Priyanka Tanwar

245 posts

Priyanka Tanwar

@PriTanwar28

📊 Ex-Financial Analyst | Entrepreneur 🚀 Business builder & trading enthusiast 💡 Guiding you to entrepreneurial success 📈 Trading tips & insights

Ludhiana Katılım Ağustos 2024

89 Takip Edilen12 Takipçiler

4 ghante ki candle close hone me thoda waqt hai aur market ekdum shant baithi hai aisi range me bina brokerage ki tension liye positions accumulate karna easy ho jata hai wazirx pe zero fees matlab har small tick pe nazar hai #candleclose #accumulation #btcinr #wazirxzero

Indonesia

@Nithin0dha @zerodha Still, I found @zerodha is more expensive than other brokers , instead there are more few brokers who are best and pocket friendly like @ShoonyaApp @kotakneo @dhan

English

This is crazy. Btw, investing in stocks, ETFs, and direct mutual funds is free at @Zerodha.

Meb Faber@MebFaber

AHAHAHA, they actually did it. The cretins at @Fidelity are charging retail $100 commissions to trade 1 share of some ETFs. Gross.

English

@TradingwithFun1 Agreed, feels like regulations are just being made to watch while traders/investors keep losing money & then they put out that disclaimer saying 9 /10 people lose money in trading.

aaj @ShoonyaApp mein bhi settlement hua and i lost the potential to trade .. bloody regulations

English

Now what if someone sold calls to avoid the quarterly settlement!

Bloody market regulators!! Not even a single decision ever to help traders or investors.

English

@thegaursaahab @ShoonyaApp arey yr ye har baar ka pnga hai on every quarterly settlement.. isme kyaa hi kr skte hai but ha atleast they are informing this from last 2 days ... emails and mobile app notifications pe

English

What the fuck

Where is the wallet money

Why wallet is not showing ?

@ShoonyaApp

English

@Roopa_1988 In mobile app its reflecting under my funds ..

when u click on ur name initials (top right corner)

English

IMO , NIM compression is the biggest concern. Lower yields + mix change is hurting more than rate cuts alone.

