Sabitlenmiş Tweet

Jeremy

19.8K posts

Jeremy

@JeremyWS

G10 & EM Macro … FX/Rates/Vol/Credit. new blog found at https://t.co/PRYnQS45AT

London Katılım Nisan 2009

754 Takip Edilen7.2K Takipçiler

Vibe shift in USD continuing, as US exceptionalism narratives take hold.

US now the clear country with the best growth fwd, and now the mkt has come to terms with a hike (u6 pricing 12.5!)

EURUSD vs 5y real rates shows a huge divergence.

It’s all driven by $ RY going up May

English

@Sergei1544 Yep. Makes directional trading tricky and so prefer looking at more Vol/RV structures.

The easy trade is over imo.

English

Sometimes the chart voodoo works.

Sfrz7 bounced at 96.00.. US10y back flirting with the major trendline.

Lots of bad shorts at bad levels sets up squeeze potential. 4.45/50 area 10y might make sense to reload.

Destination still for higher rates imo, but we’ve moved fast.

English

@RobertTimper1 What do you have for today’s core CPI seasonally adjusted ? Smth like 0.3? Thanks mate

English

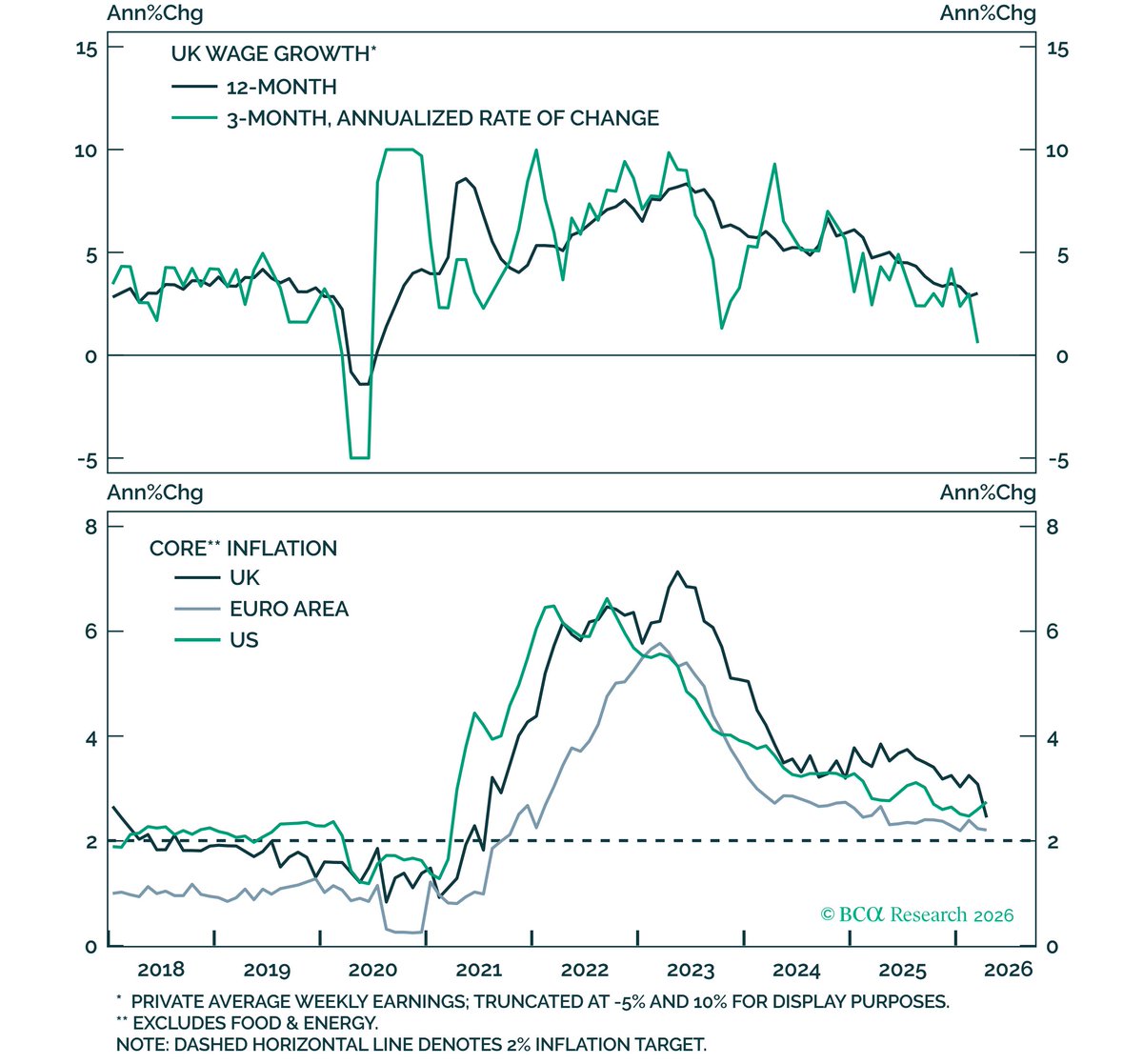

Does the UK still have an inflation problem?

After yesterday's wage growth data and today's inflation data, the underlying inflation picture at least doesn't look different from DM peers.

English

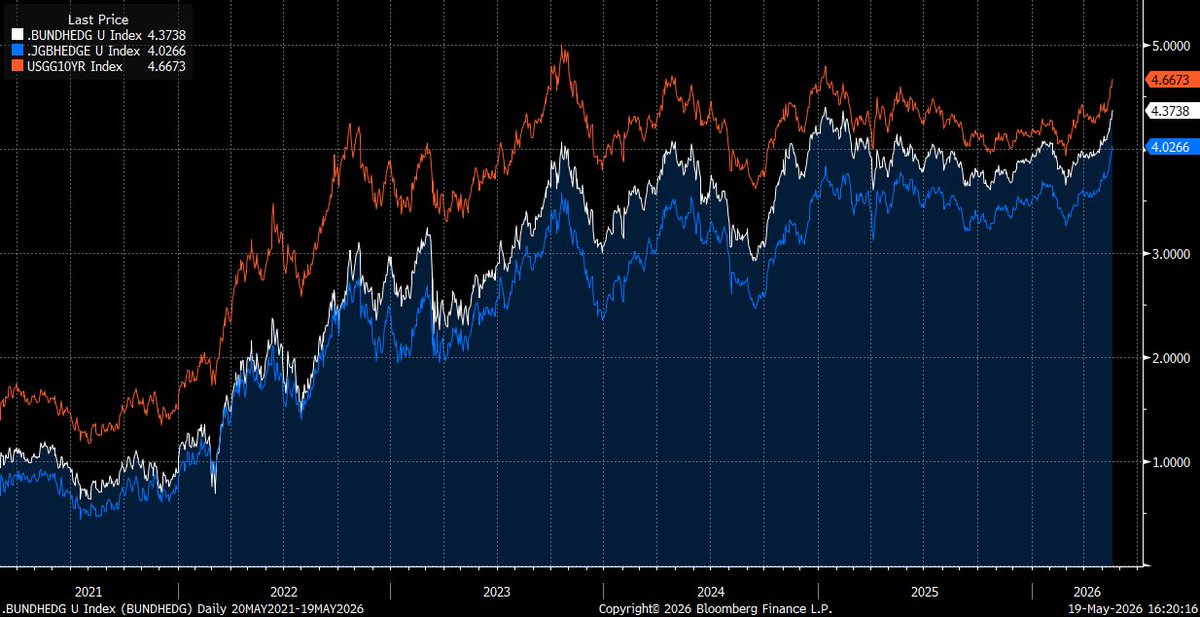

@sunchartist Got a bit busy this afternoon lol… have the bund and JGB hedged into USD handy, (vs UST10yr).. you can infer relative attractiveness for JPY domiciled from the 3 comparatively

English

@JeremyWS Thank you. Can you look at uss and German bonds swapped in jpy. I am wondering how much demand for foreign ccy bond fall give rise in yen nominal rates

English

I think under appreciated in JPY rates is the speed and direction of travel of Inflation swaps.

