Finn Stockinger@FinnStockinger

Trio-Tech $TRT: The Final Line of Defense in the AI and 800V Infrastructure Chain

Meet Trio-Tech International ($TRT), a company perfectly positioned at the epicenter of the global hardware infrastructure shift.

They provide critical high-voltage reliability testing and "burn-in" services for the world’s leading semiconductor manufacturers, ensuring the physical survival of chips powering AI Data Centers and 800V DC grids.

Read on to discover why this micro-cap is great opportunity to invest in the 2026 hardware boom.

1⃣Technical Moat: Why $TRT is Not AEHR

To understand TRT’s value, one must distinguish its role from market darling Aehr Test Systems (AEHR).

$AEHR (Wafer-level): Their systems screen chips while they are still part of a silicon wafer. This is the first stage of filtration—efficient, but not final.

$TRT (Package-level): Trio-Tech enters at the Final Stage. They test chips after they have been cut, bonded, and packaged.

In the era of AI Data Centers, where a single module costs tens of thousands of dollars, package-level testing is the only guarantee that a chip still holds its parameters after the stresses of the packaging process.

TRT acts as the "Final Auditor." They subject finished units to extreme thermal stress (burn-in) and mechanical forces in centrifuges to eliminate latent defects. TRT does not compete with AEHR; TRT closes the loop that AEHR begins.

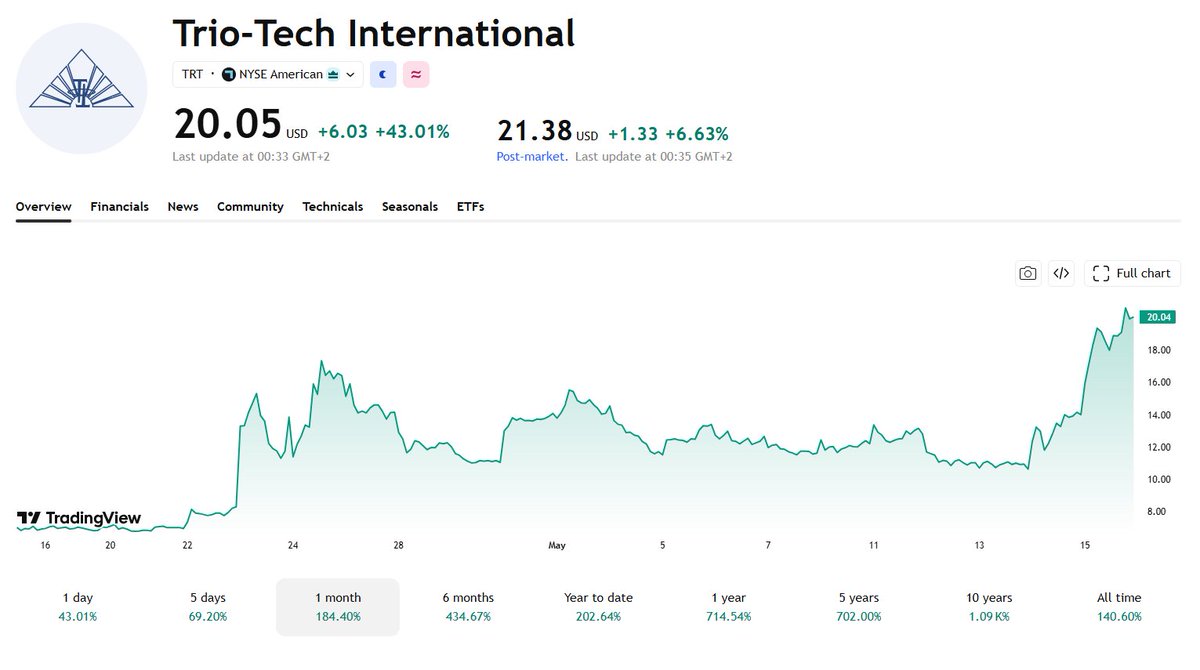

2⃣Financial Fundamentals: $19M Cash vs. Low Valuation

The 2026 balance sheet reveals a rare disparity between market valuation and real capital:

Cash Position: The company maintains approximately $19.5M in cash (approx. 32% of its market cap).

This provides a massive safety cushion with no significant long-term debt.

Inventory Strategy: Inventories have scaled to roughly $11M.

This is not "dead weight" but a strategic stockpile of components for their proprietary Burn-in Boards (BIBs) and test systems.

TRT has pre-positioned itself for a surge in orders, drastically shortening lead times.

Enterprise Value (EV): After stripping out the cash from the $73M market cap, the market is valuing TRT’s global operational business at only $40M.

With annual revenues near $40M, you are paying roughly 2.0x Sales (EV/S) for this infrastructure.

3⃣The AI Direction: Infrastructure Over Software

AI chips operate under extreme loads and generate record amounts of heat.

This drastically shortens their lifespan without proper "seasoning" in the testing phase.

Optical Modules & Accelerators: TRT has secured orders for testing boards dedicated to high-speed interfaces and GPUs.

Vendor Lock-in: By designing custom test fixtures (sockets) for the specific housing of new AI chips, TRT creates high switching costs for customers, ensuring revenue stickiness for years.

4⃣The 800V DC Standard: Breakout in Automotive & Data Centers

The transition to the 800V DC standard is one of the strongest current technological trends, and TRT is positioning itself as a key partner in this shift.

➡️AI Data Center Infrastructure:

AI data centers are moving away from low voltages toward 800V DC buses to drastically reduce energy losses when delivering massive power to GPU clusters.

Every power conversion module operating at these voltages must pass rigorous reliability tests in TRT’s chambers.

➡️Renewable Energy & BESS:

Battery Energy Storage Systems (BESS) and solar inverters are also shifting to the 800V standard to increase transmission efficiency. TRT tests the power semiconductors (SiC/GaN) that manage these flows.

➡️Automotive 800V:

In the EV sector, 800V architecture allows for ultra-fast charging. TRT holds unique military-grade certifications (MIL-STD) that allow them to test components for ADAS and high-voltage drivetrains where the margin for error is zero.

5⃣Production Capacity and Cycle Timing

The company has completed a period of heavy capital expenditure (CapEx) to modernize its laboratories in Singapore and Thailand. It is now in the monetization phase:

➡️In-House Manufacturing:

TRT builds its own centrifuges and burn-in systems. During a boom, they don't wait in line for equipment; they scale their own lines internally.

➡️Operating Leverage:

With fixed costs for service centers already covered, any increase in machine utilization above 75% translates into a rapid spike in operating margins and Earnings Per Share (EPS).

⬇️Verdict

Trio-Tech is a classic "Deep Value Play" with a massive cash floor.

The company has prepared its inventory and infrastructure for the next wave of orders from the AI and 800V DC high-voltage sectors.

For the investor, this is a purchase of a critical link in the supply chain at a moment when the market is beginning to realize that without physical reliability, no technological revolution can survive the test of time.