#HDFCBANK

PG Capital@_PGCapital

#HDFCBank $HDB #HDFC Q4'26 Earnings deep dive HDFC Bank reported a good balance sheet quarter, but the P&L was still meh. Deep dive👇 Starting with the balance sheet, deposit growth was good at 14% YoY (CASA 12% and FDs 16%) helped by overall system deposit growth. CASA ratio stayed at ~34%, where it has been for the last 6 quarters. Loan growth held at ~12% YoY, same as Q3’26, and has clearly improved from the weak levels seen a few quarters ago, broadly in line with what management's expectations. Since deposits grew faster than loans, LDR improved to 94.6% from the 98–99% range in Q2–Q3’26 (It was ~95% in Q1’26 as well, so the expectations will be to keep improving from this point onward). Management is right that LDR is not a regulatory constraint, but it still matters for HDFC Bank because it affects both growth flexibility and NIMs. If the bank wants to participate meaningfully in system credit growth, it will need to sustain strong deposit momentum. Deposit growth is important for every bank, but for HDFC Bank it matters even more right now. Wholesale borrowings also fell ~11% YoY, which helps funding costs at the margin. Moving to the P&L, the picture was weaker than the balance sheet. Despite 12% loan growth, interest income was flat and total interest income was down 1% YoY. Repo rate and loan mix explain a lot of this. HDFC Bank’s ~₹30 lakh crore loan book is now roughly split between retail and wholesale/agri. That matters because retail loans carry higher yields, while wholesale loans carry lower yields. In Q4’26, retail grew only ~8% YoY, while wholesale grew ~16%. Even within retail, credit card loans were flat YoY. This is not a one-quarter issue either. The same trend has been visible for the last 3–4 quarters. In fact, most of the acceleration in overall loan growth from 5.5% in FY25 to 12% in FY26 has come from wholesale. Wholesale growth moved from just 2% in Q4’25 and 3% in Q1’26 to 16% in Q4’26. As a result, loan yield fell to 8.4% in Q4’26 from 9.4% a year ago and 8.6% in Q3’26. That is why total interest income was down 1% YoY and flat QoQ. Of course, lower repo rates would explain a major part of the YoY decline but impact from mix was not insignificant. Interest expense declined 4% YoY and 1% QoQ as rate cuts started flowing through to deposits. But FD repricing always happens with a lag, since lower rates get passed on only when deposits come up for renewal. Management said full repricing of time deposits takes 5–6 quarters, so there is still some benefit left to come over the next quarter or two. Lower wholesale borrowings also helped a bit, though that was partly offset by faster growth in term deposits versus CASA. Cost of funds came at ~5.0% versus ~5.7% a year ago and ~5.3% in Q3’26. Since interest expense declined slightly more than interest income, NII still grew, but only by a modest 3% YoY. Calculated NIM came at 3.31%, down ~10 bps QoQ. Reported NIM, however, was up 3 bps QoQ. That difference is not unusual, since our calculation uses end-period balance sheet numbers while the company reports NIM on average assets. Other income was not too impressive either. It grew ~10% YoY, but excluding trading income, which can be volatile, growth was closer to ~7%. Overall revenue, meaning NII plus other income, grew just 5% YoY, or ~4% excluding MTM. Expenses grew 5% YoY, which looked fairly controlled. In fact, the bank has slightly fewer employees today than it did two years ago. That helps cost ratios in the near term, but over time the bank will still need stronger revenue growth rather than just tighter cost control. Cost-to-income was ~40% in Q4’26 and has stayed in a fairly narrow band since the merger. Since both revenue and operating expenses grew by roughly 5%, PPOP also grew by about 5%. Now coming to the most erratic line on the P&L — credit cost (Who said managed!? It’s called smoothening, ok!) This line is always hard to analyze cleanly, so it is better to focus on things like GNPA and slippages. GNPA came in at 1.15%, improving 18 bps YoY and 9 bps QoQ. PCR stayed stable at ~67%. Slippages also improved, down 17% YoY. So overall asset quality remained solid, still the bank’s core USP, and as management reminded us, “tested across 3 decades of business cycles.” No complaints here, thankfully. Coming back to the reported credit cost of ₹2,600 crore, this included ~₹2,700 crore of write-offs and some write-backs. (Who said managed again!)Credit cost was down 18% YoY, which is pretty much the same as the decline in write-offs, and came in at 0.36% of average loans. So 5% growth in PPOP and an 18% decline in credit cost led to 8% growth in PBT, or 6% ex-MTM, and 9% growth in PAT/EPS, or 7% ex-MTM. Coming to return ratios, ROA and ROE remained steady at ~1.8% and 14% respectively. Capital ratios also stayed comfortable. Book value per share grew 11.7% to ~365rs. Thoughts: deposit growth was good. The rest was meh. HDFC Bank used to be a clean high-teens earnings compounding story. Right now it is a single-digit earnings growth bank with a repairing balance sheet. That is still progress. It is just not the old HDFC Bank yet. Outlook for FY27: corporate loans should remain a key driver. Management called out demand in electronics, semis, auto/ancillary, renewables and food processing. Retail should improve too, with better traction in wheels, personal loans and mortgages. MSME/business banking also remains strong. So FY27 is unlikely to be only a wholesale-growth story. Was 12% growth good enough? Maybe not great, but fair. Management said they had planned around 10.5%–11.5% system growth, while actual period-end system growth ended up closer to 13.5%–13.9%. So yes, they were behind the system. But not by a mile. And they clearly do not want to force growth after coming from just 5.5% last year. I think that is sensible. The real monitorables for FY27 are deposit momentum, retail growth, and whether NIMs finally start to recover as deposit repricing catches up. More on valuation and future projections in the next post!

English

Fair trials and unbiased selection are essential to restore trust in Bihar cricket

#SaveBiharCricket

English

Priyanka Tanwar retweetledi

Has RBI really announced 'new rules' for exchanging old ₹500 & ₹1000 notes❓

Some news reports claim that the Reserve Bank of India (@RBI) has issued new guidelines to exchange discontinued currency notes.

#PIBFactCheck

❌ This claim is FAKE!

❌RBI has made NO such announcement!

✅ The official RBI website is the only authentic source for updates on financial regulations and currency-related announcements.

👉For verified information, visit:

rbi.org.in

🚫 NEVER forward unverified messages. Stay alert and share only information from trusted official sources.

