@ProbableChris btw do you use any oscillators? I saw on some of your videos some grey background with 1 or 2 lines. is this MACD lines or moving averages?

English

andrii

118 posts

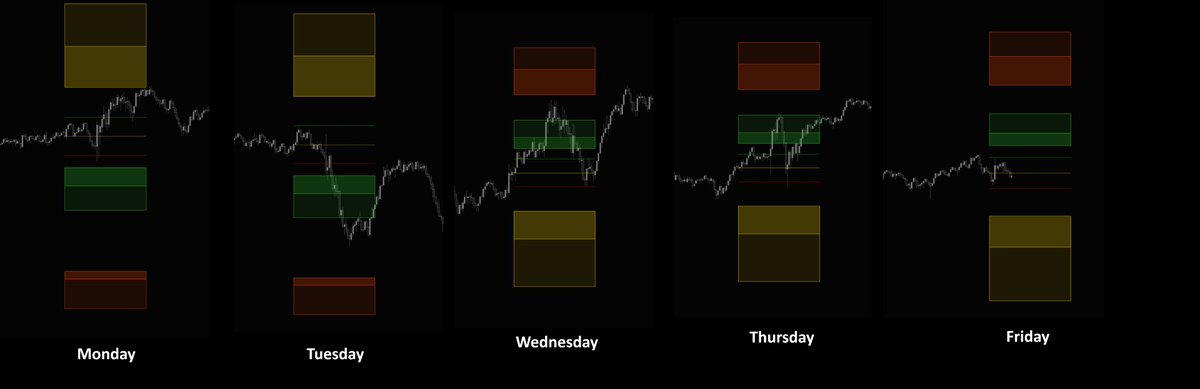

New module added to NQ Stats "AM TBR" - nqstats.com/am_tbr.html Have been meaning to get this added to the site, just haven't had time. This is time based range data I use pretty much every day as a confluence/filter for trades taken typically before NY open. The idea is simple, collect a rolling 20-day price distribution of the 8am-12pm time based range. If you aren't familiar with price distributions, check out that section on the site. This rolling distro is used to get the +/- 0.25 sdev values, which are the trigger points. Which ever is hit first, either the + or - 0.25, this creates the expectation of reversion back to the TBR Open (8am open). The site provides total reversion metrics and by-the-hour metrics. I specifically focus on reversions within the first hour (8am hour), as that has the highest hit rate. MAE for reverted and non-reverted events is provided, as well as the MFE beyond the TBR Open, derived from 10yrs of data. You will find various other data pieces on the site, but here is what it looks like on a chart. Video coming soon....