5y up to new highs today, up 70bps since the war, and 35bp this month!

BoJ falling further behind the curve. GDP overnight allays immediate concerns for June. But more is needed.

English

@sunchartist Unless that’s not what u wanted. Lmk , always got time for you

English

@sunchartist Hedged JGB back into USD… 10y JGB xccy hedged (full terms) at 4%

For the most spice, a 40y JGB, hedged with 1yr xccy is 6.8%!!

English

@cchengasaurus Yeh that’s the bit on the payoff matrix where you lose bad… For me it’s the least likely path of what can actually happen. But who knows!

I wouldn’t rec anywhere sofr personally.

Trade mostly pushed there is sep/oct/dec fomc fly.

English

@Augustus_kaizer Sure, just subjective to the whims of the market on any given day and time…

What do you see as the modal path here?

Which is the bit you disagree with most?

English

@Augustus_kaizer This is twitter my guy. Gotta keep it simple…

In any case, wasn’t referring to market implied. But simply my own most likely path.. (And that of about 90% of people i speak too)

English

@PatrickBasiewic @pdegrauwe Agreed. Completely misses the point tho. UKT does not borrow at a higher rate than French treasury.

BoE sets a higher policy rate than ECB does.

The author almost gets there in the piece, but fumbles it at the line.

English

@JeremyWS @pdegrauwe Hi. Interns also know that Uk needs GBP for spending and Europe needs Euros… and they know how IRP works

English

Why does the UK government carry a higher interest burden than the French government? open.substack.com/pub/pauldegrau…

English

@JuliusProbst @pdegrauwe Yep exactly! I gave the author the benefit of the doubt that it was either a typo or English translation error… context of the blog was for yields, not burden, but yes, if referring to burdens then the analysis is even more wrong! Hilarious eh

English

@JeremyWS @pdegrauwe Lol, this is basically irrelevant for the debt burden. interest rate burden UK ~3.6% of GDP, France ~2.5% with roughly similar debt level

English

@WinMonroe @NewLeftEViews Indeed, someone needs to do it, and no better than Toby at it!

English

@JeremyWS @NewLeftEViews On the discourse, Toby Nangle at FTAlphaville has been doing gods work trying to bring good bond chart hygiene back into vogue

English

From a master on the political economy of monetary policy:

“One wonders what the political agenda of the Bank of England was to put so much pressure on its own government, while other central banks, in particular the ECB did not do so. This is all the more surprising because the Bank of England failed to contain inflation, and then acted as a super bond vigilante punishing its own government with higher interest rates.”

Paul De Grauwe@pdegrauwe

Why does the UK government carry a higher interest burden than the French government? open.substack.com/pub/pauldegrau…

English

@WinMonroe @NewLeftEViews The author was so muddled in his writing…

he *almost* got to a reasonable answer… (which would be comparing Real yields on the bonds)… alas he just couldn’t find it.

Shame… I really thought this tragic discourse of comparing yields died out in the eurozone crisis.

English

@NewLeftEViews good time to reasses it. I suspect they were concerned about "financial dominance" but rebalancing once inflation was credibly declining would have been better in retrospect imo.

Also, there are some methodological issues with this comparison:

x.com/JeremyWS/statu…

Jeremy@JeremyWS

@pdegrauwe Hi Paul, that’s not how bonds works. UK pays 0.25% less interest than France does, when adjusting for Ccy… Even interns know how this works… Please do better.

English

Great week for the core rates view… 2027 dates across the world leading the sell off… and fed hikes finally part of the debate

We got to ~4.60 10y and 96.00 SFRZ7 much quicker than anticipated.

ER u6u7u8 fly up at 27 and GBP rates immolated (but for very different reasons!!)

Jeremy@JeremyWS

Global Rates Outlook #5: Price V Quantity & a New Era For Central Banking. Scenario based Fwd guidance & G10 responds to the Iran war more with Price than they do Quantity. And an attempt to argue the bullish case for the UK economy?? Yeh.. jwsmacro.substack.com/p/global-rates…

English