📩 If you come across any suspicious message, photo, or video related to the Central Government, send it to us. We’ll verify it for you:

📱 WhatsApp: +91 8799711259

📧 Email: factcheck@pib.gov.in

English

@rakesh_d3 @akshit_ac @GovindKuma66166 @groww_cs @_groww One thing I’ve understood is that you should never rely on just one broker. You should always have at least two brokerage accounts. And

English

Exactly.... Why should we pay taxes & brokerage for their screw up? This is not compensation, it’s damage control at best. @groww_cs can't just dump the extra cost on users and walk away. We deserve a full refund including every single rupee lost, or this needs to be taken to @SEBI_India .

English

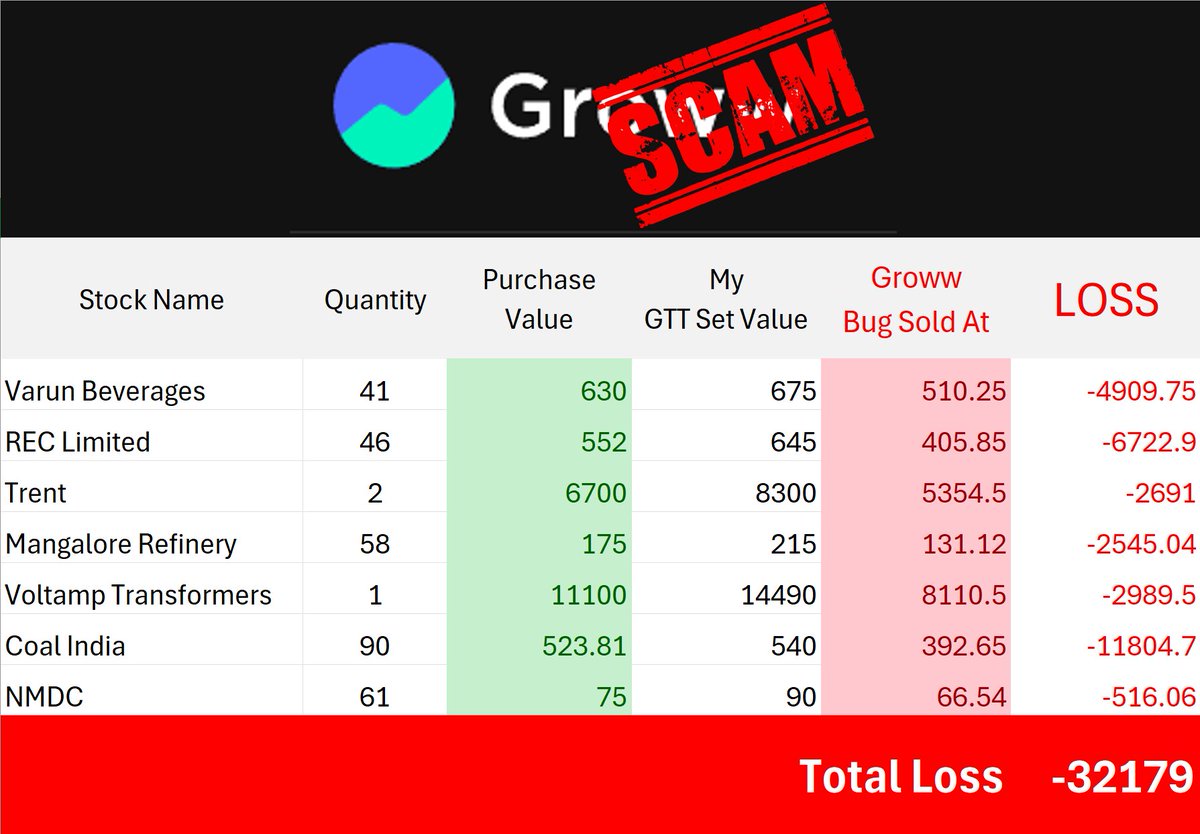

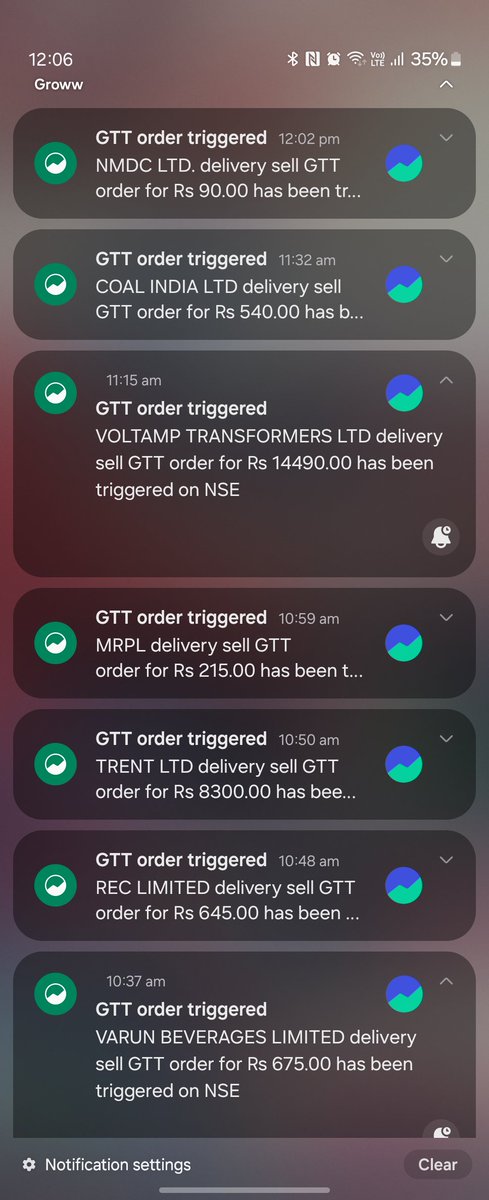

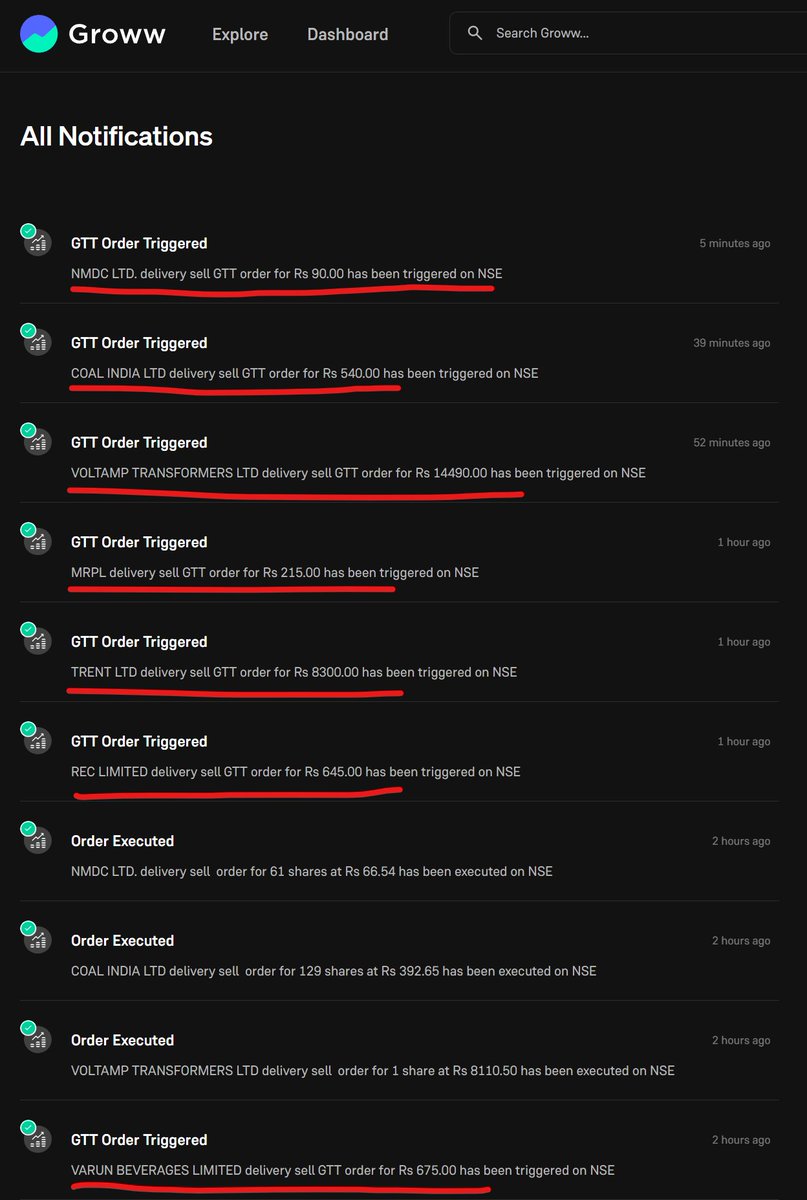

Massive Loss 🚨 of -₹32,179 because of @Groww_in's bug today.