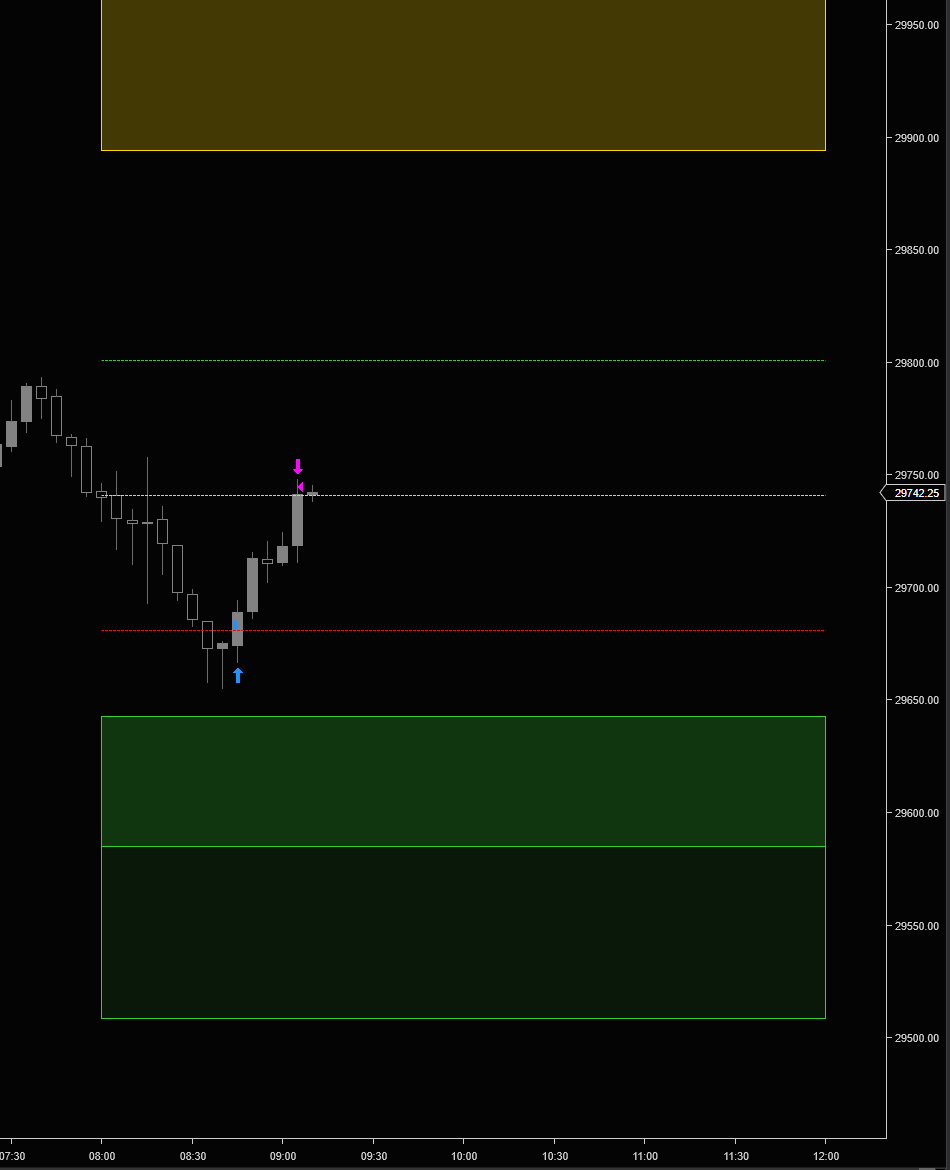

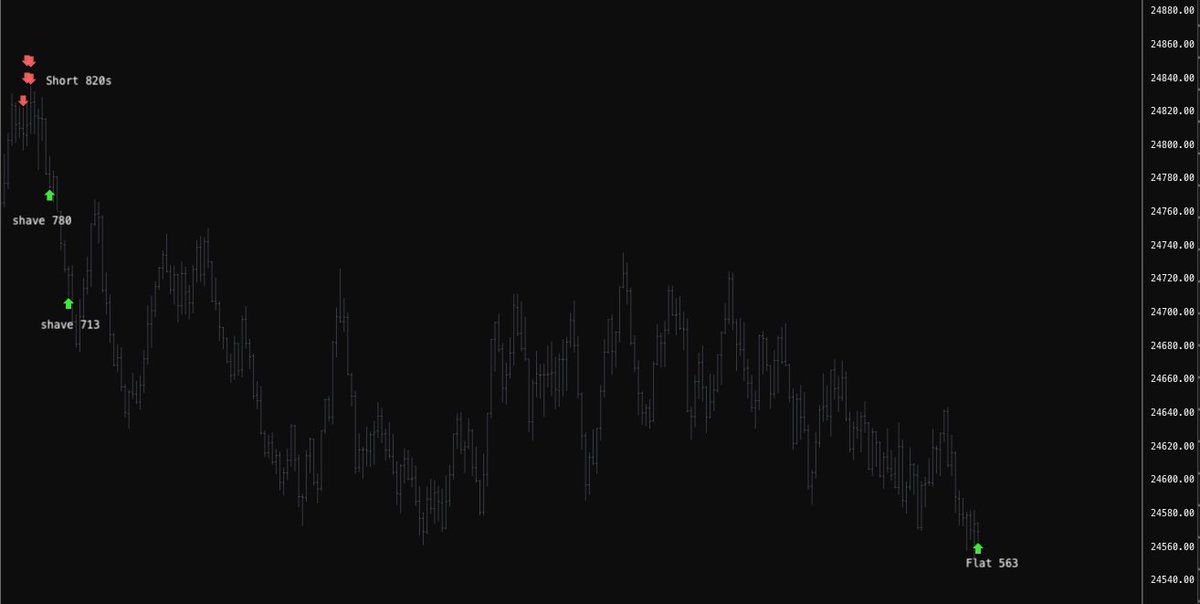

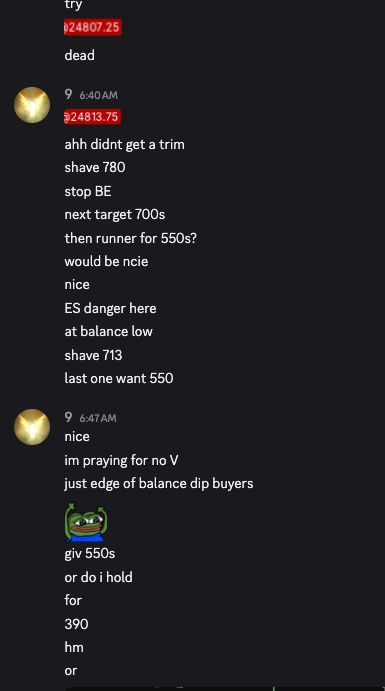

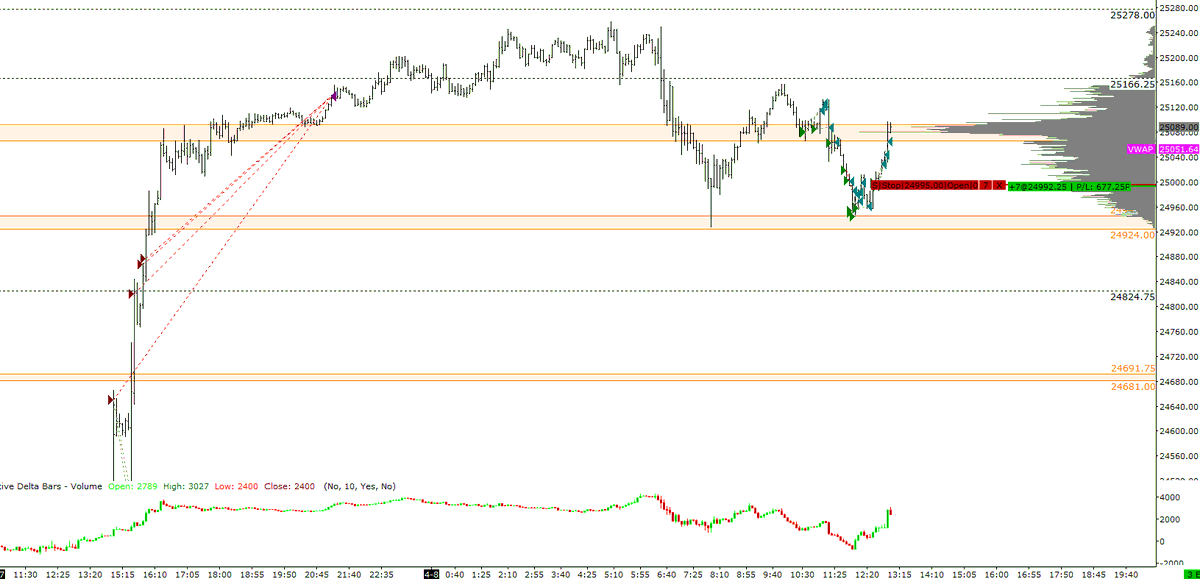

Stupid AMP margin requirements holding me back to relatively small size tonight 24800 avg short risking liquidation 150ish

Thanks to AI coding, a complex learning process is now much simpler. I filtered the top 7% YTD stocks from 2000–2026 (including delisted ones), get 1400+ stocks, and visualized them with TradingView Lightweight Charts, featuring auto-marked highs/lows and direct period displays. Browse by year or symbol, even delisted stocks from the last decade like $LVGO and $TWTR are fully accessible. Once I refine the charting and annotation features, I will open-source this learning project.

A simple version, copy paste functionality, is now public code. I tried to be as explicit as possible in the README to make it easy for anyone to set up on their own. gitlab.com/erikcarell/fin… @jfsrev

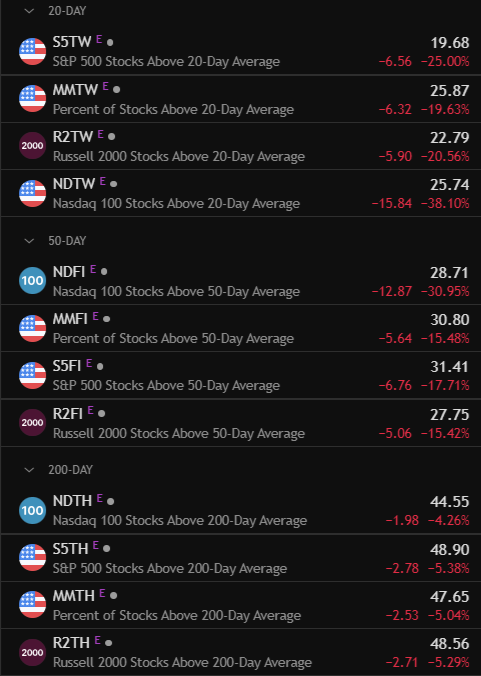

This is my free EOD breadth level panel on @tradingview — you can use the same ticker to build your own, there are much more options but I always have mine based on traditional MA value. Breadth absolutely deserves a place in your trading system, and I couldn’t agree more. When used right, it’s incredibly powerful — especially when you combine with a thorough screen of sectors and industry groups showing relative strength. One important nuance I want to highlight: relative strength isn't just about securities outperforming the benchmark on the surface. It also emerges from names that show the least weakness during prolonged down moves. That resilience matters, and that itself will be a upturning RS on a line chart based indicator. To consistently spot these opportunities, routine is everything. Regardless of what the market throws at you, your process has to stay intact — it’s what anchors your emotional discipline. Don't shut off yourself from market because of capitulation days, you should actually put even more time to mutiple screening to sieve out names for your watchlist. P.S. If the market gives us one more round of capitulation, I’m genuinely excited about the potential long bias setups that could follow. ES Futures at asia open now has already gapped down but with potential doji star to close (indecision candle), and reduced volatility going forward can build the second bear flag for April.