Quality Growth Capital

840 posts

Quality Growth Capital

@QGrowthCap

Engineer. Learning everyday about Micro/Smallcap selection: $IREN, $ONDS, $OSS, $LPTH, $SATL, $PNG.V. Smaller : $ZMDTF, $FTG, $RW.V, $VST.CN, $NPTH.V

Safe Pro Appoints Former @anduriltech Executive and U.S. Army Contracting Officer Brian Mack to its Strategic Advisory Board. Appointment to Expand Capture of Government Contracts and Further Align Safe Pro’s Emerging Artificial Intelligence Technology to Funded Army Programs and Roadmaps. bit.ly/4lMTifc $spai #AI #Drones #DefenseTech

$SIVE has gotta be the highest upside stock I’ve seen in this market since $AXTI? No way markets missed the CW laser light source for Jabil, Marvell (Celestial via $POET), O-Net, Ayar ( $NVDA, Mediatek backed)… At a $140M valuation. ($350m now) Not only do you get the most direct laser exposure to future CPO scale up? But also this cycle’s 1.6T pluggables with $JBL (formerly Intel Silicon Photonics division) coming soon. With Win Semi bridge capacity scaling needed for hyperscaler supply chains. Don’t think 99.9% of people realized the sheer scale of this yet.

🚨Just In🚨 The NATO Support and Procurement Agency (NSPA) is seeking information from industry to assist with the development and planning of a potential new requirement involving the acquisition, implementation and ongoing life cycle support of a Commercial Off-The-Shelf (COTS) or Military-Off-The-Shelf (MOTS) Counter Unmanned Aerial System (C-UAS) capability - non kinetic deployable solutions. The intention is to evaluate what could be immediately available as a solution with respect to systems, sensors, technologies and methodologies pertaining to countering UAS class 1 and class 2. The C-UAS capability shall provide NATO and Allies the operational awareness and potential UAS mitigation during peacetime vigilance, crisis and conflict. Source: eportal.nspa.nato.int/eProcurement5G…

@gfc4 curious to hear what @markminervini has to say, i would assume he is one of those

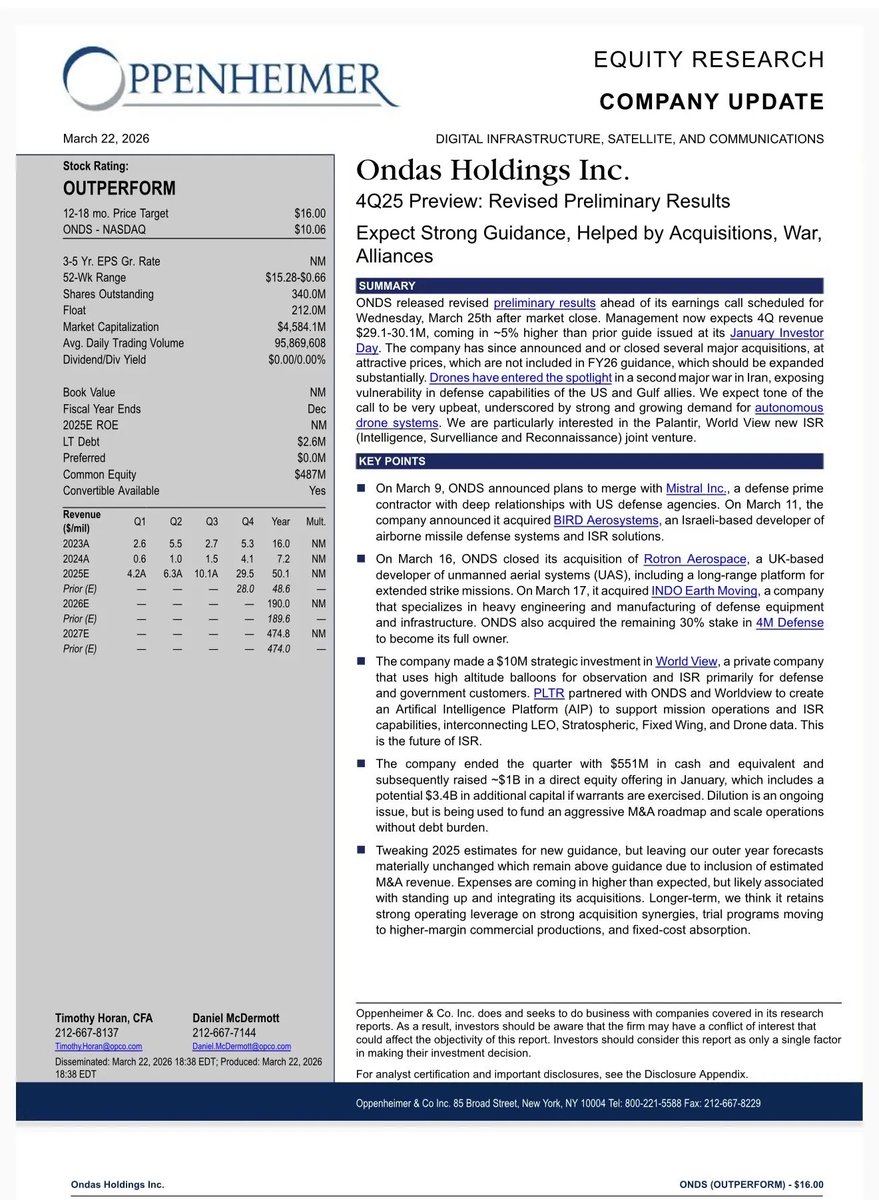

$ONDS 🔵 Q4 revenue of $30.1 million meeting the high end of our recently pre-announced target range and represents a step-change increase from prior quarters ⚪️ Full-year 2025 revenue of $50.7 million, meeting the high end of our recently pre-announced target range, representing approximately 605% year-over-year growth 🔵 Raising full-year 2026 revenue target to at least $375 million and establishing Q1 2026 revenue target of $38 - $40 million, representing approximately 640% and 820% year-over-year growth, respectively. ⚪️ Balance sheet strengthened with approximately $594.4 million in cash, cash equivalents and restricted cash as of December 31, 2025, and with approximately $960 million in net cash proceeds raised in January 2026, providing substantial capacity to support organic growth and strategic M&A ir.ondas.com/press-releases…