Sabitlenmiş Tweet

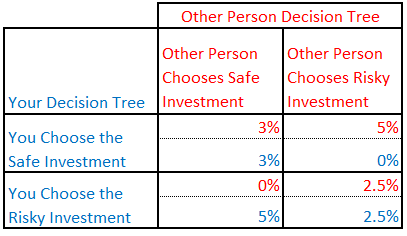

1/What happens when an industry creates individual incentives of a system that pit the individuals against each other and leads to a worse outcome for both of them--but a better outcome for the industry?

I explore this topic in this week's "Separating Value From Bias" edition

separatingvaluefrombias.substack.com/p/7-game-theor…

English