Chris™@ProbableChris

Why Market Regimes Matter

If you want to know when to widen/shorten your stops, when to use bigger/smaller risk, when to use mean reversion frameworks vs trend continuation frameworks.....knowing the market regime you are trading in is how you can determine the answers to those questions.

The market will always move from periods of compressed distribution to elevated distribution. Think of this simply as low volatility vs high volatility. When the market has been slow grind trending for awhile, you are in a compressed distribution. When the market has been creating big outlier days for awhile, you are in an elevated distribution.

Elevated Regime:

Here the market is active, its more volatile. High realized volatility usually accompanies directional conviction, news, or repricing. Moves extend further than they normally would, which punishes early fades. But elevated vol also produces the largest reversion spikes (exhaustion reversals), so mean reversion here is higher-reward and far higher-risk, and timing-dependent. In elevated regimes, expect wider moving bars, stops would be better placed wider or if not moved wider potentially using less $ risk, and the strategies you employ should be able to leverage this elevated volatility.

Compressed Regime:

Here the market is less volatile, you will see slow moving range days or slow grinding trend days. Low realized volatility means price is coiling in a tight range overall. Compression is also the setup before an expansion move. Volatility clusters, so a quiet regime is "storing" energy. In compressed regimes, expect smaller overall range within bars, stops can be tighter, and the strategies you employ here should not be trying to capture large moves because that is not the norm in compressed regimes.

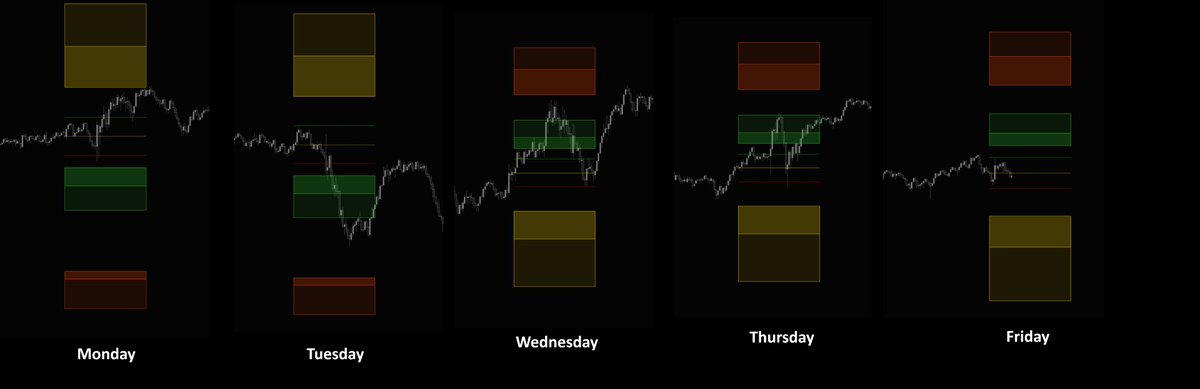

There are various ways to analyze the market and detect what regime you are in. I collect a 5yr baseline of distribution which gives me the +/- SDEV value. I than compare that baseline to the last rolling 10-days distribution, and view this data for the last 6 month, providing me with a chart. This shows me how recent price has been trading against historical price, as it pertains to market norms. I can also see when price is starting to come out of compression into an elevated state, or when price is reverting from an elevated state and falling into compression. Seeing this in the form of a chart allows me to start to make plans and assumptions and adjust my risk and strategies according.

One strategy with one risk profile is not applicable to all market regimes. Elevated, actively expanding, compressed, actively compressing....these are the 4 regimes I focus on and they tell me how I should treat the Day, the New York AM, and each individual hour. You can apply this framework to anytime time based range.