Sabitlenmiş Tweet

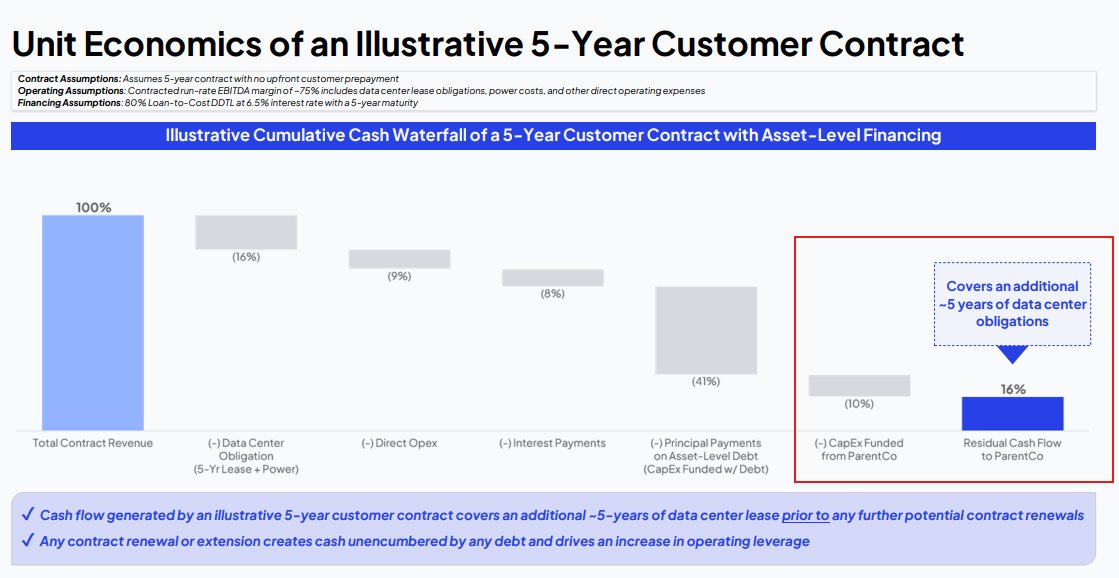

TeraWulf WULF Investment Thesis (PDF in link below, no paywall)

rittenhouseresearch.substack.com/p/terawulf-inv…

$WULF

English

Rittenhouse Research

2.4K posts

@RHouseResearch

AI infrastructure, data centers, neoclouds, software, fintech.

In Ackman's latest interview he divides the AI market, stating that it is not a bubble at the foundational layer, but highly risky at the software/model layer. He sees "near infinite demand" for compute. He believes infrastructure providers such as Microsoft, Amazon, Meta, and even SpaceX will earn massive returns on their data center investments. He is highly skeptical of pure model layer businesses like OpenAI and Anthropic. He notes they face massive capital burn rates and an existential threat from open-source models such as Chinese model and SpaceX that are driving the cost of AI access effectively to zero. A business model reliant on charging for proprietary models will collapse if open-source alternatives are essentially free. $AMZN $META $MSFT $SPCX

Chamath Palihapitiya says he regrets coming on CNBC and talking about SPACs in 2020 & 2021

Chamath Palihapitiya says he regrets coming on CNBC and talking about SPACs in 2020 & 2021

Published some thoughts on substack (no paywall) around CoreWeave's unit economics, margins, use of debt, and what I think the real risks to the business are open.substack.com/pub/rittenhous…