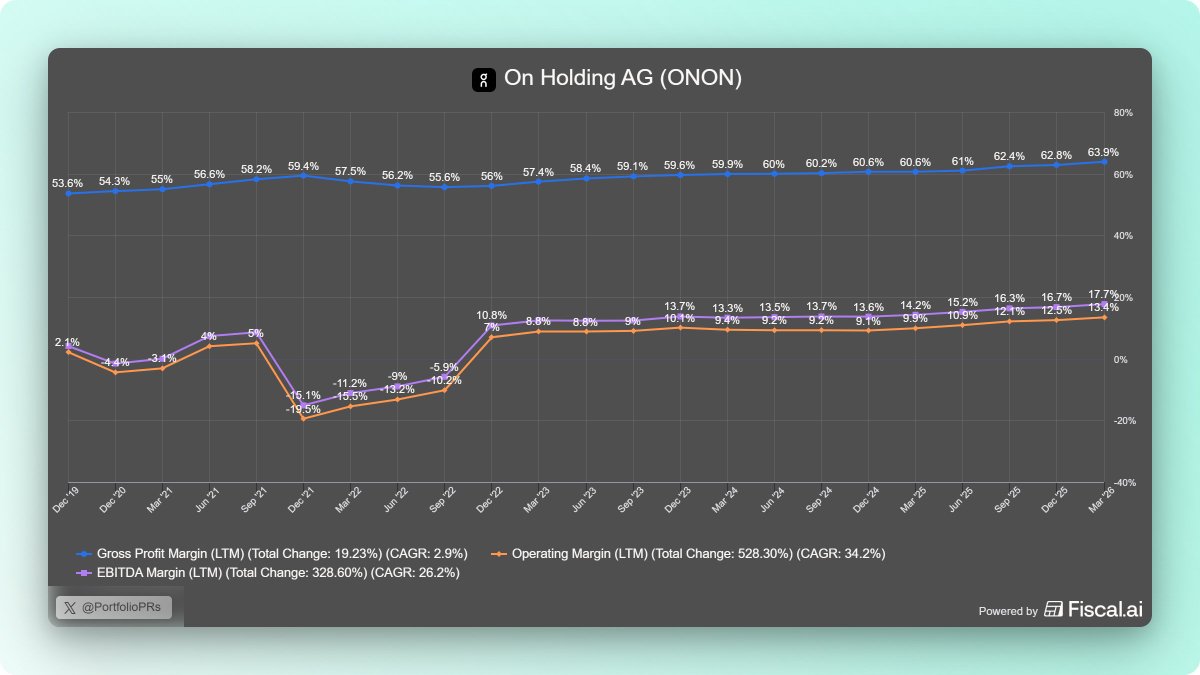

I’m contemplating between deploying it into more $UBER, $NFLX, $SHOP, $DUOL, $ONON, $META or $AMZN.

Gun to my head I'm thinking a split between $NFLX & $SHOP

Rolling NU into MercadoLibre

I sold my entire $NU position for a gain around 30% which is nice but the amount of time I held shares of Nu it did underperform. I made this decision because I view MercadoLibre $MELI as arguably the best opportunity on the market today for long term investors. I actually really like NU as a business and as an investment but I simply get excited by MELI so much more. I could have certainly sold a business of arguably less quality than NU in order to scale my MELI position but that would have left me with portfolio exposure to Latin America north of 15%, which isn’t something I’m comfortable doing right now. As MELI grows as I predict, paired with me continuing to buy shares over time, that’s a reality which may likely happen but there’s no rush to jump in so heavily right now.

I believe it’s quite simple. While it’s true that MELI and NU serve slightly different fintech purposes and each can flex unique strengths, MELI is the superior business by almost every metric. I’d argue the majority of investors holding both businesses would agree.

With MELI, you aren't just buying a bank, you’re getting multiple top tier businesses that intertwine to create a powerful flywheel effect. You have the marketplace, a fintech arm and an unrivalled logistics network. This is all supported by high potential verticals like advertising which is growing at 60%+, memberships and streaming.

While NU is the dominant fintech play today, Mercado Pago is closing the gap with speed. When you factor in MELI's ability to easily onboard users through the marketplace, it’s not just feasible, it's likely that they surpass NU in fintech users over the long term. At the same time their success “off-platform” is proving Mercado Pago isn't just an in-house' tool anymore thus proving it can win the open market. This is before we even mention the huge data advantage the marketplace gives them to underwrite loans for the credit business, unlike Nu.

Finally, while NU has a respectable moat, it is ultimately a digital one. The logistics infrastructure MELI has built is a massive, physical, hard asset moat that competitors simply cannot replicate at scale as we’ve seen with Amazon here. At the current valuation MercadoLibre is just too good to ignore.

$TTD

I used some of the ServiceNow money plus my monthly deposit to double my position in $TTD. Granted the position was one of my smaller holdings in the first place, then it had a horrible drawdown so after doubling up and of course averaging down my TTD position is still sub 5%.

I don’t believe this needs a massive explanation, It’s more likely I talk about TTDs current situation in depth in the newsletter but I do believe the business has become extremely misunderstood and pessimism has simply gotten out of hand, I believe we’ll look back at TTD in the twenties as a great opportunity years from now. I doubled the position at $29, I did want to buy at $23-$25 but I was waiting for the deposit to hit and annoyingly missed the run, but that’s completely fine. Why? Because when you have a thesis and conviction you shouldn’t let 10%/20% or more swing scare you out of potential decade long investment. I still think $TTD is undervalued so I won't miss the forest for the trees.

Sadly No PRs to report in the portfolio, In due time we’ll get back to all time highs and then of course surpass that, however on another note we did hit a great PR on my morning run today, so at least Portfolio PRs can report one PR🙂

House keeping ~ Funnily enough I’ve decided to change the name on the platform once again so after going by everydaystocksx for approximately 2 years my new name lasted about 2 months which is funny, I prefer this new set up. I’m pretty casual on social media so a casual name made much more sense. I also plan to talk more on other topics which I’m passionate about, because why not. Plus who really cares, it’s an X name lol but this one should deffo stick moving forward.

English