@VKMacro To be fair its not totally contradictory. 2y reals have moved in almost opposite directions. But hard to call UK real yields tight...

English

RobertTimper

558 posts

And finally, amidst the bond market yield debate (where QT, Gilt issuance, political risk, Brexit, and inflation expectations are all playing interdependent roles) the cumulative picture of UK price growth - versus benchmark economies - helps the additional yield premium demanded on GBP debt. Consumer prices have risen 31% since January 2020.

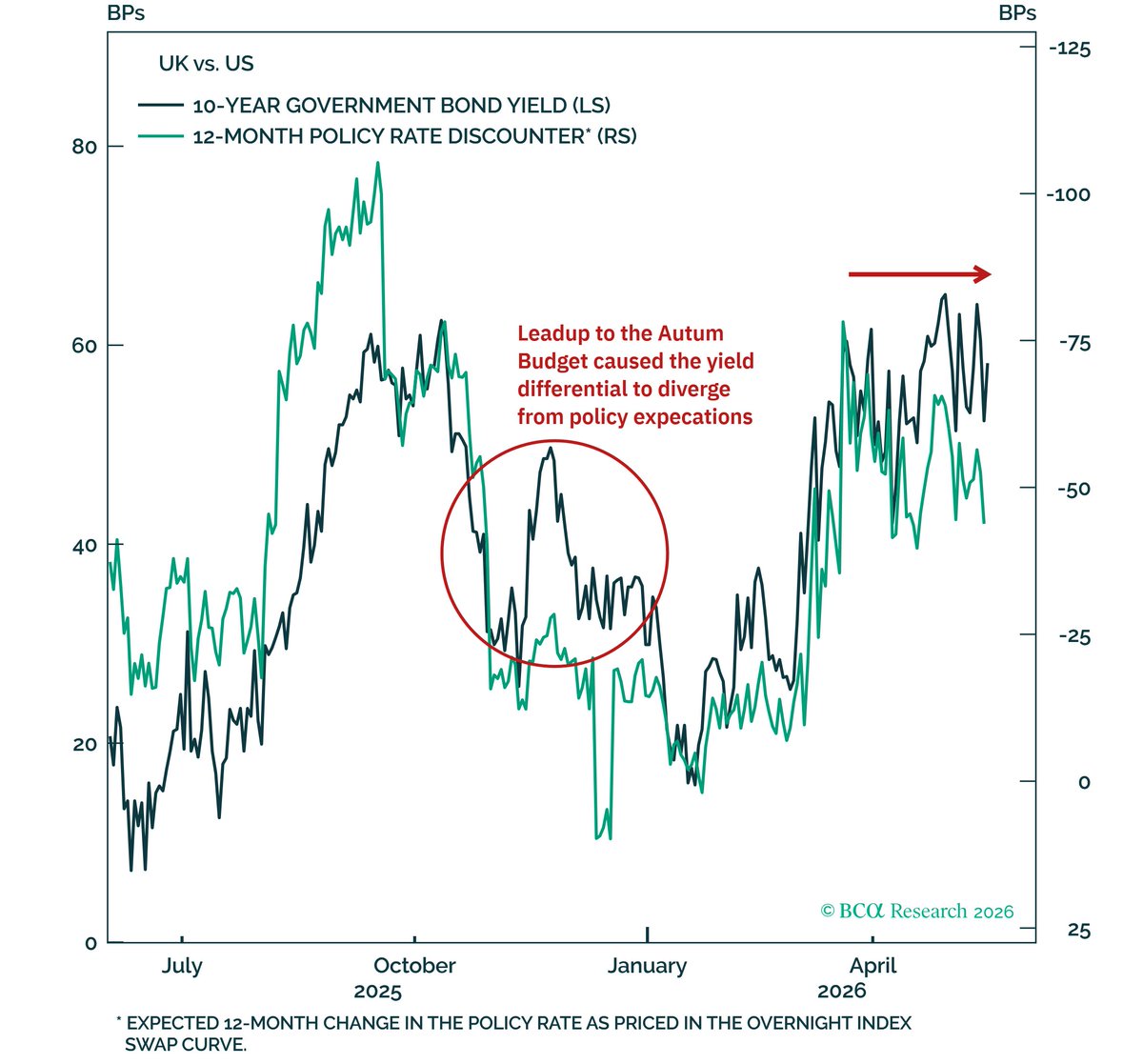

Despite the political turmoil and headlines in the UK, the gilt market has barely reacted to the risk of more fiscal spending. Yields have risen globally due to higher oil prices. The US/UK yield differential has been stable and largely driven by relative policy expectations.

The Cleveland Fed's median CPI was +0.40% in April, or 4.9% annualized. The 12-month median CPI ticked up to 2.8%, the first such increase since last summer. (The median CPI looks at the price change of the item sitting in the middle of the basket each month, which strips out the outliers that can distort core CPI.)

The effect of last week’s yen intervention is already fading, with JPY/USD at 158. The real “intervention” necessary is BoJ rate hikes. 2-Year real yields are negative again, while rising long-term inflation expectations are hurting the yen. It’s time for BoJ hikes.