Due to a technical glitch by Groww, all my GTT orders were executed at market price, completely ignoring my set trigger values.

@groww_cs Hereby,

🟥 I demand an IMMEDIATE FULL REFUND of ₹32,179

🟥 If not resolved, I will file a police complaint and escalate this to SEBI.

This is NOT a user mistake — it's a critical backend failure on your part @GrowwEngg

I’ve attached full proof with screenshots.

@groww_cs @SEBI_India @FinMinIndia @livemint @bsindia @TOIIndiaNews @moneycontrolcom @zerodha @IndianExpress @ETNOWlive @CNBCTV18News @ETMarkets @CNBCnow @business_today @NSEIndia @jagograhakjago @EconomicTimes @CNBCTV18Live

Everyone in the investor community, beware!

#GrowwScam #StockMarketIndia #GTTBug #GrowwFraud #InvestorsBeware #groww

English

@rakesh_d3 @akshit_ac @GovindKuma66166 @groww_cs @_groww I’m sure Groww won’t refund the extra charges for taxes and brokerage. That’s why they’ve told users to repurchase and settle off the difference n ol..

They’re smart enough to know that most people won’t bother checking the brokerage and tax section.

English

@YadavSaumya999 @shareefmk14 @Groww @_groww @ShoonyaApp im sure they wont reimburse anything unike @ShoonyaApp

English

@shareefmk14 @Groww Oh damn @_groww has been acting weird. I hope they could resolve this asap. In the meantime I am gonna use my @ShoonyaApp account.

English

@ashwiniGG98 @Ishita1_4_3 @Groww @ShoonyaApp @_groww haa ya exactly i had my holdings on @_groww and @ShoonyaApp ..

also faced loss due to grow's today glitch

now lets wht will thy do in terms of reimbursement

English

@Ishita1_4_3 @Groww Thank god I have my holdings in @ShoonyaApp for now. warna mai bhi aaj raise hi stuck hota. Anyway, did you raise a ticket with @_groww ?

English

@ShoonyaApp ohh my my #Modiji thoda prakaash yaha bhi daalo dekho to delhi k badhte rates

हिन्दी

Paying rent or paying EMIs — either way, it’s not cheap in metro cities.

Here’s what a 2BHK costs monthly in 2025 across India’s biggest metros.

Planning to move? Better plan your budget too.

#MetroLiving #RentInIndia #MoneyMatters

English

English

@rakesh_d3 @akshit_ac @GovindKuma66166 @groww_cs @_groww correct , exactly my point... taxes and brokerage to hume khud hi bharnaa pdega i m sure chup jaayenge ye log us time pe

English

Yes, they’ve said we have to repurchase the stocks tomorrow at CMP before 10am and they’ll refund the negative difference, but are they going to cover the taxes and brokerage too? That part is still unclear. We need a proper and transparent response from @groww_cs @_groww . This is really frustrating.

English

@_groww like others I have aso suffered from the same concern. My GTT order on executed before the trigger price was hit, leading to a huge loss. Trigger was set above market price, yet the order executed prematurely.

how will u guys compensate ?

English

QME

@THESMTRADERS or abhi to dekhte jaao modi ji kyaa kya krenge , m to mentally prepare hu portfolio or red jhelne k liye

HT

As an investor, I’m prepared to see a 50% loss in my portfolio — but I also want to see Pakistan split into four.

India would stand as strong as China — if Pakistan didn’t exist.

Pak bleed 🩸 India from last 40 years .

#PahalgamTerroristAttack #StockMarketIndia #stockmarkets

CNBC-TV18@CNBCTV18Live

Pahalgam attack: PM Modi says armed forces have full freedom to decide on targets, timing of response #PahalgamTerrorAttack cnbctv18.com/india/pahalgam…

English

@THESMTRADERS Rightly said , they should bleed badly like our portfolio

English