Ben Briggs@Rex_Finance

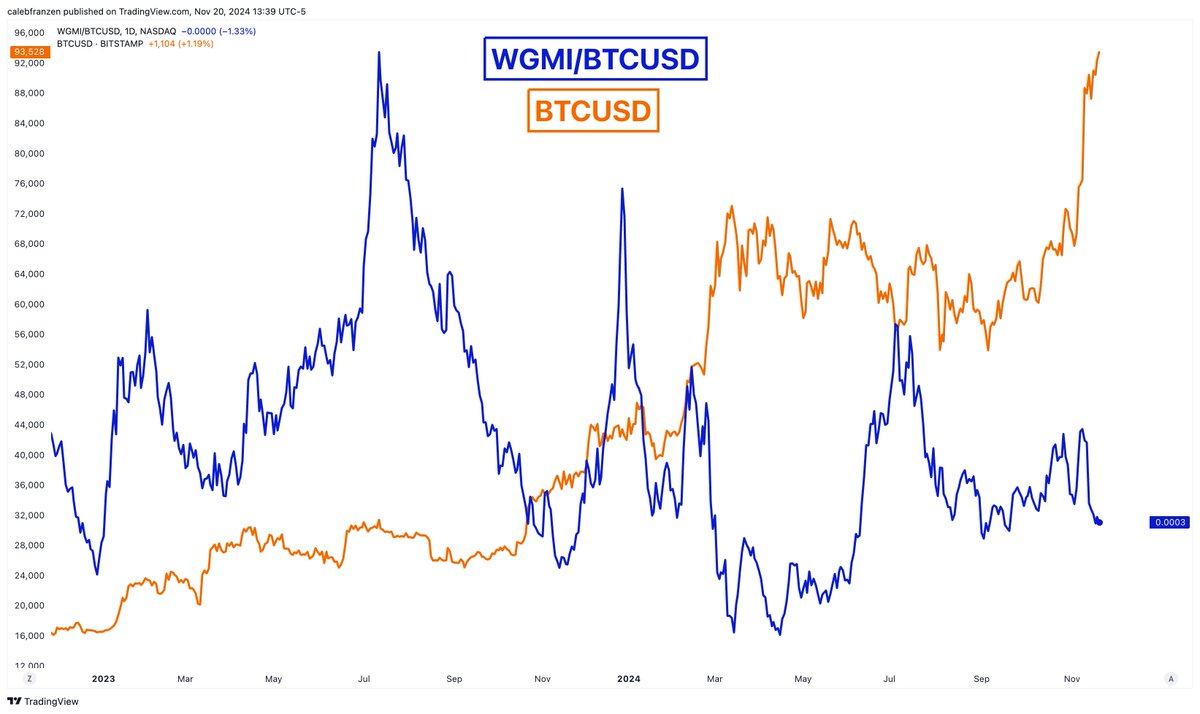

Not picking on $MARA, they're simply the latest example. This goes for all profitless companies in high risk, profitless industries (Bitcoin, HPC/AI, etc.).

As I see it today, I will never own a company in a profitless space that leverages up their company via convertible notes - even if they're "oversubscribed." They're often oversubscribed because they're free money for the lenders, who end up shorting the equity to hedge their long positions that are created via the debt repayment in shares.

Here's why: in a profitless space, the only way to pay convertible debt is by selling new shares to raise cash (dilution) OR by issuing new shares to the lender (dilution). If this is true, you're diluting to raise the same amount of money, except now you're stacking interest expense & additional fees on top of the ATM dilution. This makes little sense to me.

Now, I'm not blinded. The one benefit of convertible debt is that you can theoretically delay dilution. It's obvious how this could be beneficial in a bull market. However, it can absolutely destroy a company & shareholders in a bear market (I've seen it happen many times).

My dilemma: is it worth the gamble from management teams to utilize convertible debt in a profitless, highly-volatile space? It makes even less sense to me if a company purchases spot #Bitcoin with the proceeds, when they should be able to mine Bitcoin for a 20-30%+ discount to spot prices.

🤷🏻♂️What are your thoughts?